For Most of November, Caution Overrode Conviction

12/3/2025 (Updated: 4/3/2026) - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

Equity Markets

For Most of November, Caution Overrode Conviction

Investor sentiment in early November was weighed down by the lengthy shutdown of the federal government, with missed paychecks for the majority of federal employees and thousands of flights cancelled or delayed after the Federal Aviation Administration ordered flight cuts as air traffic control staffing shortages disrupted flights at several major airports. Concerns about the government shutdown, along with the squeeze on households from the elevated cost of necessities, were reflected in a University of Michigan survey in November which indicated that consumer sentiment fell to its lowest level in more than three years and just off its worst level ever.

Worries about the economy mounted after a report from Challenger, Gray & Christmas said that U.S. companies cut 153,000 jobs in October, nearly triple the level in September, and a total of 1.1 million jobs year-to-date, which is 65% higher than during the year ago period. Companies indicated that the reasons for the job cuts included rising costs (read that as tariffs) driving belt-tightening and hiring freezes, rising adoption of artificial intelligence tools, and weakness in warehousing with both consumers and businesses reducing spending.

We do not find it surprising that following the surge in flight cancellations and delays, along with a forecast from Transportation Secretary Duffy that air traffic would “slow to a trickle” ahead of the busy Thanksgiving holiday if the government shutdown continued, that the initial steps toward reopening the government were agreed to over the weekend of November 8-9. The ire of the public following widespread transportation delays, particularly in front of the most heavily travelled holiday of the year, and the mounting economic fallout from the shutdown brought sufficient political pressure on our elected lawmakers on Capitol Hill to end the shutdown. The more than six-week long government shutdown came to an end on November 12 when President Trump signed into law a bill that funded government operations through the end of January.

Following this resolution, investors turned their attention to the outlook for rate cuts, the release of some delayed data on the economy, and the outlook for returns on the massive artificial intelligence (AI) buildout.

Remarks by several Federal Reserve officials pointed to a divided FOMC Committee with a high degree of apprehension among its members over whether the central bank should deliver its third consecutive reduction in the federal funds rate from its current target range of 3.75% to 4.0% at the next policy meeting on December 9-10.

A growing number of Federal Reserve officials are of the opinion that it would be appropriate to hold rates steady for the time being with inflation running above the Federal Reserve’s target since 2021 and ongoing worries that tariff-related pricing pressures could be passed along to consumers next year. These officials argue that after two rate cuts this year, rates are at or near the neutral level that neither stimulates nor restrains the economy, making further rate cuts unnecessary, if not risky for bringing inflation back down to the 2% target.

Other officials are focused on the weakness in the labor market and view the current level of rates as modestly restrictive, seeing the need to get ahead of a further weakening in the economy’s forward momentum by easing policy further. Admittedly, it is impossible for the Federal Reserve to address concerns over tariff-related pricing pressures and softness in the labor market simultaneously.

The official labor market data drought ended last month with the release of the jobs report for September. Nonfarm payrolls rose a solid 119,000, up from a monthly average of 19,000 over the previous four months which was a time of unusual economic volatility spurred by President Trump significantly raising and/or imposing new tariffs on trading partners. The unemployment rate edged higher to 4.4% from 4.3%, the highest it has been since October 2021. However, the increase resulted from a sizable 470,000 increase in the labor force, which dwarfed a strong 251,000 increase in employment in the household survey, which is separate from the nonfarm payroll data from the establishment survey.

The Bureau of Labor Statistics (BLS) announced that it will not release a complete jobs report for October. Instead, the agency said October payroll data will be released along with a full labor report for November. BLS also said it was canceling the release of the October CPI report. The November jobs report will be released on December 16, six days after the Federal Reserve concludes its final policy meeting of the year, while the November CPI data will be released on December 18.

Investors also raised their concerns that the major hyperscalers (Amazon, Microsoft, and Alphabet being the top three) which provide cloud computing, networking, and internet services and run their own applications at a massive scale, plan to spend even more in 2026 on their artificial intelligence (AI) buildout than they did in 2025. While the hyperscalers funded much of their massive capital expenditures from 2023 to mid-2025 with free cash flow from their core businesses, in recent months several of the major hyperscalers have issued significant amounts of debt to help finance their AI ambitions.

As the AI buildout has reached levels few imagined just a couple years ago, the financial profile of some of the largest technology companies is evolving -- from business models that were cash rich and asset light to business models that supported heavy capital expenditures with increasing use of leverage in order to make a play for long term AI leadership. Accordingly, investors are increasingly wanting evidence that the magnitude of the expenditures to build out AI-powered products will be justified by future revenues and profit growth.

Some observers warn that the current rally in AI-related companies is beginning to resemble the dot-com bubble which occurred between roughly 1995 and 2000. While it will take time to see if the productivity promise from AI will actually evolve into a major revolution in the manner in which companies operate, and if the hyperscalers will be able to monetize their AI investments at a level which justifies the investment put into the buildout, there is an important fundamental difference between the current rise in AI-related stocks and the dot-com bubble, which is earnings.

The dot-com bubble was fueled by the growing popularity of the internet and a flood of venture capital into initial public offerings of speculative, often unprofitable startups, which with hindsight had fairly dubious business models. Today, the investments in the AI buildout are being made by the largest publicly traded technology companies which are generating massive profits on an annual basis, the vast majority of which has nothing to do with AI, making the decision to invest in the AI buildout easier.

Stock prices firmed late in the month after New York Federal Reserve Bank President John Williams, who is also vice-chair of the FOMC Committee, said that he expects the central bank can lower rates at the December FOMC meeting as labor market weakness currently poses a bigger threat than inflation as longer run inflation expectations remain in check and near their lowest levels on the year. Following his remarks, the probability of a rate cut rose to over 70%, and stock prices rose, which actually marked the low in stock prices on the month.

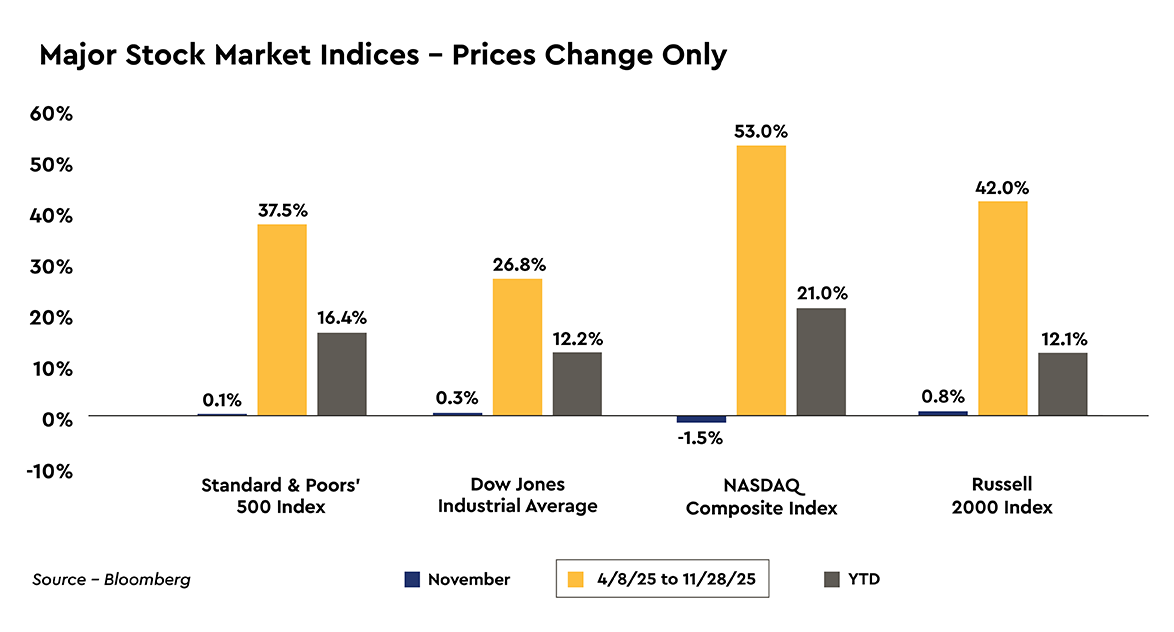

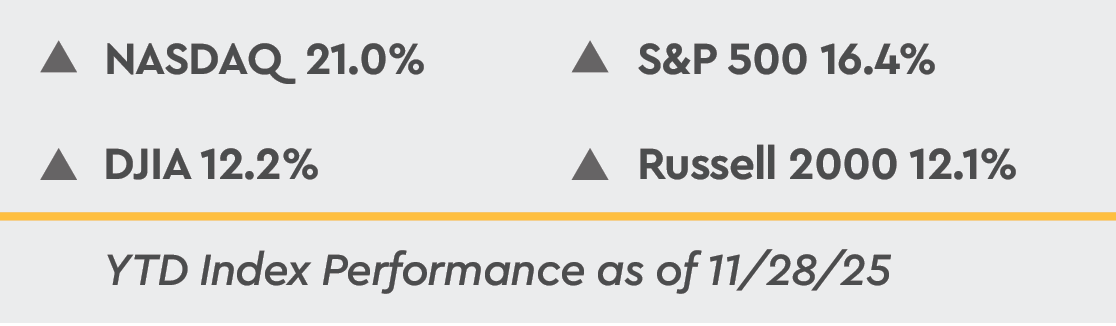

The pullback in AI-related stocks last month led to the technology-heavy NASDAQ Composite falling -1.5%, while the three other major stock market measures rose 0.1% to 0.8%. Over the first eleven months of the year, the major stock market indices are higher by 12.1% to 21.0% and are higher by an impressive 26.8% to 53.0% since the recent low in stock prices on April 8.

Look for the Economy’s Growth Rate to Re-Accelerate after the Spring to Fall Stall

It remains our view that the economy is in the midst of an elongated cycle. However, the new and/or much higher tariffs that the Trump administration hit the economy with over the spring and summer months brought about a mid-cycle slowdown as households turned defensive fearing job losses and higher prices, while businesses increasingly became hesitant to make hiring and investment decisions with the surge in uncertainty.

Keeping in mind that tariffs are ultimately a tax, the question is who pays the tax. Foreign manufacturers and exporters could pay the tax, but there is scant evidence of that occurring over the past few months. Consumers could pay the tax in terms of higher prices, and there is some evidence that a portion of the tax has shown up in higher prices for households. Finally, domestic importers and retail distributors could pay the tax, and we think that has led to the recent stall in the labor market.

It appears to us that domestic companies have attempted to force-feed productivity gains into their businesses by slowing their hiring to a trickle over the May to August timeframe while output continued to grow. This allowed companies to expand the profit margins on their existing businesses in order to absorb the increased costs from the tariffs, allowing them to largely maintain their overall profit margins despite the tariffs. In what appears to be an unintended consequence of the aggressive tariff policy, the labor market has absorbed the largest portion of the tariffs in the form of diminished employment opportunities.

We expected the pace of economic activity to pick up as 2025 drew to a close once the adjustment in staffing levels worked its way through the economy, however, the 43 day shutdown of the federal government likely delayed the reacceleration in the economy’s growth rate. We expect the economy to emerge from the tariff-related stall in early 2026 as the inherent dynamics of the US capitalistic economy manifest themselves and as the monetary and fiscal policy initiatives of 2025 take hold.

Consider the following list of supports for the economy. Continued growth in earnings is important as companies that are growing earnings are not under pressure to cut jobs, allowing households to maintain their incomes and spending levels. While companies could continue to force feed productivity gains by restraining employment growth into 2026, we think the majority of that adjustment has taken place.

On the earnings front, operating earnings on the S&P 500 in 3Q 2025 rose a huge 22% year-over-year and are forecast by the analysts at Standard & Poor’s to grow a solid 13% to 14% year-over-year in the current quarter. In our view the earnings benefit tied to deregulation and broadening AI-related productivity gains remains underappreciated, but analysts still expect operating earnings to post a gain on the order of 14% to 15% in 2026.

The shock from the tariff hikes is fading as businesses have been busy making the necessary adjustments, such as reconfiguring supply chains to the extent possible on short notice and the forced productivity initiative described above. Inflation should resume a trend toward the Federal Reserve’s 2% target as the one time tariff-related pricing pressures pass, wage growth slows, oil prices hover around $60 a barrel, and inflation-weary households continue to resist higher prices.

Business capital spending incentives in the tax and spending bill signed into law last summer and the ongoing momentum provided by the AI arms race that is driving massive transformative investments in semiconductors, data centers, and power systems will provide strong business investments again next year. The larger than normal level of income tax refunds from tax cuts retroactive to the beginning of 2025 will provide a boost to lower and moderate income households in early 2026.

Additionally, broad credit conditions appear healthy with credit yield spreads remaining tight. The Federal Reserve has delivered two rate cuts since September with additional cuts highly likely, along with ending the runoff of its bond portfolio, and Treasury yields are lower on the year bringing some relief on mortgage rates and other borrowing costs, such as car loans. Lastly, just a general fading of policy uncertainty should be broadly supportive of business and consumer confidence.

While the price-to-forward earnings ratio on the S&P 500 fell a touch last month at 22.2x on November 20 versus 23.4x in late October with the pullback in stock prices, it is still closer to the higher end of its range over the past five years and above its longer term average. However, we anticipate another year of above-trend earnings growth, and the productivity and efficiency of Corporate America is much greater today than ten years ago, let alone 20 to 30 years ago, with profit margins on the S&P 500 companies currently over 13% compared to 8% to 9% ten years ago.

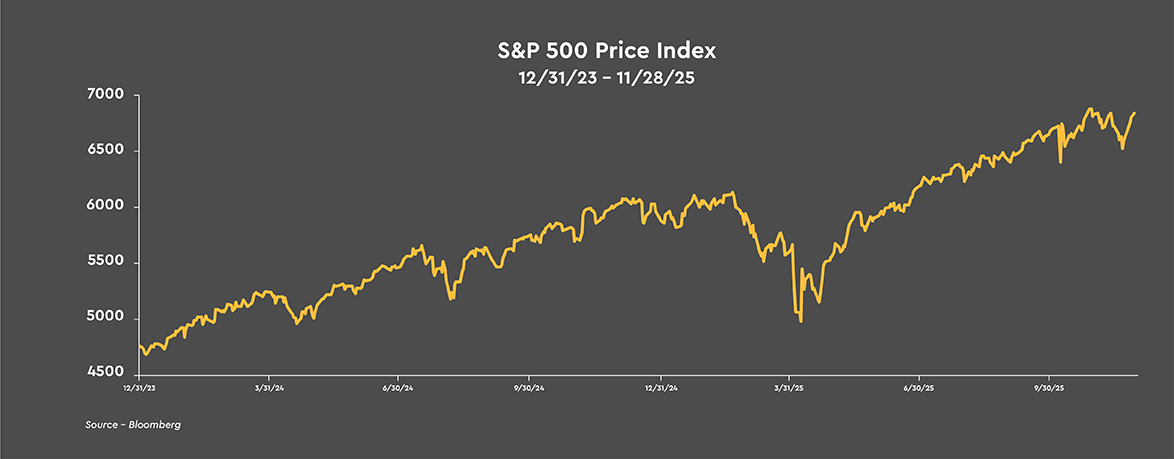

The roughly -5% pullback in the S&P 500 from the recent high on October 27 to the low on November 20 is actually a positive for the continuation of the bull market as it helps to keep stock prices from running materially ahead of the fundamentals. With the prospects for the pace of economic activity to accelerate as 2026 unfolds, the outlook for continued growth in earnings remains positive, which should lead to higher common stock prices over time.

Treasury Market

Treasury Yields and Inflation Expectations Fall Further

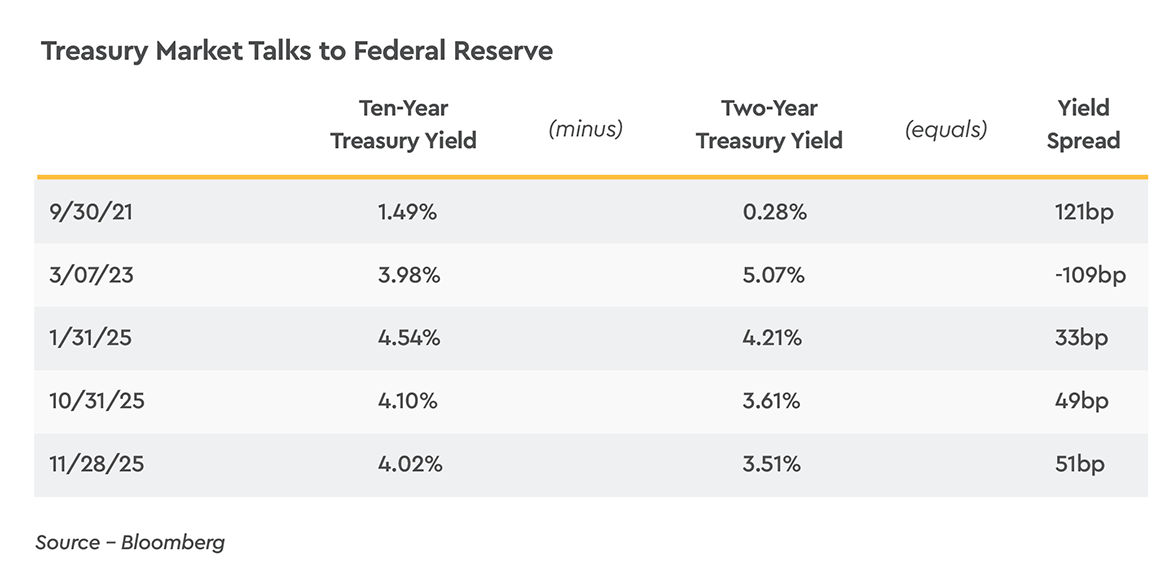

Yields on Treasury securities continued their 2025 trend lower during November, with declining inflation expectations pushing yields lower. The yield on the two-year Treasury note ended November at 3.51%, -10 basis points lower on the month and -74 basis points lower than at the end of 2024. The two-year inflation outlook fell -22 basis points to 2.37% last month, implying that the two-year real yield rose 12 basis points. The November moves in the components of the two-year Treasury are consistent with our view that the economy will reaccelerate in early 2026, and inflation will trend toward the Federal Reserve’s 2% target over the course of 2026.

The ten-year Treasury yield fell -8 basis points last month to 4.02% from 4.10% at the end of October with the ten-year inflation outlook easing further to 2.24% from 2.30% at the end of October. The decline in the inflation outlook is consistent with the view of New York Federal Reserve Bank President, John Williams, that longer run inflation expectations remain in check, part of his rationale that a December rate cut would be appropriate. The yield on the ten-year Treasury yield is lower by -56 basis points on the year.

Currently, the yield on two-year Treasury notes reflects between one to two rate cuts over the next couple months. Yields on two-year Treasury notes could drop a bit further in 2026 as the one-time price increases from tariffs roll off the inflation data, and the nation’s underlying inflation rate resumes its descent to the Federal Reserve’s 2% target. We also assume that the new chair of the Federal Reserve will attempt to take the policy rate to a more accommodative position, which could be closer to 3%.

Where the ten-year Treasury yield settles out in coming months will likely be the result of a tug-of-war between inflation pressures falling and the economy’s growth rate picking up some steam, resulting in an environment of nominal GDP running about 4.5%. Historically, the ten-year Treasury yield gravitates toward the economy’s nominal growth rate.

As such, we do not expect the yield on the ten-year Treasury note to trade consistently below 4% over the next few quarters, unless the economy’s growth rate disappoints in large measure from the economy’s 2% average annual growth rate since 1970. We are expecting an acceleration in the economy’s growth rate to a range of 2.5% to 3% in 2026 as the economy rebounds from the 2025 stall.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve, largely due to the heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.