Solid Growth in the Economy Sends Treasury Yields Higher

11/1/2024 (Updated: 2/25/2026) - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

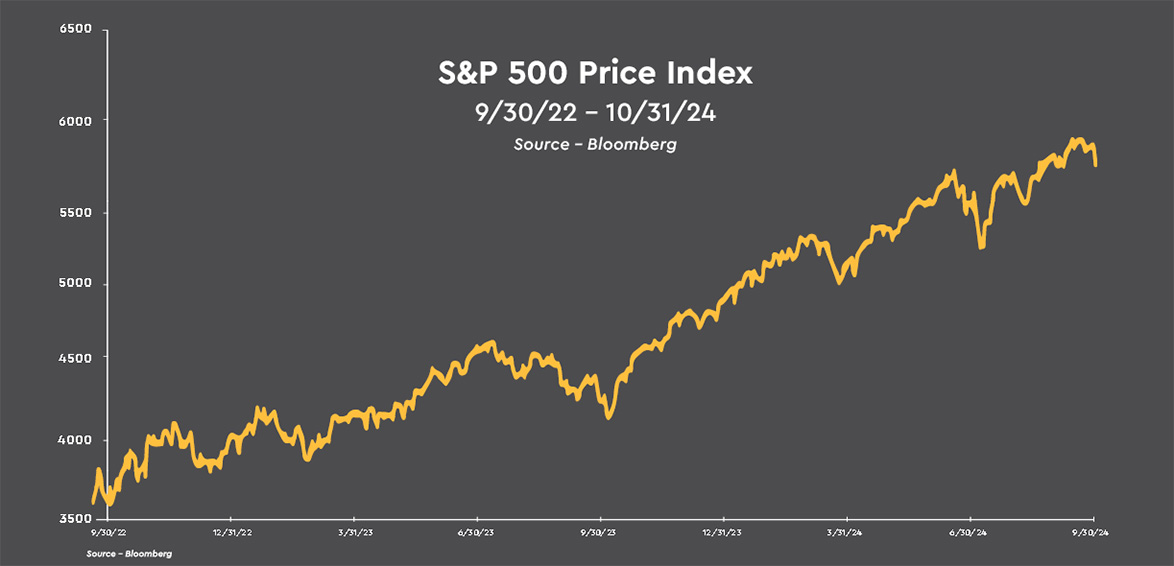

The stock market passed the two year anniversary of the start of this bull market last month, with the S&P 500 ending October 60% above its low on October 12, 2022. Given how poor investor sentiment was two years ago at the low and that the Federal Reserve continued to raise rates through July 2023, one could appropriately ask the question, “Why have common stocks risen over the past two years?”

Employers added 254,000 jobs during September, the largest monthly increase since March, with the unemployment rate dropping to 4.1% from 4.2%. The jobs report also indicated that hiring this summer wasn’t as slow as initially reported. Going into the employment report, job gains over the summer were reported to have averaged 116,000 a month, about half the pace of the previous twelve months. Revised figures showed employers added 72,000 more jobs in July and August combined than earlier reported. Taken with September, the last four months averaged jobs gains of 169,000, much closer to the 220,000 monthly average over the previous year.

Employers added 254,000 jobs during September, the largest monthly increase since March, with the unemployment rate dropping to 4.1% from 4.2%. The jobs report also indicated that hiring this summer wasn’t as slow as initially reported. Going into the employment report, job gains over the summer were reported to have averaged 116,000 a month, about half the pace of the previous twelve months. Revised figures showed employers added 72,000 more jobs in July and August combined than earlier reported. Taken with September, the last four months averaged jobs gains of 169,000, much closer to the 220,000 monthly average over the previous year.

With the South still working to recover from Hurricane Helene, Hurricane Milton barreled across Florida mid-month, leaving widespread devastation in its wake. The extent of the damage by Milton was mitigated somewhat by landfall taking place south of the heavily populated Tampa Bay metropolitan area and by the storm crossing the state fairly rapidly which lessened the amount of rainfall and shortened the period of heavy, damaging winds.

In addition to the loss of lives and billions of dollars of property damage caused by the storms, the data on the economy will be distorted in the months ahead. Upcoming data on jobs, production, retail sales, construction, and pricing pressures will require a thoughtful review as some data points will run above trend for a while and others below trend.

The economy continued to grow at a solid pace in 3Q 2024. Real GDP advanced at a 2.8% annual rate after growing at a 2.3% rate during the first half of the year. Consumer spending led the way growing at a 3.7% rate with outlays for goods higher at a 6.0% pace. Outlays for both durable and nondurable goods were helped along by goods prices falling at a -1.6% rate during the quarter, while real disposable personal income grew at a 3.2% annual rate as the labor market remained strong.

Business capital spending grew at a 3.3% rate with equipment outlays very strong at an 11.1% pace as companies are upgrading their equipment to keep pace with the latest advances in technology. Government spending made an unusually large contribution to the economy’s growth rate last quarter, largely from defense spending surging at a 14.9% rate which is largely related to the U.S. providing armaments to Israel and Ukraine. The one weak sector was residential construction outlays which fell at a -5.1% rate as housing affordability remains near all-time lows.

Possibly the best news in the report was inflationary pressures continuing to ease with core personal consumption prices rising at a 2.2% annualized rate last quarter and at a 2.7% rate on a year-over-year basis. Headline personal consumption prices rose at only a 1.5% rate in 3Q 2024 and rose 2.3% over the past year. On a broader perspective, the GDP price index rose at a 1.8% rate last quarter and rose 2.2% over the past four quarters.

Equity Markets

Solid Growth in the Economy Sends Treasury Yields Higher.

A better than expected jobs report for September altered the narrative around the trajectory for Treasury yields, the potential pace and extent of rate cuts by the Federal Reserve, boosted investors’ spirits, and lifted stock prices over the first half of the month as concerns about an imminent slowdown in the economy were alleviated. It was very good news that common stocks initially rallied on a strong jobs report as it confirms that investors are not overly concerned about a rekindling of inflationary pressures arising from the economy maintaining its forward momentum. Employers added 254,000 jobs during September, the largest monthly increase since March, with the unemployment rate dropping to 4.1% from 4.2%. The jobs report also indicated that hiring this summer wasn’t as slow as initially reported. Going into the employment report, job gains over the summer were reported to have averaged 116,000 a month, about half the pace of the previous twelve months. Revised figures showed employers added 72,000 more jobs in July and August combined than earlier reported. Taken with September, the last four months averaged jobs gains of 169,000, much closer to the 220,000 monthly average over the previous year.With the South still working to recover from Hurricane Helene, Hurricane Milton barreled across Florida mid-month, leaving widespread devastation in its wake. The extent of the damage by Milton was mitigated somewhat by landfall taking place south of the heavily populated Tampa Bay metropolitan area and by the storm crossing the state fairly rapidly which lessened the amount of rainfall and shortened the period of heavy, damaging winds.

In addition to the loss of lives and billions of dollars of property damage caused by the storms, the data on the economy will be distorted in the months ahead. Upcoming data on jobs, production, retail sales, construction, and pricing pressures will require a thoughtful review as some data points will run above trend for a while and others below trend.

The economy continued to grow at a solid pace in 3Q 2024. Real GDP advanced at a 2.8% annual rate after growing at a 2.3% rate during the first half of the year. Consumer spending led the way growing at a 3.7% rate with outlays for goods higher at a 6.0% pace. Outlays for both durable and nondurable goods were helped along by goods prices falling at a -1.6% rate during the quarter, while real disposable personal income grew at a 3.2% annual rate as the labor market remained strong.

Business capital spending grew at a 3.3% rate with equipment outlays very strong at an 11.1% pace as companies are upgrading their equipment to keep pace with the latest advances in technology. Government spending made an unusually large contribution to the economy’s growth rate last quarter, largely from defense spending surging at a 14.9% rate which is largely related to the U.S. providing armaments to Israel and Ukraine. The one weak sector was residential construction outlays which fell at a -5.1% rate as housing affordability remains near all-time lows.

Possibly the best news in the report was inflationary pressures continuing to ease with core personal consumption prices rising at a 2.2% annualized rate last quarter and at a 2.7% rate on a year-over-year basis. Headline personal consumption prices rose at only a 1.5% rate in 3Q 2024 and rose 2.3% over the past year. On a broader perspective, the GDP price index rose at a 1.8% rate last quarter and rose 2.2% over the past four quarters.

...Federal Reserve officials shifted their position a touch last month by speaking in favor of a more moderate pace of rate cuts than suggested following the September rate cut.

A consequence of the strong economic data released during October was a reversal of all of the decline in Treasury yields that accompanied the Federal Reserve’s 50 basis point rate cut in mid-September. Reflecting their data dependent approach to monetary policy, Federal Reserve officials shifted their position a touch last month by speaking in favor of a more moderate pace of rate cuts than suggested following the September rate cut.

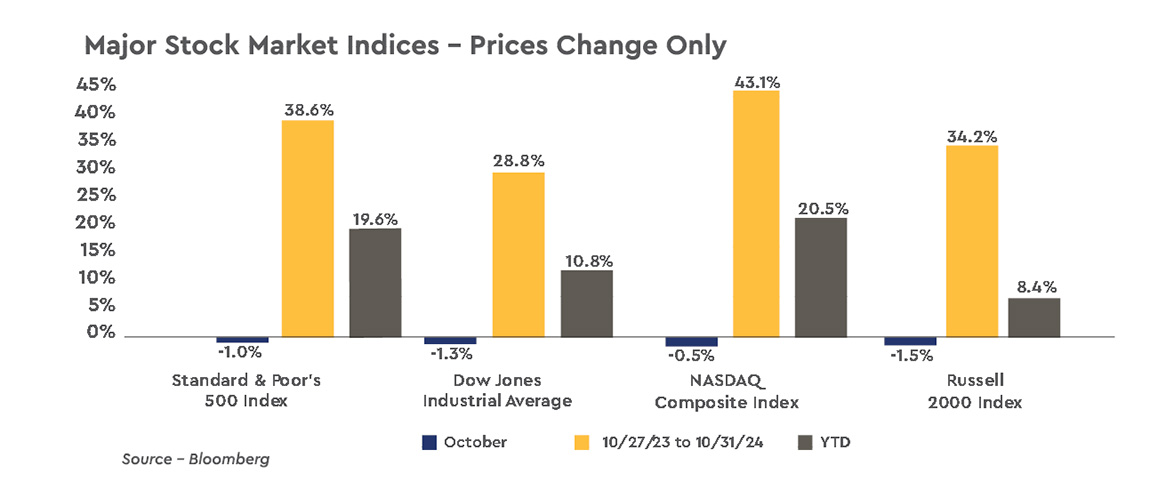

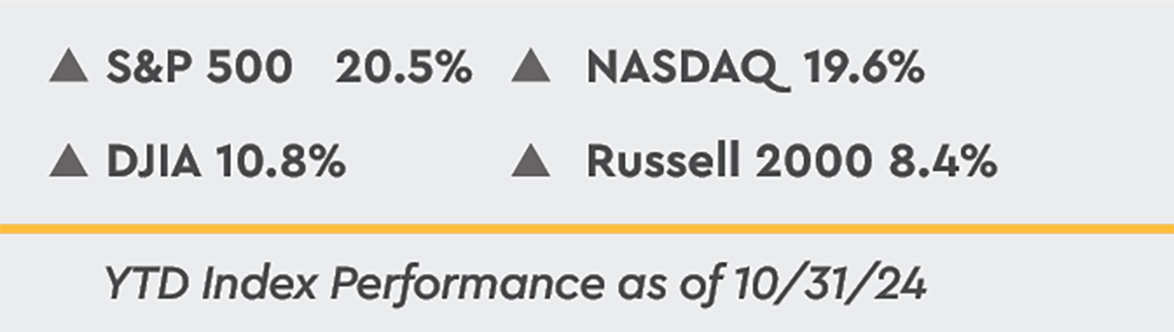

Common stocks gave back all of their gains from the first half of the month over the past two weeks as the persistent rise in Treasury yields weighed on investor sentiment. The four major stock market measures all posted small losses for October, on the order of -0.5% to -1.5%. On a year-to-date basis the NASDAQ Composite and the S&P 500 are higher by 20.5% and 19.6%, respectively, while the DJIA and the Russell 2000 Index of small company stocks continue to trail with gains of 10.8% and 8.4%.

The minutes of the Federal Reserve’s September 17-18 FOMC meeting indicated that perhaps there was more of a divide among Committee members over the extent to lower interest rates than portrayed by Chair Powell at the press conference. Although a substantial majority favored the larger 50 basis point cut that was ultimately approved, “some participants” would have preferred a smaller 25 basis point cut. The minutes emphasized that the larger rate cut was primarily aimed at recalibrating policy in light of inflation risks which had subsided and employment risks which appeared to have grown to a point that warranted “close monitoring.”

Federal Reserve officials asserted that the 50 basis point cut should not be viewed as a sign of concern over the economic outlook or “as a signal that the pace of policy easing would be more rapid.” Going into the September FOMC meeting, the economic data showed inflation steadily declining toward the Federal Reserve’s 2% target and the labor market cooling with the unemployment rate edging up to 4.2% from the 3.7% reading in January and jobs increasing about 116,000 a month over the summer, about half of the pace of the previous twelve months.

Common stocks gave back all of their gains from the first half of the month over the past two weeks as the persistent rise in Treasury yields weighed on investor sentiment. The four major stock market measures all posted small losses for October, on the order of -0.5% to -1.5%. On a year-to-date basis the NASDAQ Composite and the S&P 500 are higher by 20.5% and 19.6%, respectively, while the DJIA and the Russell 2000 Index of small company stocks continue to trail with gains of 10.8% and 8.4%.

Federal Reserve on a Gradual Path to a More Neutral Policy Stance

The minutes of the Federal Reserve’s September 17-18 FOMC meeting indicated that perhaps there was more of a divide among Committee members over the extent to lower interest rates than portrayed by Chair Powell at the press conference. Although a substantial majority favored the larger 50 basis point cut that was ultimately approved, “some participants” would have preferred a smaller 25 basis point cut. The minutes emphasized that the larger rate cut was primarily aimed at recalibrating policy in light of inflation risks which had subsided and employment risks which appeared to have grown to a point that warranted “close monitoring.”Federal Reserve officials asserted that the 50 basis point cut should not be viewed as a sign of concern over the economic outlook or “as a signal that the pace of policy easing would be more rapid.” Going into the September FOMC meeting, the economic data showed inflation steadily declining toward the Federal Reserve’s 2% target and the labor market cooling with the unemployment rate edging up to 4.2% from the 3.7% reading in January and jobs increasing about 116,000 a month over the summer, about half of the pace of the previous twelve months.

A review of the data suggests the risks to the labor market are far less worrisome that they previously appeared.

The strong September jobs report, the solid report on the economy for the third quarter, and significant upward revisions to estimates of household income, corporate revenue, and savings rates for 2022 through 2Q 2024, virtually closed the door on another 50 basis-point rate cut by the Federal Reserve at its meeting November 6th-7th, the day after the presidential and congressional elections. A review of the data suggests the risks to the labor market are far less worrisome that they previously appeared.

How might the stronger economic data impact the pace and extent to which the Federal Reserve will lower interest rates? The central bank remains data dependent, and the stronger data will likely moderate the pace of rate cuts. However, we expect the rate cutting cycle to continue into 2025 as the minutes reinforced what Federal Reserve officials have consistently stated over the past few months, that with inflation continuing to approach the 2% target and the jobs market slowing, but not slow, “it would likely be appropriate to move toward a more neutral stance of policy over time.”

The big unknown is what level of the target range for the federal funds rate is consistent with a neutral policy stance. With the federal funds rate at roughly 4.88% and inflation near 2% depending upon which inflation measure is used, a real federal funds rate just shy of 3.0% would appear to be consistent with policy still being restrictive at the current level of interest rates. As we have stated previously, it will only be with the clarity of hindsight that the extent to which policy is restrictive will be known.

We expect the Federal Reserve to move gradually, as long as the data continue to point to the economy maintaining its forward momentum and the jobs market not deteriorating in a material manner. The obvious risk the central bank faces in keeping rates in a restrictive posture for too long is the current soft landing giving way to a broader slowdown in the economy which currently would serve no useful purpose with inflation near 2% and the labor market slowing over the past year. We expect no more than four additional rate cuts to June of next year given the forward momentum in the economy currently.

Chair Jerome Powell appears to be committed to solidifying two parts of his legacy as the leader of the Federal Reserve. One is that the post-pandemic surge in inflation was tamed in an effective and relatively timely fashion. That goal has largely been achieved. The other is that taming inflation did not require pushing the economy into a recession, rather that a soft landing took place. Mr. Powell is hoping that beginning to remove some of the policy restrictiveness while the economy and employment are still relatively strong will act as an insurance policy against a hard landing for the economy.

The stock market passed the two year anniversary of the start of this bull market last month, with the S&P 500 ending October 60% above its low on October 12, 2022. Given how poor investor sentiment was two years ago at the low and that the Federal Reserve continued to raise rates through July 2023, one could appropriately ask the question, “Why have common stocks risen over the past two years?”

The answer is that investors spent the past two years pricing out significant macroeconomic risks such as fears of inflation remaining stubbornly high in a range of 3% to 4%, leading to an even more restrictive policy stance by the Federal Reserve, and the economy and company earnings suffering through a deep and prolonged recessionary period.

For 2023 and so far in 2024, investors priced in the likelihood that disinflationary influences would become the dominant trend in the economy as supply chain disruptions were repaired and commodity prices reversed their climb precipitated by Russia invading Ukraine. Additionally, the surge in housing prices eased as affordability conditions reached their worst level in four decades and the Federal Reserve took the edge off inflationary pressures by raising borrowing costs to their highest level in two decades.

This turn of events raised the likelihood of the Federal Reserve bringing the economy in on a soft landing rather than a recession, that the Federal Reserve was approaching an end to the rate hiking cycle and that a rate cutting cycle would commence to remove a degree of restrictiveness that was no longer necessary. Treasury yields fell from their October 2022 highs and the probability increased that an elongated business cycle could develop, which would support an extended earnings cycle following the downturn in operating earnings for the S&P 500 in 2022.

How might the stronger economic data impact the pace and extent to which the Federal Reserve will lower interest rates? The central bank remains data dependent, and the stronger data will likely moderate the pace of rate cuts. However, we expect the rate cutting cycle to continue into 2025 as the minutes reinforced what Federal Reserve officials have consistently stated over the past few months, that with inflation continuing to approach the 2% target and the jobs market slowing, but not slow, “it would likely be appropriate to move toward a more neutral stance of policy over time.”

The big unknown is what level of the target range for the federal funds rate is consistent with a neutral policy stance. With the federal funds rate at roughly 4.88% and inflation near 2% depending upon which inflation measure is used, a real federal funds rate just shy of 3.0% would appear to be consistent with policy still being restrictive at the current level of interest rates. As we have stated previously, it will only be with the clarity of hindsight that the extent to which policy is restrictive will be known.

We expect the Federal Reserve to move gradually, as long as the data continue to point to the economy maintaining its forward momentum and the jobs market not deteriorating in a material manner. The obvious risk the central bank faces in keeping rates in a restrictive posture for too long is the current soft landing giving way to a broader slowdown in the economy which currently would serve no useful purpose with inflation near 2% and the labor market slowing over the past year. We expect no more than four additional rate cuts to June of next year given the forward momentum in the economy currently.

Chair Jerome Powell appears to be committed to solidifying two parts of his legacy as the leader of the Federal Reserve. One is that the post-pandemic surge in inflation was tamed in an effective and relatively timely fashion. That goal has largely been achieved. The other is that taming inflation did not require pushing the economy into a recession, rather that a soft landing took place. Mr. Powell is hoping that beginning to remove some of the policy restrictiveness while the economy and employment are still relatively strong will act as an insurance policy against a hard landing for the economy.

Disinflation, Continued Growth in the Economy and Earnings, and Rate Cuts Ahead

The stock market passed the two year anniversary of the start of this bull market last month, with the S&P 500 ending October 60% above its low on October 12, 2022. Given how poor investor sentiment was two years ago at the low and that the Federal Reserve continued to raise rates through July 2023, one could appropriately ask the question, “Why have common stocks risen over the past two years?”The answer is that investors spent the past two years pricing out significant macroeconomic risks such as fears of inflation remaining stubbornly high in a range of 3% to 4%, leading to an even more restrictive policy stance by the Federal Reserve, and the economy and company earnings suffering through a deep and prolonged recessionary period.

For 2023 and so far in 2024, investors priced in the likelihood that disinflationary influences would become the dominant trend in the economy as supply chain disruptions were repaired and commodity prices reversed their climb precipitated by Russia invading Ukraine. Additionally, the surge in housing prices eased as affordability conditions reached their worst level in four decades and the Federal Reserve took the edge off inflationary pressures by raising borrowing costs to their highest level in two decades.

This turn of events raised the likelihood of the Federal Reserve bringing the economy in on a soft landing rather than a recession, that the Federal Reserve was approaching an end to the rate hiking cycle and that a rate cutting cycle would commence to remove a degree of restrictiveness that was no longer necessary. Treasury yields fell from their October 2022 highs and the probability increased that an elongated business cycle could develop, which would support an extended earnings cycle following the downturn in operating earnings for the S&P 500 in 2022.

More recently, investor sentiment has received a boost from the growing odds of divided government in Washington following this month’s presidential and congressional elections...

Simply put, common stocks prices are higher over the past two years due to disinflationary influences taking hold in the economy, no recession, the start of a rate cutting cycle, and a generally supportive backdrop for earnings. More recently, investor sentiment has received a boost from the growing odds of divided government in Washington following this month’s presidential and congressional elections which raised hopes that the policy positions of the extreme corners of both parties were unlikely to come to fruition.

The markets are on heightened alert, and small negative or positive shifts in the perception of the economy’s health are being magnified in terms of volatility in stock prices and fixed income yields. It appears to us that the economic data is consistent with an economy that is normalizing post-pandemic, at a slower growth rate with underlying inflationary pressures easing.

The markets are on heightened alert, and small negative or positive shifts in the perception of the economy’s health are being magnified in terms of volatility in stock prices and fixed income yields. It appears to us that the economic data is consistent with an economy that is normalizing post-pandemic, at a slower growth rate with underlying inflationary pressures easing.

The key for common stocks is that earnings should continue to grow through 2025...

As we enter the final two months of the year and head into next week’s elections, the data released during October tells the story of an economy that is on firm footing with consumer confidence rising, employers still adding more than 100,000 jobs each month, and wage gains handily outpacing inflation. The key for common stocks is that earnings should continue to grow through 2025, which is absolutely necessary for further gains in stock prices over the next year or so as we expect that the majority of the price-to-earnings ratio expansion from the expectation for rate cuts has already occurred.

While markets are inherently volatile, a pickup in volatility could occur in the weeks following the election as investors react to the policy implications of the election results. Investors will also react to the actual policy path by the Federal Reserve following the stronger economic data reported last month. We expect the disinflationary influences to remain intact and for the economic expansion to stay on track for an elongated cycle. The inherently positive interplay between additional rate cuts and continued growth in the economy and earnings are expected to carry the day and support higher common stock prices over time.

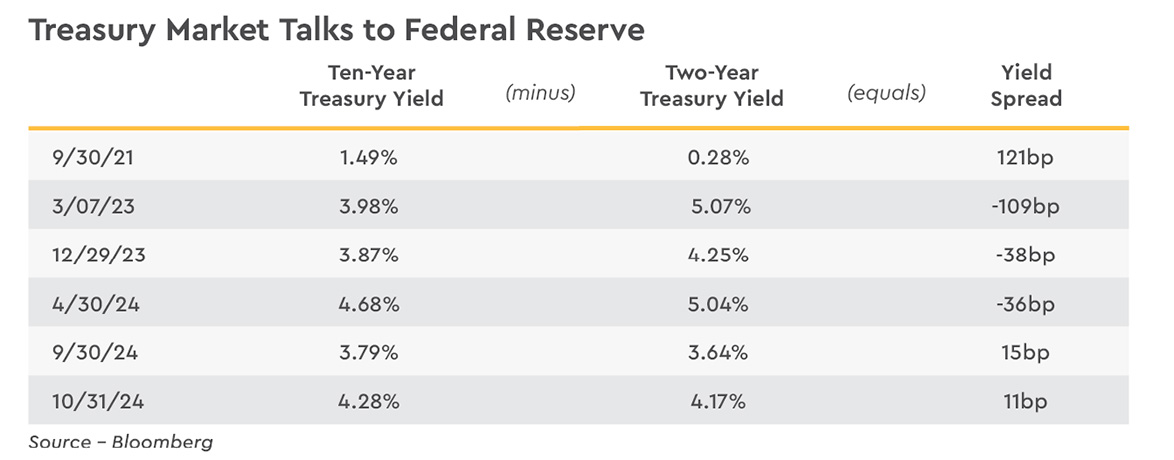

Treasury yields rose right into month end, with the two-year Treasury note yield ending the month at 4.17%, 62 basis points higher than the September low. Similarly, the ten-year Treasury note yield finished October at 4.28%, a rise of 64 basis points from the September low.

There are several reasons behind the sharp reversal in Treasury yields last month. First, and likely most importantly, the strong jobs report for September put fears of the economy falling into recession any time soon to bed and gave Federal Reserve officials some pause about the pace and extent of additional rate cuts. Supporting this view is that nearly 66% of the rise in ten-year Treasury yields since mid-September reflected a rise in real yields consistent with an improved outlook for the economy, with only 34% reflecting a rise in inflation expectations.

Despite assertions from both candidates that their administrations would reign in inflation, investors are concerned that the policy proposals of former President Trump and Vice President Harris will boost inflationary pressures. Both candidates are supporting a variety of tax cuts -- although the Vice President is also supporting an array of tax hikes -- and are supporting measures to lower illegal immigration. Mr. Trump has gone a step further by proposing the largest deportation operation in U.S. history. To the extent each candidate would address illegal immigration, labor market conditions could tighten, placing upward pressure on wages.

Mr. Trump has also called for a significant increase in tariffs on imports to revive domestic manufacturing.

Higher tariffs have the potential to immediately raise the prices of consumer goods and, in the process, reverse the recent deflation in goods prices which has helped bring inflation down toward the Federal Reserve’s 2% target. However, the impact from an increase in tariffs would likely be a one-time bump in prices rather than an ongoing dynamic which would raise the rate of change in prices, i.e., inflationary pressures. Higher tariffs would also likely slow the pace of consumer spending.

Investors are also clearly concerned about the federal government’s dismal fiscal situation. The federal budget deficit for fiscal year 2024 clocked in at $1.83 trillion dollars, 13% larger than the year before despite the real economy growing 2.7% year-over-year and no domestic crisis requiring huge, unbudgeted federal spending.

While tax revenue grew 11% to $4.92 trillion, federal government spending also rose 11% to $6.75 trillion with interest payments on the national debt now larger at $950 billion than the entire defense budget of $826 billion or Medicare at $869 billion. Neither presidential candidate has offered proposals to address the deteriorating U.S. fiscal situation. We expect the bond market to force our elected officials to address this unsustainable deficit situation in the years (maybe months?) ahead.

While tax revenue grew 11% to $4.92 trillion, federal government spending also rose 11% to $6.75 trillion with interest payments on the national debt now larger at $950 billion than the entire defense budget of $826 billion or Medicare at $869 billion. Neither presidential candidate has offered proposals to address the deteriorating U.S. fiscal situation. We expect the bond market to force our elected officials to address this unsustainable deficit situation in the years (maybe months?) ahead.

In last month’s ISS with the yield on ten-year Treasury securities at 3.79% at the end of September, we stated that the vast majority of the decline in ten-year Treasury yields for this cycle had already occurred, and with a modest acceleration in the economy’s growth rate expected in late 2025 that ten-year Treasury yields could rise above 4.0% again. Well as already covered, that pickup in the economy’s growth rate unexpectedly showed up in the data last month, pushing the yield on ten-year Treasury securities well above 4.0% during October.

We are looking for the disinflationary trends in the economy to remain in place as inflation expectations remain well contained and for the economy’s growth rate to slow in 2025 from monetary policy remaining in a moderately restrictive posture as rates are only gradually lowered. As such, we look at the recent backup in Treasury yields as an opportunity to add some duration to fixed income portfolios. Investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve while also modestly extending duration to lock in yields on intermediate term -- four to seven year -- fixed income securities.

Even though yield spreads on both investment grade and non-investment grade corporate securities to Treasury securities are below average, it appears to be worthwhile to increase corporate bond exposure as we expect the soft landing scenario to continue to play out, with the economy in the early stages of an elongated economic cycle. In this environment, yield spreads are not likely to widen to any significant degree.

While markets are inherently volatile, a pickup in volatility could occur in the weeks following the election as investors react to the policy implications of the election results. Investors will also react to the actual policy path by the Federal Reserve following the stronger economic data reported last month. We expect the disinflationary influences to remain intact and for the economic expansion to stay on track for an elongated cycle. The inherently positive interplay between additional rate cuts and continued growth in the economy and earnings are expected to carry the day and support higher common stock prices over time.

Treasury Market

Treasury Yields Rebound from Mid-September Lows

The most surprising development in the financial markets over the past 45 days was the significant rebound in Treasury yields following the larger than expected 50 basis point cut in the target range for the federal funds rate at the September 17-18 FOMC meeting. In the week following the rate cut, the two-year Treasury yield declined to 3.55%, materially below the recent peak of 5.05% recorded April 29. Likewise, the ten-year Treasury yield fell to 3.64% the day before the meeting, well below the late April high of 4.71%.Treasury yields rose right into month end, with the two-year Treasury note yield ending the month at 4.17%, 62 basis points higher than the September low. Similarly, the ten-year Treasury note yield finished October at 4.28%, a rise of 64 basis points from the September low.

There are several reasons behind the sharp reversal in Treasury yields last month. First, and likely most importantly, the strong jobs report for September put fears of the economy falling into recession any time soon to bed and gave Federal Reserve officials some pause about the pace and extent of additional rate cuts. Supporting this view is that nearly 66% of the rise in ten-year Treasury yields since mid-September reflected a rise in real yields consistent with an improved outlook for the economy, with only 34% reflecting a rise in inflation expectations.

Despite assertions from both candidates that their administrations would reign in inflation, investors are concerned that the policy proposals of former President Trump and Vice President Harris will boost inflationary pressures. Both candidates are supporting a variety of tax cuts -- although the Vice President is also supporting an array of tax hikes -- and are supporting measures to lower illegal immigration. Mr. Trump has gone a step further by proposing the largest deportation operation in U.S. history. To the extent each candidate would address illegal immigration, labor market conditions could tighten, placing upward pressure on wages.

Mr. Trump has also called for a significant increase in tariffs on imports to revive domestic manufacturing.

Higher tariffs have the potential to immediately raise the prices of consumer goods and, in the process, reverse the recent deflation in goods prices which has helped bring inflation down toward the Federal Reserve’s 2% target. However, the impact from an increase in tariffs would likely be a one-time bump in prices rather than an ongoing dynamic which would raise the rate of change in prices, i.e., inflationary pressures. Higher tariffs would also likely slow the pace of consumer spending.

Investors are also clearly concerned about the federal government’s dismal fiscal situation. The federal budget deficit for fiscal year 2024 clocked in at $1.83 trillion dollars, 13% larger than the year before despite the real economy growing 2.7% year-over-year and no domestic crisis requiring huge, unbudgeted federal spending.

While tax revenue grew 11% to $4.92 trillion, federal government spending also rose 11% to $6.75 trillion with interest payments on the national debt now larger at $950 billion than the entire defense budget of $826 billion or Medicare at $869 billion. Neither presidential candidate has offered proposals to address the deteriorating U.S. fiscal situation. We expect the bond market to force our elected officials to address this unsustainable deficit situation in the years (maybe months?) ahead.In last month’s ISS with the yield on ten-year Treasury securities at 3.79% at the end of September, we stated that the vast majority of the decline in ten-year Treasury yields for this cycle had already occurred, and with a modest acceleration in the economy’s growth rate expected in late 2025 that ten-year Treasury yields could rise above 4.0% again. Well as already covered, that pickup in the economy’s growth rate unexpectedly showed up in the data last month, pushing the yield on ten-year Treasury securities well above 4.0% during October.

We are looking for the disinflationary trends in the economy to remain in place as inflation expectations remain well contained and for the economy’s growth rate to slow in 2025 from monetary policy remaining in a moderately restrictive posture as rates are only gradually lowered. As such, we look at the recent backup in Treasury yields as an opportunity to add some duration to fixed income portfolios. Investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve while also modestly extending duration to lock in yields on intermediate term -- four to seven year -- fixed income securities.

Even though yield spreads on both investment grade and non-investment grade corporate securities to Treasury securities are below average, it appears to be worthwhile to increase corporate bond exposure as we expect the soft landing scenario to continue to play out, with the economy in the early stages of an elongated economic cycle. In this environment, yield spreads are not likely to widen to any significant degree.