Rising Treasury Yields & Policy Uncertainty Interrupt Rally in Stocks

1/1/2025 (Updated: 4/9/2026) - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

As 2025 unfolds, the backdrop for common stocks still looks positive as a couple of the trends that powered common stocks higher over the past two years remain in place, while others have largely played out, but do not appear to be poised to reverse and become headwinds to stock prices. However, the new year brings a new round of policy uncertainties that will only clear up as Congress and the incoming administration decide on a wide range of policy proposals.

While inflation remains well off the 40 year highs recorded in mid-2022, the reported inflation data remain above the Federal Reserve’s 2% target, and progress appears to have stalled. The inflation data remain messy, however, due to distortions from the shelter component and from several one-off items, such as higher used vehicle prices due to the vehicles lost to the hurricanes and higher egg prices from an outbreak of a fatal strain of bird flu. The year-over-year rise in the consumer price index in November was 2.7%, higher than the October reading of 2.6%, while the core CPI rose 3.3% year-over-year and has been stuck between 3.2% and 3.3% for the past six months.

The inflation reports are still biased to the high side by shelter costs (4.6% higher year-over-year) which accounted almost two-thirds of the year-over-year rise in both the headline and core CPI readings for November. The roughly 18 to 24 month lag with which real time rent prices factor into the CPI is a well-documented distortion of reported inflation to the high side currently.

Removing shelter, the headline CPI was higher by 1.0% year-over-year, while the core CPI was higher by 1.2%. Consider that if a real time rent measure was used in the calculation of the CPI — the Bureau of Labor Statistics reports that rent increases for new tenants were higher by 1.0% year-over-year in 3Q 2024 — core inflation over the past twelve months would be 2.0%, right in line with the Federal Reserve’s target.

Investors also tried to determine the most likely path of policy under the new administration, particularly for immigration and trade. President-elect Trump has promised to close the southern border and deport illegal immigrants and raise or impose new tariffs on trading partners when he takes office later this month. Those policies could reverse two developments that have supported the disinflation trend of the past two years, falling goods prices and slower wage growth.

Equity Markets

Rising Treasury Yields and Policy Uncertainty Interrupt the Rally in Stocks

After posting very strong gains during November in the aftermath of the presidential election and the second rate cut by the Federal Reserve, common stocks were not able to gather any upward momentum during December as investors digested the continued move higher in Treasury yields and tried to determine the state of inflation as the data delivered mixed messages. Consider that the yields on two-year and ten-year Treasury securities rose another 8 and 40 basis points, respectively, last month and are higher by 70 and 94 basis points since the Federal Reserve cut rates back in September. High and rising Treasury yields typically represent a significant headwind to higher common stock prices, as Treasury securities provide risk free returns when held to maturity.While inflation remains well off the 40 year highs recorded in mid-2022, the reported inflation data remain above the Federal Reserve’s 2% target, and progress appears to have stalled. The inflation data remain messy, however, due to distortions from the shelter component and from several one-off items, such as higher used vehicle prices due to the vehicles lost to the hurricanes and higher egg prices from an outbreak of a fatal strain of bird flu. The year-over-year rise in the consumer price index in November was 2.7%, higher than the October reading of 2.6%, while the core CPI rose 3.3% year-over-year and has been stuck between 3.2% and 3.3% for the past six months.

The inflation reports are still biased to the high side by shelter costs (4.6% higher year-over-year) which accounted almost two-thirds of the year-over-year rise in both the headline and core CPI readings for November. The roughly 18 to 24 month lag with which real time rent prices factor into the CPI is a well-documented distortion of reported inflation to the high side currently.

Removing shelter, the headline CPI was higher by 1.0% year-over-year, while the core CPI was higher by 1.2%. Consider that if a real time rent measure was used in the calculation of the CPI — the Bureau of Labor Statistics reports that rent increases for new tenants were higher by 1.0% year-over-year in 3Q 2024 — core inflation over the past twelve months would be 2.0%, right in line with the Federal Reserve’s target.

Investors also tried to determine the most likely path of policy under the new administration, particularly for immigration and trade. President-elect Trump has promised to close the southern border and deport illegal immigrants and raise or impose new tariffs on trading partners when he takes office later this month. Those policies could reverse two developments that have supported the disinflation trend of the past two years, falling goods prices and slower wage growth.

Investors also tried to determine the most likely path of policy under the new administration, particularly for immigration and trade.

Mid-month the Federal Reserve signaled its intention to slow the pace of rate cuts this year amid worries that inflation progress has stalled at a rate above the Federal Reserve’s 2% target. Finally, Congress wrestled with passing a funding bill to keep the federal government open past December 20, only averting a government shutdown when the House approved a stopgap measure to fund the government until mid-March at the eleventh hour.

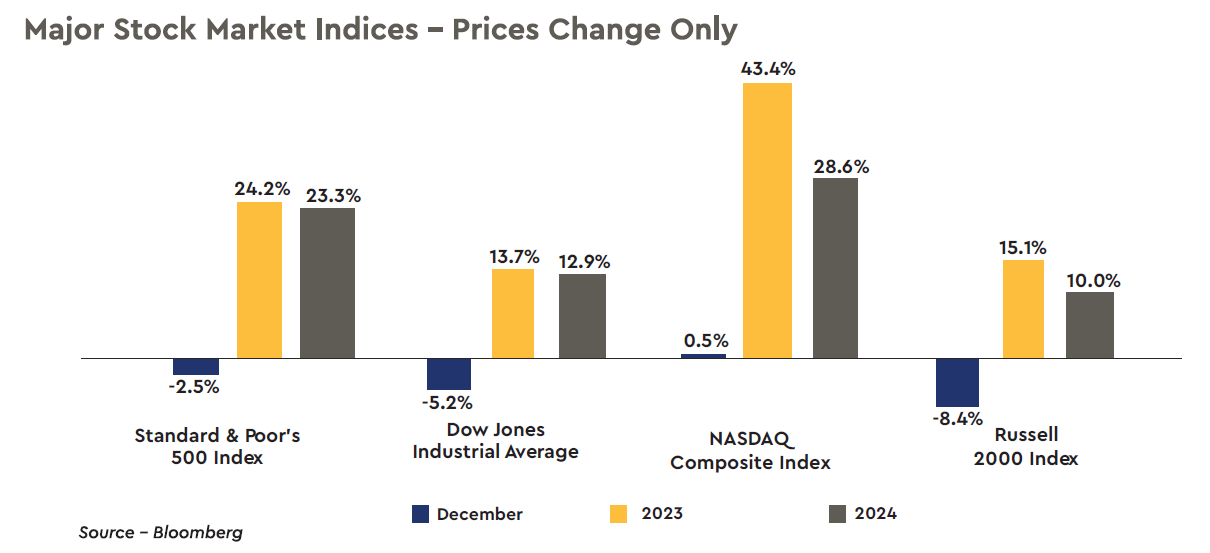

These concerns weighed on investor sentiment during December, leading to a lack of buying interest for common stocks rather than a bout of aggressive selling pressure. Only the technology-heavy NASDAQ Composite posted a gain last month, rising a modest 0.5%. The Russell 2000 Index of small company stocks, which tend to issue more floating rate debt than do larger companies, bore the brunt of the shift in the outlook for fewer rate cuts this year and into 2026, by falling -8.4%. The S&P 500 and the DJIA declined -2.5% and -5.2%, respectively, during December.

Despite the small decline in the S&P 500 last month, the broad U.S. stock index basically matched its strong 2023 gain of 24.2% by rising another 23.3%, marking its best consecutive years since 1997 and 1998. The NASDAQ Composite turned in the best performance for 2024 with a gain of 28.6% following a spectacular advance of 43.4% in 2023. The DJIA and the Russell 2000 were the laggards on the year posting gains of 12.9% and 10.0%, respectively.

Mr. Powell emphasized in September that the FOMC Committee was not responding to a substantial slowing of the economy, but rather was looking at an opportunity to “recalibrate” policy away from a rigid focus on inflation to a broader effort to make sure the softening of the labor market over the summer did not feed upon itself. The 50 basis point cut in the policy rate was intended to bring the policy rate closer to the so-called neutral rate that neither spurs nor slows the economy’s growth rate.

The Federal Reserve cut rates again at the November FOMC meeting, by 25 basis points, and with the third consecutive rate cut at last month’s meeting, the policy rate has now been lowered by a full percentage point. Policymakers at the Federal Reserve acted with a sense of urgency over the last four months of 2024 to shift policy to a less restrictive posture. The central bank was trying to prevent past rate hikes, which took borrowing costs to a more than two decade high, from pushing the economy into an unnecessary recession which would have served no useful purpose, with inflation off the boil and making progress toward the 2% target and a moderate cooling of the labor market taking place over the course of 2024.

These concerns weighed on investor sentiment during December, leading to a lack of buying interest for common stocks rather than a bout of aggressive selling pressure. Only the technology-heavy NASDAQ Composite posted a gain last month, rising a modest 0.5%. The Russell 2000 Index of small company stocks, which tend to issue more floating rate debt than do larger companies, bore the brunt of the shift in the outlook for fewer rate cuts this year and into 2026, by falling -8.4%. The S&P 500 and the DJIA declined -2.5% and -5.2%, respectively, during December.

Despite the small decline in the S&P 500 last month, the broad U.S. stock index basically matched its strong 2023 gain of 24.2% by rising another 23.3%, marking its best consecutive years since 1997 and 1998. The NASDAQ Composite turned in the best performance for 2024 with a gain of 28.6% following a spectacular advance of 43.4% in 2023. The DJIA and the Russell 2000 were the laggards on the year posting gains of 12.9% and 10.0%, respectively.

Federal Reserve Positioned for a Pause

In a widely anticipated move, the Federal Reserve lowered the target range for the federal funds rate to 4.25% to 4.5% at the December 17-18 FOMC meeting. The Committee’s forecasts and Chair Powell’s comments at the press conference indicated that the initial phase of cutting rates is over. The Federal Reserve began cutting rates at the September FOMC meeting with a 50 basis point cut, which was the first time the central bank went beyond its more traditional 25 basis point cut absent the economy being in recession or the financial markets being in crisis mode.Mr. Powell emphasized in September that the FOMC Committee was not responding to a substantial slowing of the economy, but rather was looking at an opportunity to “recalibrate” policy away from a rigid focus on inflation to a broader effort to make sure the softening of the labor market over the summer did not feed upon itself. The 50 basis point cut in the policy rate was intended to bring the policy rate closer to the so-called neutral rate that neither spurs nor slows the economy’s growth rate.

The Federal Reserve cut rates again at the November FOMC meeting, by 25 basis points, and with the third consecutive rate cut at last month’s meeting, the policy rate has now been lowered by a full percentage point. Policymakers at the Federal Reserve acted with a sense of urgency over the last four months of 2024 to shift policy to a less restrictive posture. The central bank was trying to prevent past rate hikes, which took borrowing costs to a more than two decade high, from pushing the economy into an unnecessary recession which would have served no useful purpose, with inflation off the boil and making progress toward the 2% target and a moderate cooling of the labor market taking place over the course of 2024.

The December FOMC meeting offered a notable shift in the outlook for rate cuts this year and into 2026.

The December FOMC meeting offered a notable shift in the outlook for rate cuts this year and into 2026. New projections show the Committee expects to make fewer rate cuts, with the median forecast pointing to two cuts in 2025, down from four at the September FOMC meeting and only one cut in 2026, down from two. Mr. Powell said the decision to cut rates again “was a closer call” than recent decisions, and that “From here it is a new phase, and we are going to be cautious about further cuts.”

Of the twelve voters at the December meeting, there was one dissent, while three nonvoting members of the Committee indicated that the rate cut was not necessary. Given the strength in the economy and the lack of further progress in the various measures of inflation declining to the Federal Reserve’s 2% target, the Federal Reserve is likely to pause the rate cuts for some period of time. A pause will give the Committee time to review more data, assess the impact of the 100 basis points of rate cuts so far on the current status of inflation and the jobs market, and analyze the initial policies the Trump administration will put into effect.

While the FOMC Committee remains data dependent regarding future policy moves, it has also become policy dependent following Donald Trump winning the presidential election. President-elect Trump has proposed changes to trade, immigration, regulation, and tax policies which will undoubtedly reshape the outlook for growth, employment, and inflation in coming years. The shift in the rate outlook appears to be tied to the uncertainty and risks around the still-to-be-defined policies of the incoming administration.

Consider that while inflation has declined in a significant manner since the peak in the spring of 2022 — thanks mostly to supply chain healing, lower commodity prices, and labor force growth — the slowdown in inflationary pressures has been uneven at times. The path to the 2% inflation target was pushed out to 2027 from 2026 in the latest Summary of Economic Projections, and the Committee now expects core inflation to rise by 2.5% in 2025, higher than its expectation in September of 2.2%. More importantly, the Federal Reserve now sees inflation risks weighted to the upside rather than broadly balanced as it did in September.

On December 18th, investors reacted very negatively to the outlook for fewer rate cuts with the DJIA falling more than 1,100 points, or -2.6%, while the S&P 500 lost nearly -3.0% and the NASDAQ Composite -3.6%. The yields on two-year and ten-year Treasury securities each rose by 12 basis points. There seems to be a sense on the Committee that policy is not as restrictive as previously thought with the Trump administration proposing a pro-growth policy agenda. Investor attention is now shifting from the outlook for interest rates to a focus on fiscal, trade, and immigration policies with the outlook for the economy soon to be in the hands of the Trump administration for the next couple years.

The economy looks to have grown at an above trend pace of 2.7% last year and enters 2025 with positive forward momentum supported by a slowing, but still solid jobs market, steady income growth, strong productivity gains, and healthy business capital spending spurred by artificial intelligence related investments. We continue to expect that the economy is on track for an elongated cycle, helped along by the surge in both business and household sentiment post-election and expectations of a business friendly policy agenda.

Operating earnings for the companies in the S&P 500 are expected to grow roughly 15% to 16% this year according to the analysts at Standard & Poor’s, with the economic expansion remaining on track and further gains in productivity. Look for earnings in the technology sector, communication services, and industrial companies driven by technology to continue compounding at a significant pace.

Of the twelve voters at the December meeting, there was one dissent, while three nonvoting members of the Committee indicated that the rate cut was not necessary. Given the strength in the economy and the lack of further progress in the various measures of inflation declining to the Federal Reserve’s 2% target, the Federal Reserve is likely to pause the rate cuts for some period of time. A pause will give the Committee time to review more data, assess the impact of the 100 basis points of rate cuts so far on the current status of inflation and the jobs market, and analyze the initial policies the Trump administration will put into effect.

While the FOMC Committee remains data dependent regarding future policy moves, it has also become policy dependent following Donald Trump winning the presidential election. President-elect Trump has proposed changes to trade, immigration, regulation, and tax policies which will undoubtedly reshape the outlook for growth, employment, and inflation in coming years. The shift in the rate outlook appears to be tied to the uncertainty and risks around the still-to-be-defined policies of the incoming administration.

Consider that while inflation has declined in a significant manner since the peak in the spring of 2022 — thanks mostly to supply chain healing, lower commodity prices, and labor force growth — the slowdown in inflationary pressures has been uneven at times. The path to the 2% inflation target was pushed out to 2027 from 2026 in the latest Summary of Economic Projections, and the Committee now expects core inflation to rise by 2.5% in 2025, higher than its expectation in September of 2.2%. More importantly, the Federal Reserve now sees inflation risks weighted to the upside rather than broadly balanced as it did in September.

On December 18th, investors reacted very negatively to the outlook for fewer rate cuts with the DJIA falling more than 1,100 points, or -2.6%, while the S&P 500 lost nearly -3.0% and the NASDAQ Composite -3.6%. The yields on two-year and ten-year Treasury securities each rose by 12 basis points. There seems to be a sense on the Committee that policy is not as restrictive as previously thought with the Trump administration proposing a pro-growth policy agenda. Investor attention is now shifting from the outlook for interest rates to a focus on fiscal, trade, and immigration policies with the outlook for the economy soon to be in the hands of the Trump administration for the next couple years.

Higher Treasury Yields vs. Earnings Growth

As 2025 unfolds, the backdrop for common stocks still looks positive as a couple of the trends that powered common stocks higher remain in place, while others have largely played out, but do not appear to be poised to reverse and become headwinds to stock prices. However, the new year brings a new round of policy uncertainties that will only clear up as Congress and the Trump administration decide on a wide range of policy proposals.The economy looks to have grown at an above trend pace of 2.7% last year and enters 2025 with positive forward momentum supported by a slowing, but still solid jobs market, steady income growth, strong productivity gains, and healthy business capital spending spurred by artificial intelligence related investments. We continue to expect that the economy is on track for an elongated cycle, helped along by the surge in both business and household sentiment post-election and expectations of a business friendly policy agenda.

Operating earnings for the companies in the S&P 500 are expected to grow roughly 15% to 16% this year according to the analysts at Standard & Poor’s, with the economic expansion remaining on track and further gains in productivity. Look for earnings in the technology sector, communication services, and industrial companies driven by technology to continue compounding at a significant pace.

Common stocks tend to perform better when the Federal Reserve is gradually lowering rates because that means the economy and the financial markets are not under stress,

While recent inflation data have not been uniformly reassuring at face value with year-over-year readings closer to 3% rather than the Federal Reserve’s 2% target, digging into the reports and the November read on core PCE inflation indicate that the disinflation trend of the past two years has not reversed, but has clearly moderated. With the path to 2% not proving to be linear or tidy and concerns that certain policies of the Trump administration could keep inflation stubbornly high, interest rates and bond yields will likely remain higher than expected just a few months ago.

Despite inflation potentially remaining above the 2% target for the next year or two, a rekindling of inflationary pressures may not be the most likely scenario, as the labor market softened last year, and one-off spikes like used vehicle and egg prices will filter out of the data. Additionally, shelter inflation has started to slow and is expected to ease further as newly signed rental leases continue to roll into the data series, motor vehicle insurance inflation looks to be stabilizing as the outsized gains over the past three years have caught up to the increase in vehicle prices, and the Federal Reserve remains committed to positioning monetary policy to eventually bring inflation down to the 2% target. However, resurgent inflation cannot be ruled out as a risk, particularly in the event of excessively loose fiscal policy.

Which brings up the outlook for monetary policy. While the Federal Reserve cut rates by another 25 basis points at last month’s FOMC meeting, the Committee and Chair Powell acknowledged that the path forward is more uncertain given the strength in the economy and worries that inflation progress has stalled above the Federal Reserve’s 2% target. It would not surprise us if the Federal Reserve is on pause for an extended period of time.

Common stocks tend to perform better when the Federal Reserve is gradually lowering rates rather than aggressively cutting rates because that means the economy and the financial markets are not under stress, which would require a markedly easier monetary policy in short order. In that regard, the cautious shift in the rate outlook by the Federal Reserve at the December FOMC meeting could be viewed as good news for the outlook for common stocks this year.

While uncertainty about the future always seems to be high, policy uncertainty is particularly high currently. The incoming administration is supporting a wide range of ambitious policy outcomes, with little clarity on the actual policies. Mass deportations of illegal immigrants and closing the southern border could tighten labor market conditions and place upward pressure on wages and prices, but could also soften consumer demand.

Tariffs will likely raise the prices of imported goods, but could also squeeze profit margins, further strengthen the dollar, and weigh on household and business sentiment. Keep in mind, however, that during his first term President Trump was just as likely to use the threat of tariffs as a negotiating tactic as he was to actually implement them. A softer approach on regulation should boost business activity, productivity, and earnings, while tax cuts will support consumer and business spending, but could seriously widen the budget deficit and keep upward pressure on bond yields.

Change is in the wind with President-elect Trump returning to the White House with many campaign promises that he will attempt to fulfill, leaving businesses and the markets to figure out how the looming policy initiatives will alter the outlook for investment, growth, and inflation. Likewise, the Federal Reserve will need to navigate what the eventual set of policies passed by Congress will mean for growth and inflation.

Returns on common stocks this year will be determined by the tradeoff between higher Treasury yields and the ability of Corporate America to deliver a meaningful gain in earnings. Add in the Federal Reserve turning more cautious at the December FOMC meeting and we do not expect any further price-to-earnings ratio expansion in 2025. We expect that earnings will determine the path for stock prices this year.

We continue to view the aggressive rise in Treasury yields from the lows recorded in mid-September and the possibility of yields rising further as the biggest risks to common stocks over the next couple months. The major risk to stock prices over the next year or so would be the Federal Reserve needing to shift policy to a more restrictive stance to fight a rekindling of inflationary pressures, which would likely reset common stock prices lower.

Finally, do not be surprised if common stocks are hit with some selling pressure over the next couple weeks as investors in taxable accounts take some capital gains that were postponed from late 2024 to avoid paying capital gain taxes this coming April. Delaying taking gains pushed the tax burden out to April 2026. A growing economy, pro-growth policies, strong earnings, inflation within a range of 2% to 3%, and a central bank that will guide rates lower as inflation eases further should allow common stocks to regain their upward trajectory should a near term bout of volatility and selling pressure hit the market.

The yield on the ten-year Treasury note rose another 40 basis points last month to 4.58% and is now 94 basis points higher than the 3.64% yield the day before the September FOMC meeting. The 3.64% ten-year Treasury yield was then comprised of a 2.12% ten year inflation expectation and a real yield of 1.52%.

Currently, the 4.58% ten-year Treasury yield is comprised of a somewhat higher ten year inflation expectation of 2.35%, a rise of 23 basis points, while the real yield is higher by 71 basis points at 2.23%. The stronger economic data over the past three months and the expectation that President Trump’s economic agenda will be pro-growth and add to the national debt led to 76% of the rise in the ten-year Treasury yield since mid-September showing up as a higher real yield.

Despite inflation potentially remaining above the 2% target for the next year or two, a rekindling of inflationary pressures may not be the most likely scenario, as the labor market softened last year, and one-off spikes like used vehicle and egg prices will filter out of the data. Additionally, shelter inflation has started to slow and is expected to ease further as newly signed rental leases continue to roll into the data series, motor vehicle insurance inflation looks to be stabilizing as the outsized gains over the past three years have caught up to the increase in vehicle prices, and the Federal Reserve remains committed to positioning monetary policy to eventually bring inflation down to the 2% target. However, resurgent inflation cannot be ruled out as a risk, particularly in the event of excessively loose fiscal policy.

Which brings up the outlook for monetary policy. While the Federal Reserve cut rates by another 25 basis points at last month’s FOMC meeting, the Committee and Chair Powell acknowledged that the path forward is more uncertain given the strength in the economy and worries that inflation progress has stalled above the Federal Reserve’s 2% target. It would not surprise us if the Federal Reserve is on pause for an extended period of time.

Common stocks tend to perform better when the Federal Reserve is gradually lowering rates rather than aggressively cutting rates because that means the economy and the financial markets are not under stress, which would require a markedly easier monetary policy in short order. In that regard, the cautious shift in the rate outlook by the Federal Reserve at the December FOMC meeting could be viewed as good news for the outlook for common stocks this year.

While uncertainty about the future always seems to be high, policy uncertainty is particularly high currently. The incoming administration is supporting a wide range of ambitious policy outcomes, with little clarity on the actual policies. Mass deportations of illegal immigrants and closing the southern border could tighten labor market conditions and place upward pressure on wages and prices, but could also soften consumer demand.

Tariffs will likely raise the prices of imported goods, but could also squeeze profit margins, further strengthen the dollar, and weigh on household and business sentiment. Keep in mind, however, that during his first term President Trump was just as likely to use the threat of tariffs as a negotiating tactic as he was to actually implement them. A softer approach on regulation should boost business activity, productivity, and earnings, while tax cuts will support consumer and business spending, but could seriously widen the budget deficit and keep upward pressure on bond yields.

Change is in the wind with President-elect Trump returning to the White House with many campaign promises that he will attempt to fulfill, leaving businesses and the markets to figure out how the looming policy initiatives will alter the outlook for investment, growth, and inflation. Likewise, the Federal Reserve will need to navigate what the eventual set of policies passed by Congress will mean for growth and inflation.

Returns on common stocks this year will be determined by the tradeoff between higher Treasury yields and the ability of Corporate America to deliver a meaningful gain in earnings. Add in the Federal Reserve turning more cautious at the December FOMC meeting and we do not expect any further price-to-earnings ratio expansion in 2025. We expect that earnings will determine the path for stock prices this year.

We continue to view the aggressive rise in Treasury yields from the lows recorded in mid-September and the possibility of yields rising further as the biggest risks to common stocks over the next couple months. The major risk to stock prices over the next year or so would be the Federal Reserve needing to shift policy to a more restrictive stance to fight a rekindling of inflationary pressures, which would likely reset common stock prices lower.

Finally, do not be surprised if common stocks are hit with some selling pressure over the next couple weeks as investors in taxable accounts take some capital gains that were postponed from late 2024 to avoid paying capital gain taxes this coming April. Delaying taking gains pushed the tax burden out to April 2026. A growing economy, pro-growth policies, strong earnings, inflation within a range of 2% to 3%, and a central bank that will guide rates lower as inflation eases further should allow common stocks to regain their upward trajectory should a near term bout of volatility and selling pressure hit the market.

Treasury Market

Treasury Yields Rise Further

We continue to view the somewhat remarkable rise in Treasury yields since the Federal Reserve cut the target range for the federal funds rate by a larger than expected 50 basis points at the September 17-18 FOMC meeting as the most surprising, and potentially alarming, recent development in the financial markets. Expectations for stronger real growth, worries that inflation progress has stalled, concerns about the federal budget deficit and the massive supply of new issue Treasury debt that needs to be sold, and the Federal Reserve signaling that additional rate cuts are likely to be more cautious and gradual combined to push yields on Treasury securities even higher during December.The yield on the ten-year Treasury note rose another 40 basis points last month to 4.58% and is now 94 basis points higher than the 3.64% yield the day before the September FOMC meeting. The 3.64% ten-year Treasury yield was then comprised of a 2.12% ten year inflation expectation and a real yield of 1.52%.

Currently, the 4.58% ten-year Treasury yield is comprised of a somewhat higher ten year inflation expectation of 2.35%, a rise of 23 basis points, while the real yield is higher by 71 basis points at 2.23%. The stronger economic data over the past three months and the expectation that President Trump’s economic agenda will be pro-growth and add to the national debt led to 76% of the rise in the ten-year Treasury yield since mid-September showing up as a higher real yield.

We continue to view the somewhat remarkable rise in Treasury yields as the most surprising, and potentially alarming, recent development in the financial markets.

An analysis of the 70 basis point rise in the two-year Treasury yield to 4.25% from 3.55% the week following the September FOMC meeting is a bit different. The two year inflation expectation has risen by 38 basis points to 2.38% from 2.0% -- 54% of the rise in the two-year Treasury yield -- reflecting a fairly significant increase in the near term inflation outlook. The real yield has risen by 32 basis points to 1.87% from 1.55% -- 46% of the rise in the two-year Treasury yield.

The ballooning of the national debt over the past 20 years is quite alarming, growing from $7.4 trillion in 2004 to $36.2 trillion currently, with interest on the debt in FY 2024 at $950 million, larger than the entire defense budget of $826 billion. The interest cost of the debt is on a path to only increase as maturing Treasury securities are replaced with securities carrying higher interest rates and from annual budget deficits remaining close to $2 trillion. Higher real yields likely will be required by investors to fund the out-of-control national debt.

With the yield on the two-year Treasury note only 13 basis points below the 4.38% midpoint of the current target range of the federal funds rate, the market is not expecting a further material drop in the target range for the federal funds rate. This is consistent with our view that the Federal Reserve is about to pause the rate cuts and that the central bank could be on pause for an extended period of time. This somewhat more restrictive monetary policy stance should lower the odds of a flare up of inflationary pressures over the next year. If not, upward pressure on both real and nominal yields on two-year Treasury securities will likely emerge.

As we mentioned in the October ISS, in a steady state environment the yield on the ten-year Treasury note tends to settle in at a level near the growth rate of nominal GDP. An inflation rate and a real growth rate both in the range of 2% to 2.5%, would be consistent with a yield on the ten-year Treasury note in a range of 4.0% to 5.0%, which covers the current yield of 4.58%. Where the yield on the ten-year Treasury note trades over the next year will be determined by how the policy proposals of the Trump administration unfold and how they impact the economy, inflation, and the outlook for the budget deficit.

In this environment, investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve, while also modestly extending duration to lock in yields on intermediate term -- four to seven year -- fixed income securities. Even though yield spreads on both investment grade and non-investment grade corporate securities to Treasury securities are below average, it appears to be worthwhile to increase corporate bond exposure as we expect the soft landing scenario to continue to play out, with the economy in the early to middle stage of an elongated economic cycle. In this environment, yield spreads are not likely to widen to any significant degree.

The ballooning of the national debt over the past 20 years is quite alarming, growing from $7.4 trillion in 2004 to $36.2 trillion currently, with interest on the debt in FY 2024 at $950 million, larger than the entire defense budget of $826 billion. The interest cost of the debt is on a path to only increase as maturing Treasury securities are replaced with securities carrying higher interest rates and from annual budget deficits remaining close to $2 trillion. Higher real yields likely will be required by investors to fund the out-of-control national debt.

With the yield on the two-year Treasury note only 13 basis points below the 4.38% midpoint of the current target range of the federal funds rate, the market is not expecting a further material drop in the target range for the federal funds rate. This is consistent with our view that the Federal Reserve is about to pause the rate cuts and that the central bank could be on pause for an extended period of time. This somewhat more restrictive monetary policy stance should lower the odds of a flare up of inflationary pressures over the next year. If not, upward pressure on both real and nominal yields on two-year Treasury securities will likely emerge.

As we mentioned in the October ISS, in a steady state environment the yield on the ten-year Treasury note tends to settle in at a level near the growth rate of nominal GDP. An inflation rate and a real growth rate both in the range of 2% to 2.5%, would be consistent with a yield on the ten-year Treasury note in a range of 4.0% to 5.0%, which covers the current yield of 4.58%. Where the yield on the ten-year Treasury note trades over the next year will be determined by how the policy proposals of the Trump administration unfold and how they impact the economy, inflation, and the outlook for the budget deficit.

In this environment, investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve, while also modestly extending duration to lock in yields on intermediate term -- four to seven year -- fixed income securities. Even though yield spreads on both investment grade and non-investment grade corporate securities to Treasury securities are below average, it appears to be worthwhile to increase corporate bond exposure as we expect the soft landing scenario to continue to play out, with the economy in the early to middle stage of an elongated economic cycle. In this environment, yield spreads are not likely to widen to any significant degree.