Common Stocks Advance Further During January, Led by Small Company Stocks

2/3/2026 (Updated: 2/24/2026) - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

Kevin Warsh’s nomination to succeed Jerome Powell as chair of the Federal Reserve is widely seen as removing a cloud over Federal Reserve independence that has been hanging over the financial markets and threatening to drive longer dated Treasury yields higher if a political pawn had been nominated.

Equity Markets

Common Stocks Advance Further During January, Led by Small Company Stocks

Common stocks opened January with a strong and broad-based rally as investors turned the page to a new year, buoyed by three rate cuts since September and a growing conviction that the pace of economic growth will accelerate and that the jobs market will strengthen this year. However, the advance in stock prices ran into some turbulence following the Department of Justice opening a criminal investigation into Federal Reserve Chair Jerome Powell, an apparent escalation by the Trump administration to pressure the central bank to further lower interest rates.

The criminal investigation is related to Mr. Powell’s Senate Banking Committee testimony last June on the renovation of Federal Reserve office buildings. In an unprecedented video statement following the receipt of the subpoenas, Chair Powell struck a defiant tone, asserting that the probe “is about whether the Federal Reserve will be able to continue to set interest rates based on evidence and economic conditions, or whether instead, monetary policy will be directed by political pressure or intimidation.” Mr. Powell went on to say that the subpoenas from the Justice Department are the result of longstanding frustration by President Trump over the Federal Reserve’s refusal to cut interest rates as quickly and as much as the President has demanded.

A criminal investigation of a sitting chair is without precedent and could backfire on Mr. Trump’s plans for the Federal Reserve. It could embolden certain governors and Federal Reserve Bank presidents to harden their views on the appropriate stance of monetary policy, asserting the independence of the central bank. The administration’s tactics could also motivate Mr. Powell to stay on as a governor until his term ends in 2028 after his term as chair runs out in May. Staying on would deprive the President of the ability to appoint another loyalist to the Board.

President Trump followed up the attack on Chair Powell by floating the idea to cap the interest rate on credit cards at 10% for one year as he pushes his recent messaging of making the cost of living more affordable for Americans. Stocks in the financial sector traded lower over concerns about earnings and a possible unintended consequence of limiting access to credit card debt for many households and small businesses. The concern is that financial institutions could be much more selective about only issuing credit cards to borrowers with the highest credit score, limiting the number of consumers and small businesses that might be eligible for getting credit.

President Trump also signed executive orders restricting large institutional investors from buying single-family homes and calling for restrictions on executive pay, dividend payments, and stock buybacks for defense companies. Administration officials also mentioned placing similar restrictions on other industries, such as large home builders and banks.

The President intensified his rhetoric on the U.S. gaining control of Greenland, threatening to impose additional tariffs on countries opposing the sale of the Danish territory to the U.S., raising fears about European trade retaliation and the stability of NATO. The new, punitive tariffs were scheduled to start at 10% on February 1 and rise to 25% on June 1. Stock prices fell following the threats to take control of Greenland by whatever means necessary, with the S&P 500 falling a little over -2% on January 20.

Stock prices remained under pressure until the President ruled out using force to acquire Greenland and called for immediate negotiations on the island’s status in his address to the World Economic Forum in Davos, Switzerland on January 21. Following what President Trump described as “a very positive discussion with the Secretary General of NATO,” he called off threatened tariffs on European nations as he said “the framework of a future deal” on Greenland was reached with NATO.

While specifics of the deal are still to be negotiated, it likely will involve access to mineral rights for the U.S. and its European allies, as well as, a focus on how NATO members can work together to safeguard Arctic security. The specific negotiations will aim to ensure “that Russia and China never gain a foothold -- economically or militarily -- in Greenland,” a NATO spokesman said. It appears President Trump followed a well established strategy of making strong, possibly audacious demands, threatening economic and/or military consequences if his demands are not met to gain maximum leverage, then reaching compromise once the opponent’s position has weakened.

As the month drew to a close, the markets had to digest a further rise in geopolitical tensions as President Trump threatened a major strike on Iran after preliminary discussions on limiting the country’s nuclear program and ballistic missile production failed to make progress, raising fears of oil prices jumping. New tariff threats on Canada and South Korea raised, once again, concerns over trade disruptions and higher prices on an array of imported goods.

Finally, last Friday President Trump nominated former Federal Reserve governor Kevin Warsh to be the next chair of the central bank once Jerome Powell’s term as chair is over in May. As covered later in this report, we look at Mr. Warsh as a good, experienced choice to lead the Federal Reserve, who will bring a pragmatic approach to conducting monetary policy with a clear understanding of the need to protect the central bank’s political independence.

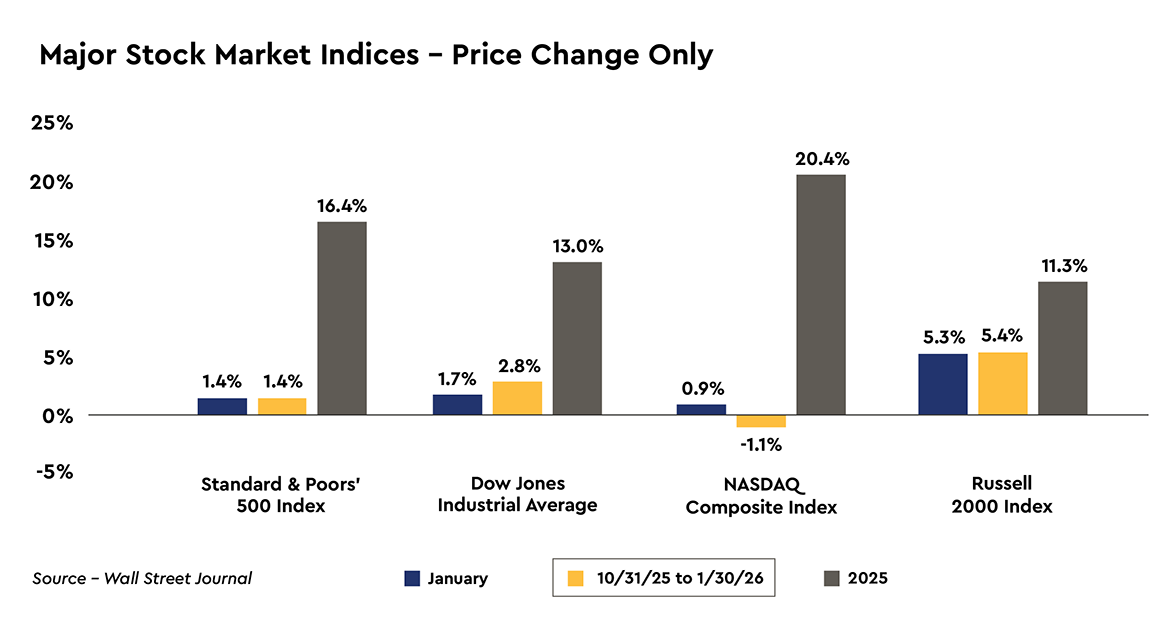

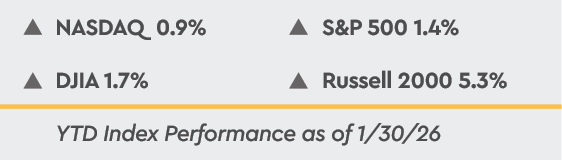

Despite President Trump hitting investors with a series of rapid fire moves during January, the large company stock market measures posted small gains while small company stocks were the big winner on the month. The NASDAQ Composite posted the smallest gain on the month at 0.9%, while the S&P 500 and the DJIA rose 1.4% and 1.7%, respectively. The Russell 2000 Index rose 5.3% during January and also led all the major stock market indices since the end of October with a gain of 5.4%.

Federal Reserve Enters New “Wait and See” Phase

As widely expected, the Federal Reserve left the target range for the federal funds rate unchanged at 3.5% to 3.75% at the January 27-28 FOMC meeting. It appears Federal Reserve policy has entered a new “wait and see” phase that will likely play out over the remainder of Jerome Powell’s term as chair as the FOMC Committee signaled little urgency to resume rate cuts. There were two dissents to the decision to leave rates unchanged, with Governors Waller and Miran wanting 25 basis point cuts.

We would characterize the tone of the policy statement and the press conference as suggesting the vast majority of the FOMC committee being very sanguine about the current positioning of monetary policy. The policy statement said that “economic activity has been expanding at a solid pace.” Importantly, the line on downside risks to employment was removed. We read that as, “no pressing need to lower interest rates.” The policy statement also stated that “Inflation remains somewhat elevated.” We read that as being supportive of leaving rates unchanged.

During the press conference, Chair Powell said, “There was broad support on the Committee for holding today, including among non-voters.” The Committee was very divided in December with three voters dissenting, but not all in the same direction. There were two “no” votes from regional Federal Reserve Bank presidents with four other nonvoting Bank presidents indicating that they did not support the decision to lower rates. Recent President Trump appointee, Stephen Miran, wanted a 50 basis point rate cut.

With Chair Powell stating that recent data pointed to a “clear improvement in the outlook for growth” since the December meeting and “some signs of labor market stabilization,” we think the Federal Reserve will be on hold through Mr. Powell’s final FOMC meeting as chair in April.

Kevin Warsh Picked to Succeed Jerome Powell

Last Friday, President Trump named former Federal Reserve governor Kevin Warsh to succeed Jerome Powell as chair of the Federal Reserve, ending a months-long saga that has seen unprecedented turmoil about the leadership at the central bank and its independence to conduct monetary policy. The financial markets had little reaction to Mr. Warsh’s nomination, a sign that investors view him as a credible steward of monetary policy who will pursue policy in a manner that is consistent with both sides of the Federal Reserve’s dual mandate, both maximum employment and price stability, rather than simply following President Trump’s preference for lower interest rates.

Kevin Warsh takes his new position at a time when the Federal Reserve is facing several challenges, including inflation still running above the central bank’s 2% target, the labor market slowing in a significant manner since last April, assessing how artificial intelligence is impacting the outlook for productivity and the labor market, responding to the emergence of digital currencies and their impact on the banking system, and the Federal Reserve facing unprecedented political pressure from President Trump to lower interest rates.

Mr. Warsh served at the Federal Reserve from 2006 to 2011, a critical period leading up to and ultimately through the Great Financial Crisis. During his time at the Federal Reserve, Kevin Warsh played an important role in the design and implementation of emergency lending programs aimed at stabilizing the economy and the financial markets. He supported the initial efforts to stabilize the credit markets with an unprecedented round of bond purchases known as quantitative easing.

However, he later broke ranks with then-chair Ben Bernanke and voted against the second round of bond purchases, warning that large scale asset purchases and an extended period of zero interest rates risked distorting the financial markets and undermining longer term price stability. This policy stance has bolstered his standing with investors wary of rising inflationary pressures and fiscal dominance -- keeping interest rates low to lower the costs of funding the national debt.

The nomination of Kevin Warsh will need Senate confirmation, a process that could be difficult given that Republican Senator Thom Tillis, the swing vote on the Senate Banking Committee, has said that he will block President Trump’s nomination of Mr. Warsh as Federal Reserve chair until the criminal probe of the current chair, Jerome Powell, is resolved. The ball is now in the court of the Department of Justice.

Leaving aside how the confirmation process will play out, Mr. Warsh’s nomination is widely seen as removing a cloud over Federal Reserve independence that has been hanging over the financial markets and threatening to drive longer-dated Treasury yields higher if a political pawn had been nominated. President Trump is likely appointing a Federal Reserve chair who may be no more inclined to bend to political pressure than Mr. Powell.

Things could well work out good for President Trump, however, if the new central bank chair is a pragmatist who conducts monetary policy with a degree of patience and steadfastness that lowers the inflation expectation embodied in Treasury yields, allowing nominal yields to decline over time, which will lower borrowing costs linked to Treasury yields, such as mortgage rates and the interest rate on auto loans.

Elongated Economic Cycles Are the Norm

Economic cycles in the U.S. since 1960 have been much longer than the three year average of ten expansions from the end of WWI to 1960 as long as inflationary pressures remain relatively well behaved. Leaving aside the highly inflationary period from 1971 to 1982 when the Federal Reserve had to step in several times to combat the worst inflationary pressures since WWII, the five business expansions since 1960 averaged 8.6 years, ranging from 6.1 years to 10.7 years.

While monetary and fiscal policy clearly played a role, we believe the inherent self-interest of participants in a capitalistic economy to grow and achieve higher standards of living lead to strong work ethics, higher levels of education and training, heavy funding of research and development, innovation, and creativity which drives efficiency and productivity leading to higher real wages and profits are the main drivers of elongated economic cycles.

Given these intrinsic dynamics of a capitalistic economy, it typically takes a significant exogenous event to break a cycle. Consider that the last three business expansions ended because of the collapse of the speculative dot-com bubble which coincided with a massive pullback in business capital spending in the aftermath of Y2K in 2001, the Great Financial Crisis precipitated by the subprime mortgage crisis which led to the plunge in housing prices and the value of mortgage-backed securities and the recession of December 2007 to June 2009, and the Covid-19 pandemic which led to the federal government mandated, sudden stop recession of 2020. In fact, we think the economic cycle of the 2010’s could still be in effect if not for the pandemic.

Based on our historical review and assessment of the current underlying fundamentals, it remains our view that the economy is in the midst of an elongated cycle that began in May 2020, but experienced a mid-cycle slowdown during 2Q and 3Q 2025, particularly in the labor market, due to the dramatic shift in tariff policy by the Trump administration. In response to the markedly higher tariff rates, domestic importers, distributors, and retailers attempted to force feed productivity gains into their businesses by slowing their hiring to a trickle from May to the end of 2025 while the volume of transactions and revenue continued to grow.

Being slow to hire, yet also slow to fire, led to a stall in the labor market, but not a contraction which could have led to a decline in consumer spending. Force feeding productivity gains in response to the sudden rise in the tariff burden allowed companies to expand profit margins on their existing business in order to absorb a good portion of the increased costs from the tariffs. The response by Corporate America last year is just the latest example of companies being incredibly adept at quickly adjusting to unexpected macro impacts, with overall profit margins actually increasing despite the higher tariffs.

In what appears to be an unintended consequence of the aggressive tariff policy, the labor market absorbed the largest portion of the tariffs in the form of diminished employment opportunities. With trade deals completed with most trading partners and the White House wanting a strong economy heading into the mid-term elections, we do not expect any major surprises on the tariff front over the remainder of the year. However, as January showed, tariff threats are always a possibility as President Trump continues to try to revamp the world order to his vision.

Currently, the economy’s growth rate is accelerating on the back of the continued AI buildout, business capital spending incentives, larger than normal tax refunds that will hit households in a couple months, moderating inflationary pressures, an accommodative monetary policy, lower Treasury yields, generally healthy credit conditions, and, hopefully, fading policy uncertainty flowing from Washington. Household purchasing power should continue to grow with less of that growth coming from new workers and more coming from higher real wages. Profit margins should continue to expand, combining with strong volume growth to produce a second consecutive year of above trend earnings growth.

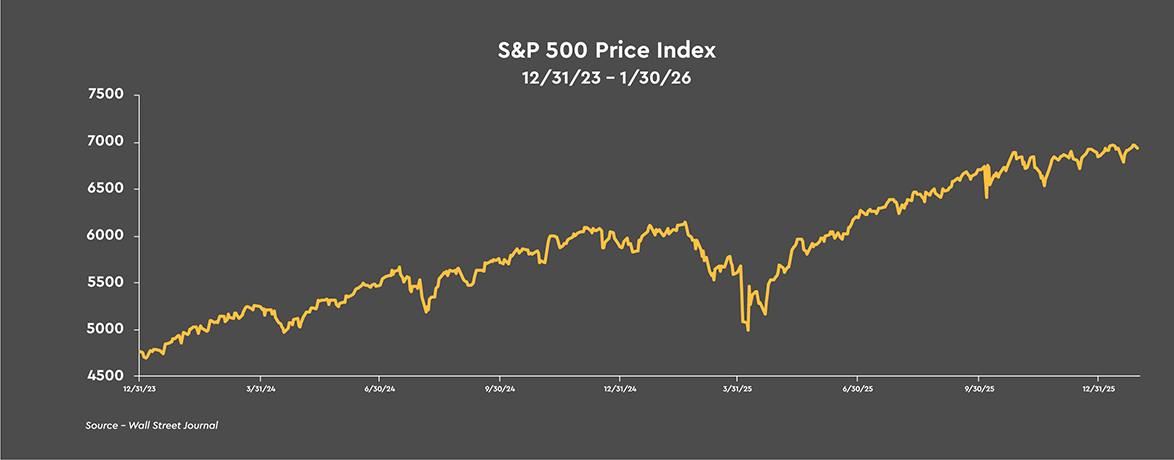

Since mid-2024, earnings growth has driven the current bull market rather than price-to-earnings multiple expansion and we expect that to continue this year. Earnings growth is closing out 2025 on a strong note. So far, with roughly 47% of the S&P 500 companies reporting, 4Q 2025 operating earnings are projected to have grown 17.4% on a year-over-year basis, which would result in a 13.7% gain for full year 2025. The analysts at Standard & Poor’s are forecasting operating earnings to grow almost 17% over the four quarters of 2026, which would be a significant advance.

The bull market is maturing in a very healthy manner, broadening out from the powerful, but narrow advance in the major stock market measures over the 2023 to October 2025 period led by a surge in the stock prices of the largest technology companies to now include the majority of publicly traded U.S. stocks. Finally, the nomination of Kevin Warsh to be the next chair of the Federal Reserve should allow investors to focus on corporate earnings and economic fundamentals, rather than political interference at the central bank.

Treasury Market

Treasury Yields and Inflation Expectations Rose During January

Yields on Treasury securities rose a touch last month with the two-year Treasury yield rising 6 basis points to 3.54% and ten-year Treasury yields climbing 7 basis points to 4.24%. While the two-year Treasury yield only rose 6 basis points, its components made rather large moves. The implied inflation expectation rose a whopping 63 basis points to 2.62% after declining -38 basis points during December, while the real yield fell -57 basis points.

It appears that the rise in geopolitical tensions last month along with new tariff threats on Canada and South Korea raised fears of oil prices jumping and higher prices on an array of imported goods, pushing near term inflation expectations higher.

Yields on two-year Treasury notes tend to lead the federal funds rate and the 3.54% yield currently is only slightly below the 3.63% midpoint of the current target range for the federal funds rate. As such, the Treasury market is anticipating only a small chance of a rate cut by the Federal Reserve over the next few months.

While near term inflation expectations rose sharply, longer term inflation expectations remained relatively well anchored with ten year inflation expectations rising 8 basis points on the month to 2.33%, accounting for more than the 7 basis point rise in ten-year Treasury yields.

It appears that the yield on ten-year Treasury notes is still being impacted by the yield on longer dated, overseas sovereign securities, which saw a significant rise during 2025 and remained at elevated levels during January. The yield on ten-year German bunds was largely unchanged at 2.85%, while the yield on Japan’s ten-year government bond rose another 18 basis points to 2.25%. The upward pressure on global sovereign bond yields is a result of widespread concerns over persistently large budget deficits across many countries, as well as expectations for a pickup in growth.

In the U.S., another year of a federal budget deficit around $1.8 trillion and our expectation for an acceleration in the economy’s growth rate lumps the U.S. yield dynamics in with other sovereign yields. Where the ten-year Treasury yield settles out in coming months will likely depend on yield levels on overseas sovereign bonds and from a tug-of-war between inflation pressures falling and the economy’s growth rate picking up some steam, resulting in an environment of nominal GDP running about 4.5% to 5.0%. Historically, the ten-year Treasury yield gravitates toward the economy’s nominal growth rate.

As such, we expect the yield on the ten-year Treasury note to be under modest upward pressure over the next few quarters, unless the economy’s growth rate disappoints in large measure from the economy’s 2% average annual growth rate since 1970. We are expecting an acceleration in the economy’s growth rate to a range of 2.5% to 3% in 2026 as the economy rebounds from the 2025 stall in the labor market.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve, largely due to the heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.