A Shifting Market Finds Broader Support

7/9/2026 - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

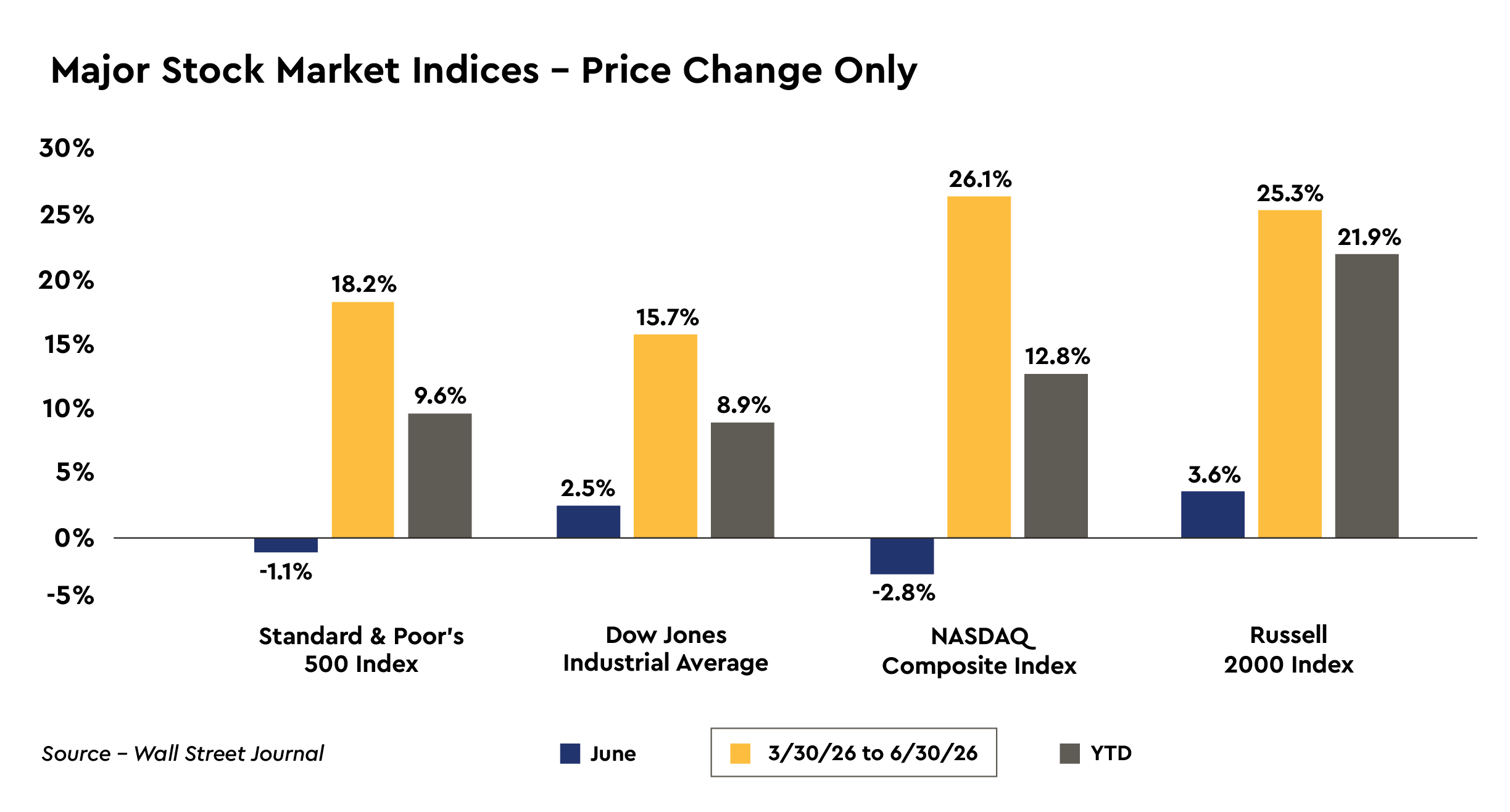

Stocks Deliver Mixed Returns During June

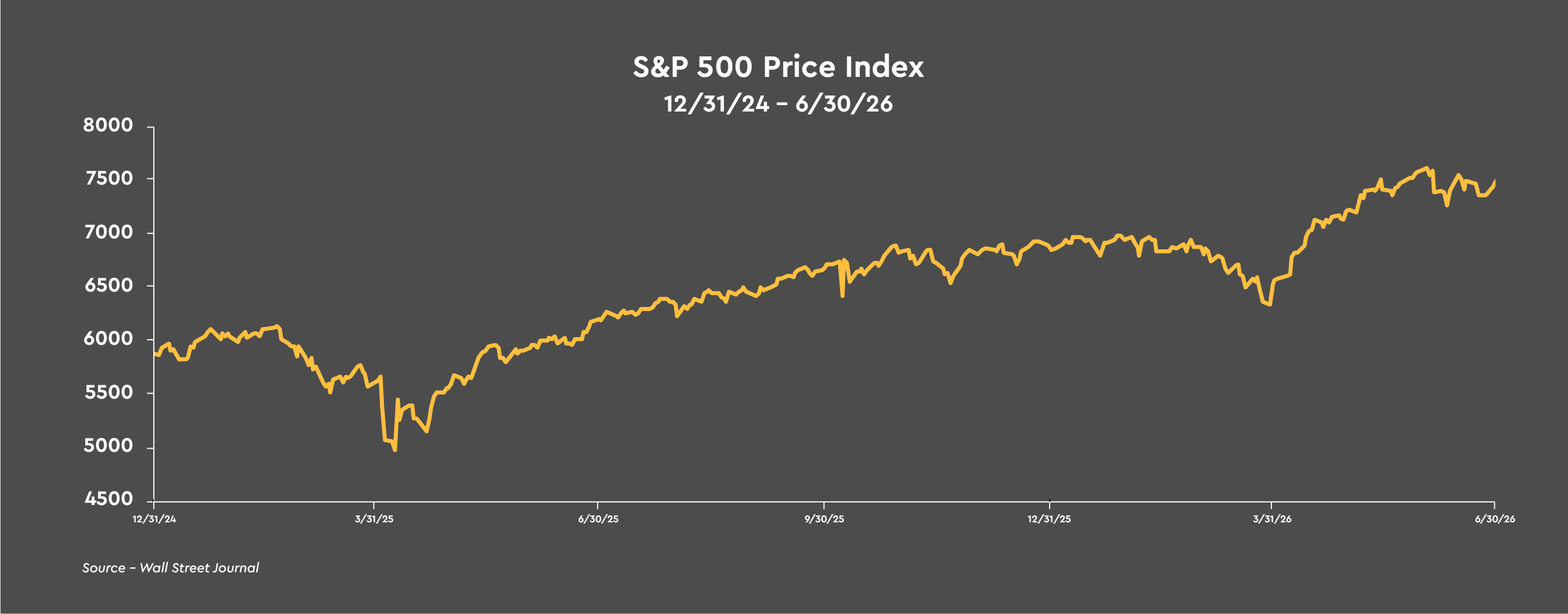

Following gains of 16.1% and 24.9% in the S&P 500 and the NASDAQ Composite during April and May, fears that the Federal Reserve could actually raise interest rates in the months ahead due to mounting inflationary pressures and a strong rebound in jobs growth over the past three months collided with renewed worries about the massive artificial intelligence outlays by the “Big Five” hyperscalers -- Amazon, Google, Microsoft, Meta and Oracle -- to bring about an abrupt end to nine weeks of gains over the first seven trading days of June.

The stock prices of several of the major technology giants that powered the market’s climb to record highs turned lower, as investors are increasingly wanting concrete evidence that the magnitude of the investments necessary to build out AI-powered products will be justified by future revenues and profit growth. The pullback gathered steam after a third straight monthly report of strong jobs gains raised new worries that the Federal Reserve might need to raise interest rates later this year to fight inflation, which exceeded 4% on the CPI for the first time in three years during May. The Federal Reserve reinforced these concerns over the path of interest rates at the June FOMC meeting by pivoting from an easing bias at the April meeting to a perceived bias to raise rates before year end.

Investors were also concerned that a wave of very large, privately-held technology companies were lining up to list publicly, led by SpaceX’s initial public offering carrying an historic $1.77 trillion initial valuation, with expectations that Open AI (ChatGPT) and Anthropic (Claude) would list within the next three to six months with rumored valuations approaching or exceeding $1 trillion each. The concern was that the early June weakness in stock prices could deepen as investors lightened up on some of what they owned to make room for the newly listed mega cap technology companies. Despite the worries, the SpaceX IPO successfully debuted on the NASDAQ on June 12 with the S&P 500 finishing June above its recent June 10 low.

The U.S. and Iran signed a memorandum of understanding, or MOU, on June 17 signaling a coordinated effort that could lead to the beginning of the end to the war that disrupted global trade and sent oil prices soaring. The MOU is essentially a 60-day ceasefire agreement during which Iran would reopen the Strait of Hormuz after the U.S. ends its blockade of Iran’s ports and lifts sanctions on its oil sales, providing the Iranian regime with much needed revenue to shore up its battered economy.

Iran also committed not to seek a nuclear weapon, which has been its stated position for over three decades, although the details of that commitment will be the subject of negotiations with the U.S. over the next two months. The MOU lays out the promise of extensive sanctions relief, restoring Tehran’s access to some of its estimated $100 billion in frozen assets, and a $300 billion fund to facilitate reconstruction and repair of war damage, all tied to Iran’s performance on U.S. demands regarding issues such as keeping the strait open and dismantling its nuclear program.

While the announcement of an agreement to begin the negotiations to end the war in Iran is great news and lifts the outlook for the world economy and the financial markets to the extent that it holds, a healthy level of skepticism must be maintained to see if the Iranian regime lives up to its end of the agreement and whether the U.S. can reach all of its objectives as the details of a workable and lasting peace agreement are hammered out.

With investors rethinking the costs and benefits of the data center buildout boom necessary to win the AI arms race, the growing likelihood that the next rate move by the Federal Reserve could be a hike, and the ongoing uncertainty over the extent to which Iran will be able to exert control over the global energy markets, the major stock market measures delivered a mixed array of returns last month.

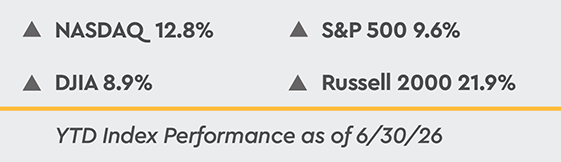

The DJIA and the Russell 2000 gained 2.5% and 3.6% during June and ended the month at new all-time highs. The S&P 500 and the NASDAQ Composite fell -1.1% and -2.8% last month and ended June -1.5% and -3.2% below their all-time highs. For the first six months of 2026, the major stock market indices generated strong gains of 8.9% to 21.9% with the Russell 2000 Index of small company stocks leading the way.

Ticking Clocks Led to a Heavily Scrutinized Memorandum of Understanding

Our biggest concern, in the near term, is how much negotiating leverage the U.S. has given up to begin negotiations with Iran to permanently end the conflict. The U.S. naval blockade of the Strait of Hormuz for ships using Iranian ports significantly squeezed Iran’s economy by severing its primary revenue source on the order of $400 to $500 million a day in oil revenue. This strain on the regime’s finances exposed Iran’s Hormuz vulnerability and is the primary reason Iran came to the bargaining table.

Allowing Tehran to sell its oil again removes the key leverage point the U.S. had achieved in negotiations through the naval blockade. We referred to this last month as one of three ticking clocks which would eventually lead to an end of the conflict. Additionally, the ability of Iran to close the strait again in short order does not bode well for long term stability in the Middle East and in the global energy markets.

The MOU is essentially a negotiated agreement to negotiate an agreement with all major issues being pushed to the 60 day negotiating period. The process of destroying and disposing of Iran’s highly enriched uranium stockpile and Iran’s ability to place tolls on ships passing through the Strait of Hormuz after the 60 day negotiating period are issues to be ironed out as the MOU is either silent or not explicitly clear on the topics. With U.S. military assets remaining in the Gulf region, the threat of the U.S. restarting the blockade of Iran’s ports could be the hammer the U.S. needs to regain leverage and achieve its objectives in the negotiations.

After signing the MOU, President Trump said he agreed to the MOU because continued war could have led to “economic catastrophe” as global oil reserves were on track to run out in about four weeks. This observation by the President is the third ticking clock we covered last month that shrinking global inventories of energy supplies could lead to new all-time highs in energy prices during the peak summer consumption period, driving inflation even higher across the globe, which would only strengthen Iran’s negotiating leverage each passing day. Mr. Trump went on to say that without the deal, “the alternative would be a worldwide depression” and the market “would go down at levels that nobody ever saw before, maybe except for 1929.”

These comments strongly suggest that the MOU was reached from the position of President Trump’s fear of higher oil prices and falling stock prices heading into the midterm elections. The result was the deal’s upfront sanctions relief on Iran’s oil sales and no corresponding hard commitment from Iran to dismantle its nuclear program.

As June drew to a close, Iran attacked two vessels attempting to cross the strait. The U.S. responded with strikes on Iranian military targets, while Iran escalated the flare-up by attacking U.S. military targets in Kuwait and Bahrain, placing the fragile ceasefire at risk and stalling the peace negotiations. Underlining the difficult backdrop to the negotiations, Iran is asserting that it has the sole authority to manage traffic in the Strait of Hormuz under the MOU and instructed ships wanting to cross the strait that they will have to register with Iran and sign up for a mandatory insurance policy, which has all the characteristics of a toll.

From the perspective of the U.S., the success of the negotiations, once they resume, hinge on Iran making concessions to the U.S. on the nuclear issue, relinquishing any notion of “controlling” the strait and therefore the world’s energy markets, and ending support for its “proxy forces” which are a network of armed non-state actors funded, trained, and equipped by the IRGC to project regional influence and counter U.S. and Israeli interests in the Middle East.

Since the signing of the MOU, Tehran has been trying to treat control of the Strait of Hormuz as the spoil of a successful, defensive war effort and is behaving as if it has the upper hand in negotiations because they doubt President Trump will risk a rebound in oil prices before the midterm elections. The U.S. could restart the blockade of Iran’s ports and stop Iran’s ability to sell its oil, resuming the severe squeeze on the Iranian economy to regain the upper hand in the negotiations, but at the cost of higher oil prices.

Time will tell which party has the effective leverage to turn the negotiations in their favor. For the time being, we can only monitor the broader security environment in the strait and the actual traffic going through it, both of which are key to maintaining oil prices close to the current $70 a barrel.

Chairman Warsh Commits to Deliver Price Stability

As widely expected, at Kevin Warsh’s first FOMC Committee meeting as chairman of the Federal Reserve on June 16-17, the Committee left the target range for the federal funds rate unchanged at 3.5% to 3.75%. The text of the policy statement was shortened dramatically and carried a hawkish tone. Key language indicating a bias toward future rate cuts was removed from the policy statement and Chairman Warsh repeatedly emphasized that officials are “unambiguously and unanimously” committed to bringing inflation down to the Federal Reserve’s 2% target.

The Committee did publish its quarterly Summary of Economic Projections, including the dot plot of forecasts about the path of interest rates. Chairman Warsh did not submit his own projections because he does not believe in the value of forward guidance. Of the 18 committee members who submitted forecasts, nine thought there could be at least one rate hike by the end of 2026, up from none in the SEP released at the March FOMC meeting.

The markets appeared to be surprised by the hawkish positioning of the FOMC committee, in general, and Mr. Warsh, in particular, as he attempted to establish his inflation fighting credentials up front, with stock and fixed income prices falling. The S&P 500 and the NASDAQ fell -1.4% and -1.6% after the release of the policy statement and the yield on the two-year Treasury note, which tends to rise and fall with changes in expectations for short-term rates set by the central bank, jumped 13 basis points to 4.20%, the highest level since February 2025.

Mr. Warsh unveiled a sprawling and ambitious endeavor encompassing five task forces which will rethink virtually everything done at the central bank to set policy and suggest what can be improved so that the FOMC Committee hits its 2% inflation target that they have failed to deliver for over 63 months. Each of the five task forces will address a different topic, including a comprehensive look at Federal Reserve communications, the size and composition of the Federal Reserve’s balance sheet, evaluate the use and relevance of existing data sources and consider methodological changes to improve data gathering, the impact of technology -- such as artificial intelligence -- on productivity and jobs in an era of transformation, and the Federal Reserve’s framework on inflation and its causes, but importantly, not the 2% target.

Each task force will include members both currently on the Federal Reserve staff and outside the Federal Reserve, and will include people “inside and outside the economics profession.” Chairman Warsh said the task forces will start with first principles, ask hard questions, examine current practices, consider alternatives, and ultimately propose next steps to be considered by policymakers. The task forces will begin their reviews in the next couple weeks with “hopefully most, if not all of them, concluding by year end.” The scope of the reviews reflect the breadth of Mr. Warsh’s reform ambitions.

In last month’s Investment Strategy Statement, we stated that we expected a return of Mr. Warsh’s hawkish orientation of his first term at the Federal Reserve rather than his more dovish posturing during 2025, when he was campaigning for the job, that the artificial intelligence boom would deliver a productivity surge that would produce a “golden age” economy of rapid growth and falling inflation that would be supportive of rate cuts.

Our outlook for policy is unchanged after Chairman Warsh’s first FOMC meeting. We continue to expect that policy will remain on hold for the foreseeable future, despite half of the committee members that provided forecasts looking for a rate hike before year end. The hawkish tone of the policy statement and Mr. Warsh’s tone during the press conference should lower inflation expectations.

Add in that we expect the May CPI inflation rate of 4.2% year-over-year to be the high water mark for the most recent inflation cycle following the tariffs of 2025 and the oil price shock of 2026, and we look for inflationary pressures to ease over the next year, lowering the need to actually raise interest rates. A Federal Reserve that is focused and steadfast in its mission to lower the nation’s inflation rate to the 2% target will eventually lead to lower Treasury yields which will lower the cost of borrowings tied to Treasury securities such as mortgages and car loans.

The Backdrop for Common Stocks Is Supportive of Higher Prices

While the S&P fell a modest -1.1% last month, major changes took place under the surface with a rotation into slower growing consumer, healthcare, and financial companies and less expensive value stocks, in general, and away from the narrow technology-focused, mega-cap monolith that drove stock index leadership over the past three years. Capital did not exit risk last month, it was reallocated into a much broader collection of stocks that are perceived to be undervalued, largely immune to artificial intelligence disruptions, and not at risk of returns on the artificial intelligence infrastructure buildout disappointing.

Data released during June suggested the economy, outside of the housing industry, is healthy and the growth rate appears to be accelerating. Consider that solid results were reported for both services and manufacturing purchasing managers’ surveys for May. The S&P Global manufacturing survey has expanded for eleven straight months, reaching its highest level in June since May 2022, reflecting the initial efforts to reshore manufacturing production to the U.S., the surge in capital spending associated with the buildout of data centers across the country, and the business capital spending incentives contained in last year’s tax and spending bill. With nonfarm payrolls adding 565,000 jobs over the past three months, the labor market is adding jobs at a healthy pace after registering basically no growth last year.

Geopolitical concerns have eased following the announcement of an agreement between the U.S. and Iran to begin negotiations to end the conflict, despite some healthy skepticism regarding how much leverage the U.S. has given up to get the deal done before the midterm elections. Inflationary pressures should ease as oil prices have fallen in a dramatic fashion since mid-May and Treasury yields appeared poised to drop over the next year as the Federal Reserve has strengthened its commitment to bring inflation down to its 2% target. These are all positive developments that are supportive of the economy and earnings.

Since mid-2024, earnings growth has driven the current bull market rather than price-to-earnings multiple expansion. Earnings growth started 2026 on a strong note with 1Q 2026 operating earnings on the S&P 500 companies growing a remarkable 21.7% on a year-over-year basis, according to FactSet, and are projected to grow more than 24% over the four quarters of 2026, a truly significant advance. With the significant rotations taking place in the stock market since the beginning of the year, valuations on mega cap technology companies have become more reasonable, falling more than the price-to-earnings ratio on the S&P 500 has dropped.

With credit yield spreads very tight to Treasury securities, initial claims for unemployment insurance at the midpoint of its range since late 2021, profit margins at historically wide levels and likely to widen further with the ongoing productivity gains, and earnings growing at very rapid rates, there appears to be very little risk of the economy falling into recession any time soon.

Inflation Expectations Collapse

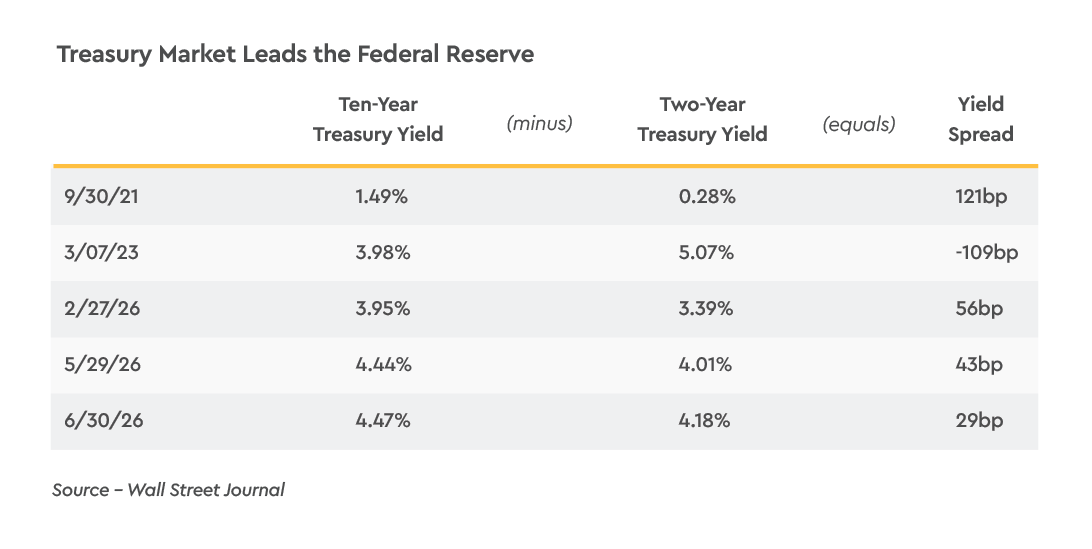

The stunning drop in oil prices during June and an unexpectedly hawkish FOMC meeting led to a collapse in inflation expectations last month. At the shorter end of the yield curve, the yield on two-year Treasury notes rose to 4.18% by the end of June from 4.01% on May 29, however, the inflation expectation over the next two years collapsed a stunning -42 basis points to 2.30% from 2.72% at the end of May. The real two-year Treasury yield rose to 1.88% from 1.29% at the end of May as the drop in oil prices boosted the growth outlook.Similar, but less dramatic shifts took place at the longer end of the Treasury yield curve as the yield on ten-year Treasury notes rose to 4.47% from 4.44% at the end of May as the ten-year inflation outlook fell -9 basis to 2.27%, reasonably close to the Federal Reserve’s 2% inflation target. The real ten-year Treasury yield rose 12 basis points to 2.20%.

While longer dated Treasury yields could always bounce higher again if the current negotiations to end the Iran war collapse and the Strait of Hormuz is closed with Iran and the U.S. restarting their respective blockades, the absolute level of the real yield on ten-year Treasury securities remains among the highest that has been available since the aggressive tightening of monetary policy from March 2022 to July 2023.

Given our well documented concerns over the size of the federal budget deficit and the ballooning national debt that is currently carrying an interest expense of $1 trillion per year, we recommend intermediate term securities in the five- to seven-year range. Adding corporate securities to the mix will increase the real return on the fixed income portfolio. That medium term exposure can be barbelled with holdings at the shorter end of the Treasury yield curve which is still elevated due to the heavy insurance of Treasury bills to finance the federal budget deficit.