Geopolitical Disequilibrium and the Path to Resolution in Iran

6/4/2026 - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

The dueling blockades the U.S. and Iran have put in place in the Strait of Hormuz have started three clocks ticking which will eventually lead to an end of the conflict. They do not indicate when a resolution to the conflict will be reached or whether the final agreement will achieve all of the U.S. objectives, however. They only indicate that a series of disequilibrium conditions exist, which will need to be resolved over time.

Dueling Blockades Will Eventually Lead to an End of the Conflict with Iran

The U.S. and Iran remained deadlocked during May in a high stakes standoff over control of the Strait of Hormuz, characterized by a U.S. naval blockade of Iranian ports and Tehran maintaining control over the international waterway crucial to the world’s energy markets. Iran’s ability to threaten neighboring Gulf states, which are both militarily vulnerable to direct attacks from Iran and economically important to the U.S., combined with Iran’s ability to effectively close the strait, have for now prevented the U.S. from forcing Iran to agree to its demands for an end to the conflict.

For most of May, President Trump dismissed Iranian peace proposals as unacceptable and described the fragile ceasefire, which has now lasted longer than the bombing campaign, as being on “massive life support.” Following his recent trip to China, President Trump announced he delayed a planned, major military assault on Iran at the request of Gulf allies to allow time for a diplomatic agreement. In response, Iran’s Revolutionary Guard (IRGC) threatened to extend the Middle East conflict “beyond the region” if the U.S. and Israel resume attacks on Iran.

Despite several military skirmishes over the past week, officials involved in negotiations with Iran to end the war report that the U.S. and Iran have “mostly agreed” to the terms of an agreement to temporarily end the three month old war and reopen the Strait of Hormuz, though there are differing accounts of some of the terms. As May comes to a close, President Trump has not yet signed off on the agreement, which would extend the ongoing ceasefire and start negotiations on the future of Iran’s nuclear program.

The dueling blockades the U.S. and Iran have put in place in the Strait of Hormuz have started three clocks ticking which will eventually lead to an end of the conflict. They do not indicate when a resolution to the conflict will be reached or whether the final agreement will achieve all of the U.S. objectives, however. They only indicate that a series of disequilibrium conditions exist, which will need to be resolved over time. The U.S. Navy’s blockade of the Strait of Hormuz for ships using Iranian ports in mid-April started two clocks ticking.

First, the U.S. blockade is costing Iran between $400 to $500 million a day, mostly in lost oil and petrochemical export revenue, significantly squeezing Iran’s economy by severing its primary revenue source. The blockade is severely straining the regime’s finances, making it difficult to pay government workers, military personnel, and, importantly, the members of the IRGC, the powerful political, military, and economic force that dominates Iran, defends the regime, and coordinates Iran’s war effort.

The loss of its primary source of hard currency has sent Iran’s currency, the rial, to record lows against the U.S. dollar, sending inflation soaring to over 50% according to the International Monetary Fund, and mass job layoffs have also been reported. Secondly, and possibly more important from a strategic perspective, as Iran runs out of oil storage capacity, it will be forced to shut in active wells, a costly and drastic measure that risks permanent damage to its oil fields, which could impair crude production for years to come.

The strategic shift by the U.S. to increase the economic pressure on Iran by blockading their ports and away from military pressure exposed Iran’s Hormuz vulnerability, giving the U.S. newfound leverage. The Iranian regime is weighing the cost of enduring the severe economic pain to achieve its military and geopolitical objectives and extract more concessions from Washington in the negotiations versus the threat that a crumbling economy and spiraling prices fuels a repeat of the nationwide anti-government protests that spread to over 200 cities across the country in January. The protests were the largest uprising in Iran since the 1979 Islamic Revolution and the ensuing crackdown left thousands of protesters dead.

The key consideration for the U.S. and the third ticking clock is that while oil prices did rise a little more than 70% compared to before the start of the war to around $112 per barrel in early April before ending May about 34% higher at around $87 per barrel, a massive surplus of crude oil in storage tanks, strategic reserves, and floating upon the high seas aboard oil tankers cushioned the rise in oil prices since the Strait of Hormuz was effectively closed three months ago. That surplus is now dwindling at a record pace as an estimated 13 to 14 million barrels per day of Middle East oil and refined products are not reaching the global energy markets on a daily basis.

Critical shortages of crude and refined products could emerge within weeks if the Strait of Hormuz remains closed to commercial shipping over the summer months. While the drawdown of the massive surplus and some demand destruction due to higher prices has bought some time and prevented energy prices from exploding higher, the loss of critical crude supplies has left little margin for error in the weeks ahead to avoid critically low levels of crude and refined products.

A surge in energy prices to new all-time highs is not out of the question if the global energy markets suffer a critical supply squeeze during the peak summer consumption period, driving inflation even higher across the globe. Reopening the strait is the only near term solution to the energy shortage. The U.S. is well aware that shrinking global inventories on a daily basis strengthen Iran’s negotiating leverage.

While the Iran/Hormuz situation dominated the attention of investors last month, an important summit meeting between the U.S. and China also took place. The expectations for President Trump’s state visit to China mid-month were admittedly low, however, the trip went a long way toward strengthening the fragile trade truce reached in October which suspended China’s proposed export controls on rare earth elements and other critical minerals in return for the U.S. lowering tariffs on Chinese imports.

Trade is obviously important to both sides and appears to be aligned around the goal of stabilizing the bilateral relationship between the two super powers, with trade seen as the most fruitful channel to accomplish this in the near term. The meetings also maintained the strategic positioning the U.S. has achieved in its trade agreements with China.

China boldly pressed its claims on Taiwan, but after the summit President Trump said the long-standing U.S. policy on Taiwan -- strategic ambiguity over independence for the democratic, self-governed island -- remains the same. President Trump suggested he and President Xi saw eye-to-eye on Iran, noting that China agreed that the Strait of Hormuz should remain a free waterway and that Iran should never have access to a nuclear weapon. However, it appears President Xi made no commitment to help bring about a resolution to the conflict, but did agree not to supply Iran with arms.

The U.S. and Chinese sides have only released a few details on specific trade agreements which were reached. However, President Trump did announce that China will order 200 Boeing aircraft, which is a major win in its own right. Keep in mind that the commitment by China to purchase jets from Boeing is actually a backdoor way to make sure that the U.S. has ongoing access to rare earth minerals for the manufacturing and technology sectors.

President Trump’s invitation to Mr. Xi to visit the White House on September 24 means the two leaders can talk in person again before the expiration of the one year trade truce set for October. President Xi said the U.S. and China agreed to “strategic stability” as a framework for the next three years -- the remainder of President Trump’s term in office -- according to state media.

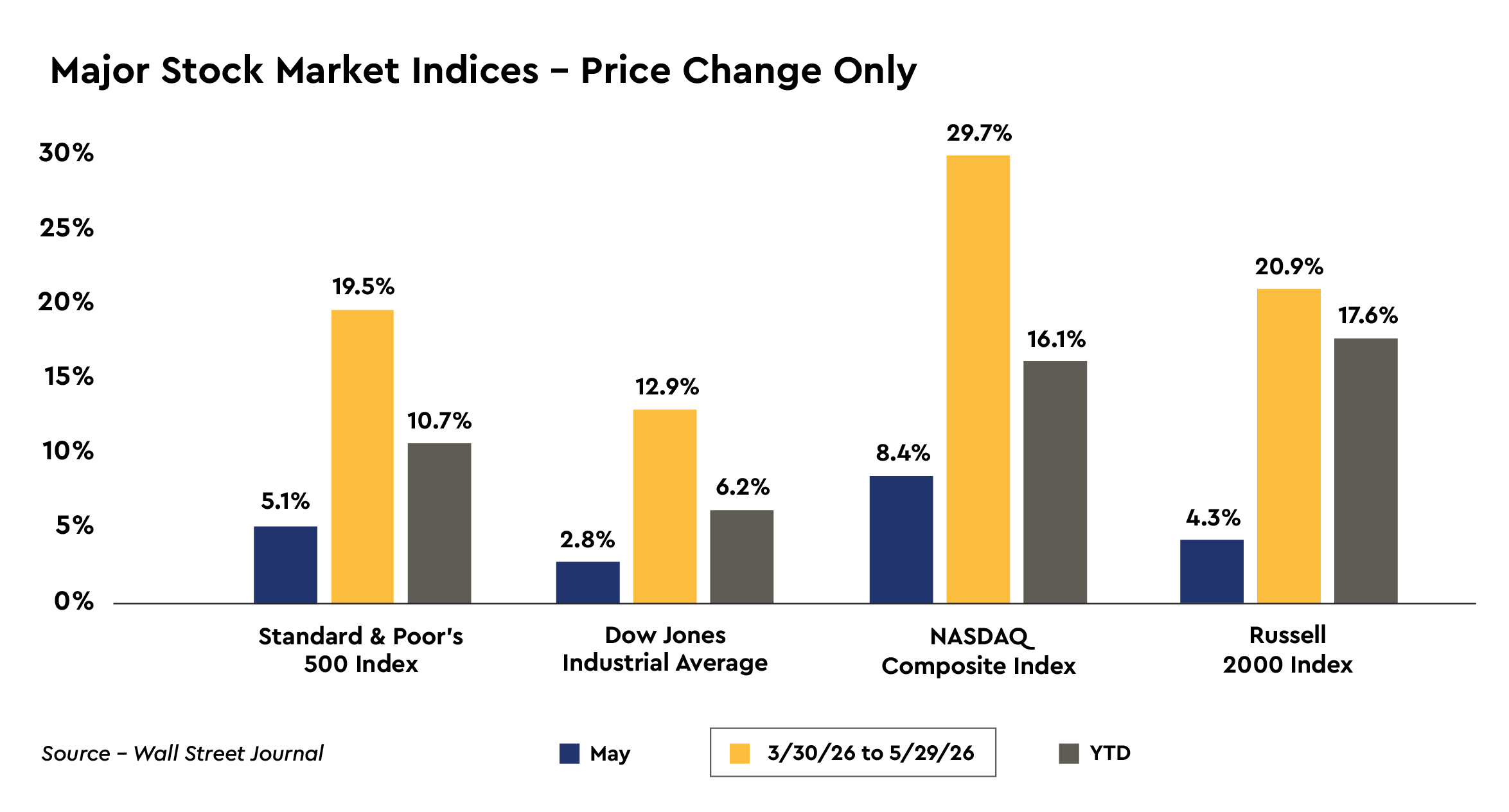

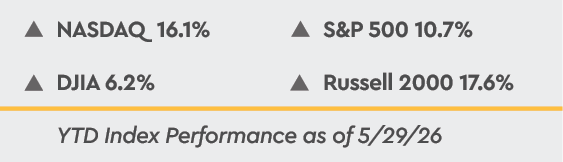

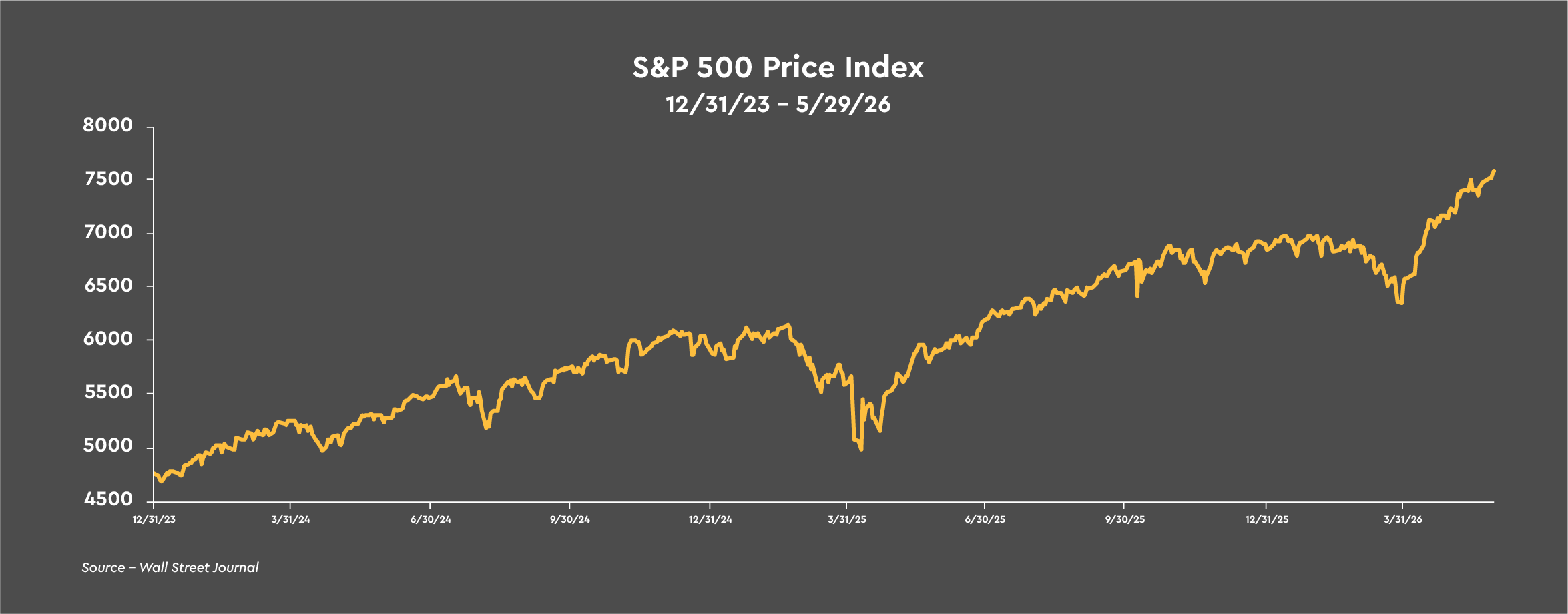

Investors continue to anticipate the U.S. and Iran eventually reaching a workable settlement to the conflict that reopens the strait and lowers energy prices with the S&P 500 advancing for nine straight weeks since the March 30 low. The S&P 500 gained 19.5% over that timeframe, reaching a series of new record highs. Stock prices posted strong gains for the second consecutive month during May as oil prices fell more than -14% and companies delivered strong earnings, led by technology companies. The major market measures rose 2.8% to 8.4% during May led by the NASDAQ Composite and are higher by 6.2% to 17.6% over the first five months of 2026 led by the Russell 2000 index of small company stocks.

The Kevin Warsh Era as Chair of the Federal Reserve Begins

Jerome Powell’s term as chair of the Federal Reserve ended on May 22, and Kevin Warsh’s era as the 17th chair of the central bank started. Mr. Warsh starts his second term at the Federal Reserve in a challenging environment with the inflation measures hitting their highest levels in three to four years and remaining stubbornly above the central bank’s 2% target for five years. Taken with a jobs market that is showing signs of stabilizing so far in 2026 after a significant downshift last year, this points to an FOMC Committee that is likely on hold for the foreseeable future.

Additionally, three of the five regional Federal Reserve Bank presidents that are currently voting members of the Committee opposed the messaging in the April 28-29 policy statement implying that further rate cuts could be ahead, instead preferring that the so-called “easing bias” in the statement be removed. While the three dissenting votes by the Bank presidents reflect mounting concerns that elevated energy prices and the compounding effects of tariffs could cause inflation pressures to become embedded more broadly across the economy, we also view the dissents as a declaration of independence that they will not be swayed by any attempts at political interference in the conduct of monetary policy.

The new chair spent 2025 constructing a case for the Federal Reserve to deliver the interest rate cuts President Trump wanted with an artificial intelligence boom delivering a productivity surge that would produce a “golden age” economy of rapid growth and falling inflation. His record during his first term at the Federal Reserve from 2006 to 2011, which covered the Great Financial Crisis, led most observers to characterize Chair Warsh as instinctively hawkish as he strongly opposed the second round of bond purchases in November 2010, ultimately leading him to resign from the Board in February 2011. As a result, investors and the markets are questioning if the new chair will bring a dovish or hawkish perspective to his new role.

We expect to see a return of Mr. Warsh’s hawkish orientation of his first term at the Federal Reserve as it aligns with his core beliefs and instincts, which we believe would be more consistent with the legacy he will want to build as chair of the Federal Reserve. Does Kevin Warsh want the legacy of Arthur Burns who is criticized for yielding to the political pressure of Richard Nixon and is often blamed for the 1970’s “Great Inflation,” or the legacy of Paul Volcker who is remembered for ending the chronic, debilitating inflationary spiral of the 1970’s and early 1980’s and for solidifying the central bank’s independence from political pressure, demonstrating that central banks can and should take policy actions that can be unpopular to ensure long-term economic stability?

Consider Mr. Warsh’s comments from his opening statement before the Senate Banking Committee on April 21. He made it very clear that “…monetary policy independence is essential.” He went onto to say that “Congress tasked the Federal Reserve with the mission to ensure price stability, without excuse or equivocation, argument, or anguish. Inflation is a choice, and the Federal Reserve must take responsibility for it.” Mr. Warsh concluded by stating that “I am committed to ensuring that the conduct of monetary policy remains strictly independent.” We are inclined to take Mr. Warsh’s statements at face value.

Federal Reserve independence is not merely an academic theory, it is a vital, practical policy dictum designed to protect long run U.S. prosperity from the short run pressures of election cycles. Elected officials are naturally inclined to prefer low interest rates to boost the economy, particularly before elections. Consistently low interest rates when the economy is already strong and/or inflationary pressures are building can result in damaging, high rates of inflation. Independent central banks have a proven track record of maintaining lower, more stable rates of inflation than those under direct political control of elected officials.

The minutes of the April 28-29 FOMC meeting confirmed that the Committee pivoted from considerations of additional rate cuts, which had dominated their deliberations for the past two years, to weighing the need to raise rates as the Iran conflict has reshaped the policy outlook. The minutes indicated that “many” officials would have preferred removing the easing bias from the policy statement, implying that the additional support could have come from voting members who wanted to strike the language, but were not prepared to dissent over it, or from the seven regional Federal Reserve Bank presidents who were not eligible to vote at the meeting.

The three dissents by the regional Federal Reserve Bank presidents and a careful review of the minutes of the April FOMC meeting clearly points to the center of the FOMC Committee moving to a neutral policy stance that Chair Warsh will need to confront head on at the June FOMC meeting. Mr. Warsh is on record that he is not in favor of “forward guidance” from the Committee and instituting that reform in June would allow the Committee to remove the easing bias in the policy statement without the shift becoming a contentious point of debate.

The Federal Reserve that Kevin Warsh is now leading remains in a difficult position as the oil shock resulting from the Iran conflict creates both downward pressure on growth, particularly on the majority of consumers that fall into the lower to middle income categories, and small businesses and upward pressure on inflation. We continue to expect no rate cuts any time soon because no matter how the data is viewed, inflation remains uncomfortably high and exceeded expectations in the inflation reports for April. The bond market is not going to tolerate wishful thinking of a “golden age” economy saving the nation from inflation. The bond market wants assurance that the Warsh-led Federal Reserve is serious about bringing inflation down to the central bank’s 2% target.

The futures market for the federal funds rate is looking for a rate hike by early 2027 with a growing probability of a second hike before the end of 2027. The Treasury market is also looking for a rate hike, if not two hikes, over the next twelve months or so with the yield on the two-year Treasury note finishing May at 4.01%, 38 basis points higher than the 3.63% mid-point of the current 3.50% to 3.75% target range for the federal; funds rates.

Higher Inflation and Treasury Yields versus Strong Earnings Growth

It seems to us that the building inflationary pressures and higher yields on Treasury securities are the biggest risks to common stocks over the next couple of months. The rise in energy prices resulting from the Iran war pushed the year-over-year rise in the CPI from 2.7% as 2025 came to a close to 3.8% at the latest reading for April. Without a reversal of the recent rise in energy prices in the near term, inflationary pressures will only rise, potentially on the back of even higher energy prices, but also from high energy prices bleeding into the costs of transportation, manufacturing, farming, and packaging, impacting virtually every good and service produced in the U.S. over time.

The yield on the ten-year Treasury note has risen from 4.17% at year end 2025 to 4.44% at the end of May, although the ten-year Treasury yield did hit 4.67% on May 19, its highest level since January of 2025 when investors were expecting the policy agenda of the Trump administration to bring about a significant acceleration of the economy’s growth rate. The higher Treasury yields are directly related to the higher inflation readings resulting from the surge in energy prices resulting from the supply disruption associated with the closure of the Strait of Hormuz. Higher Treasury yields lower the relative attractiveness of common stocks, while also working against the economy’s expected growth rate by negatively impacting the interest rate sensitive sectors of the economy, such as housing and motor vehicles.

Keep in mind that persistently higher inflationary pressures would eventually force the Federal Reserve to shift to a restrictive monetary policy if the higher rates of inflation look to be self-reinforcing by boosting inflation expectations. A tighter monetary policy could require a reset in the financial markets depending upon the extent to which inflation expectations rise. While the ten year inflation expectation embodied in Treasury securities has risen 12 basis points to 2.36% since before the start of the Iran war, they declined by -9 basis points during May as investors are looking for oil prices to fall before year end. So far, the markets are not expecting a materially tighter monetary policy or a reset in the markets, but that threat only grows the longer the Strait of Hormuz remains closed.

A resolution of the Iran conflict will reverse the rise in inflation and Treasury yields and reduce the risks they currently pose to the stock market. The three ticking clocks discussed above will eventually lead to an end of the conflict, the nature of the eventual agreement and the timing are unknown, however.

While investors faced several challenges over the past three months, once the initial shock of higher oil prices and the near term boost in inflation was digested, the focus returned to the fundamental outlook for common stocks, which ultimately comes down to the outlook for the economy and earnings. It remains our view that the economy remains in the midst of an elongated cycle, that hit a tariff speed bump during 2025 and an oil price shock so far in 2026.

Jobless claims, credit yield spreads, consumer spending, robust business capital spending, and a recent stabilization of the jobs market all point to positive growth in the economy, albeit at a slower pace than was expected at the beginning of the year. We expect the economy’s growth rate to pick up once a resolution to the Iran conflict has been finalized and oil prices fall. While a lengthy period of crude and refined product reserve building, global stockpiling, and logistical realignment will moderate the decline in energy prices for some time, lower energy prices are ahead.

A blistering pace of earnings growth has been a dominant theme for the stock market’s resilience so far this year despite the unsettling geopolitical headlines. Earnings growth has powered the gain in the S&P 500 over the first five months of 2026 as the increase in earnings has outpaced the rise in prices, resulting in the price-to-earnings multiple on the S&P 500 easing to 21.4x at the end of May versus 22.6x at the end of 2025. As the S&P 500 has hit record high after record high since mid-2024, earnings growth has driven all of the gain over the past two years rather than any price-to-earnings multiple expansion.

With 97% of the S&P 500 companies reporting, 1Q 2026 operating earnings rose a remarkable 21.5% on a year-over-year basis, compared to an expected first quarter growth rate closer to 14% at the beginning of the year. The consensus forecast provided by FactSet is for operating earnings to grow 22.8% over the four quarters of 2026, a truly significant advance. Robust productivity growth and a focus on efficiency by Corporate America generated an historic profit margin on operating earnings in 1Q 2026 of 16.7%, materially greater than the 8% to 9% profit margins of ten years ago. The outlook for continued growth in earnings remains positive, which should lead to higher common stock prices over time.

Fixed Income Looks More Attractive with the Backup in Yields

As fixed income investors price out the likelihood of rate cuts this year and price in higher rates of inflation in the near term, the attractiveness of fixed income securities has increased. The nominal yield on two-year Treasury securities has risen to 4.01% from 3.39% on February 27 before the start of the Iran war. Of that 62 basis point increase in yield, the real yield has increased 41 basis points, or 66% of the rise in nominal yields to 1.29%.

Likewise, at the longer end of the Treasury yield curve, the nominal yield on ten-year Treasury securities has risen to 4.44% from 3.95% on February 27. Of that 49 basis point increase in yield, the real yield has increased 37 basis points, or 76% of the rise in nominal yields to 2.08%. Historically, real yields on ten-year Treasury securities above 2.0% have been an attractive entry point for hold to maturity investors.

While Treasury yields could always bounce higher again if the current movement toward a temporary halt to the conflict with Iran falters and the strait remains closed into the summer months, the absolute level of the real yield on ten-year Treasury securities currently is among the highest that has been available since the aggressive tightening of monetary policy from March 2022 to July 2023.

Given our well documented concerns over the size of the federal budget deficit and the ballooning national debt that is currently carrying an interest expense of $1 trillion per year, we recommended intermediate term securities in the five to seven year range. Adding corporate securities to the mix will increase the real return on the fixed income portfolio. That medium term exposure can be barbelled with holdings at the shorter end of the Treasury yield curve which is still elevated due to the heavy insurance of Treasury bills to finance the federal budget deficit.