Supply Disruption Leads to Surge in Oil Prices & Slump in Stocks

4/3/2026 (Updated: 4/27/2026) - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

While it was unsettling to watch the rise in oil prices and uncertainty last month and the resulting drop in stock prices, the underlying fundamentals for the U.S. economy -- strong corporate earnings growth, the continued AI buildout, the business capital spending incentives contained in the tax and spending bill signed into law last summer, larger than normal tax refunds from the tax cuts that were retroactive to the beginning of 2025, and a more balanced regulatory regime -- are still positive. The current pullback in common stocks is providing long term investors with an opportunity to put uninvested cash to work at much more attractive prices.

Investors had one key question once the U.S. and Israel started the air strikes, “Will there be a quick resolution to the war with Iran, or will it be a drawn out affair?” The conduit from geopolitical unrest in the Middle East to the global economy and markets is the price of oil. The keys for the U.S. to end the conflict is making sure that Iran’s capacity to build a nuclear bomb has been materially degraded, if not eliminated, and reopening the Strait of Hormuz to safe passage.

While the U.S. and Israel quickly achieved military dominance, and Iran’s missile and nuclear programs were significantly degraded, Tehran’s hardline regime remained entrenched and was still able to hit sensitive targets across the Gulf after four weeks of military strikes. The battered but resilient regime has pursued a strategy of sowing economic chaos in the global markets by threatening to attack foreign vessels attempting to pass through the Strait of Hormuz, with traffic in the strategically vital passageway grinding to a halt.

Oil prices have traded higher because there appears to be no end in sight to oil disruptions through the Strait of Hormuz. The Iranian strategy is to not only push oil prices higher to damaging levels to place pressure on President Trump to end the hostilities on terms favorable to Iran, but to sever global supply chains for liquified natural gas, refined energy products, petrochemicals, and fertilizers.

The month long trends of rising oil prices and falling common stock prices initially reversed on March 23rd after President Trump posted on social media that he was postponing threatened strikes against Iran’s power plants by five days as the U.S. and Iran were having “productive conversations regarding a complete and total resolution of our hostilities.” This announcement came after President Trump threatened in a Saturday evening post that “If Iran does not fully open, without threat, the Strait of Hormuz within 48 hours…the U.S. will hit and obliterate their various power plants.”

Oil prices fell a touch further mid-week as the U.S. sent a 15 point peace plan to Iran to end the war and as Iran’s mission to the United Nations said that “non-hostile vessels” would be able to pass through the Strait of Hormuz provided they coordinate “with the competent Iranian authorities.”

However, oil prices rebounded after Iran responded to the U.S. peace plan by declaring that it will not end the conflict unless Washington pays war reparations, closes its military bases in the Gulf region, and international shippers pay a toll to Iran for the right to transit the Strait, three demands that the U.S. has said are “non-starters” in terms of reaching an agreement to end the war. With every day that the Strait remained closed, investors’ fears that gaining control of the Strait may require a longer campaign increased, despite President Trump’s rhetoric about the war already being won.

One day before President Trump’s original five-day postponement was set to expire, he extended his reprieve for Iran’s energy infrastructure ten days to April 6, which he said was in response to a request from Iran. The ten-day reprieve failed to soothe the market’s oil supply concerns, however, with oil prices rising further. While President Trump’s move avoided escalating the war with Iran at a time that the U.S. had signaled it was open to a negotiated end to the conflict, investors seemed to increasingly lose faith that a quick end to the war with Iran was possible.

The events of last week make three things perfectly clear. One is that while the U.S. decided when the war with Iran would begin, it does not yet control when the war will end. While most of Iran’s military capabilities have been destroyed, its arsenal of drones, naval mines, fast attack craft and midget submarines, and an extensive arsenal of coastal launched anti-ship missiles currently gives Tehran the ability to maintain the narrow Strait of Hormuz as a high risk transit zone for commercial shipping. Second is that what is left of the Iranian regime understands that maintaining control of the Strait is their only bargaining chip currently. The Trump administration has not yet unveiled how the U.S. will translate its military achievements into a lasting cessation of the conflict, with a guarantee that the Strait of Hormuz will offer safe passageway for ships from across the globe. Uncertainty and prices for energy, certain chemicals, and fertilizer will remain high until the key to unlocking the Straits is unveiled. The third is just how rapidly things can change once the drivers of a downturn in stock prices reverse as long as the fundamentals supporting higher stock prices remain in place. While stock prices eventually reversed late in the week and declined to new lows on the month, the rebound in stock prices early in the week is a reminder of how the markets are likely to respond once the war with Iran ends and the Strait of Hormuz is reopened.

Investors received another reminder to remain invested during periods of rising geopolitical tensions following an unconfirmed report on the last day of March that the new Iranian president was open to ending the war with certain guarantees. Stock prices rebounded sharply on the news, which only gained steam on a report from Axios that China and Pakistan proposed a deal on a cease fire and safe passage through the Strait of Hormuz.

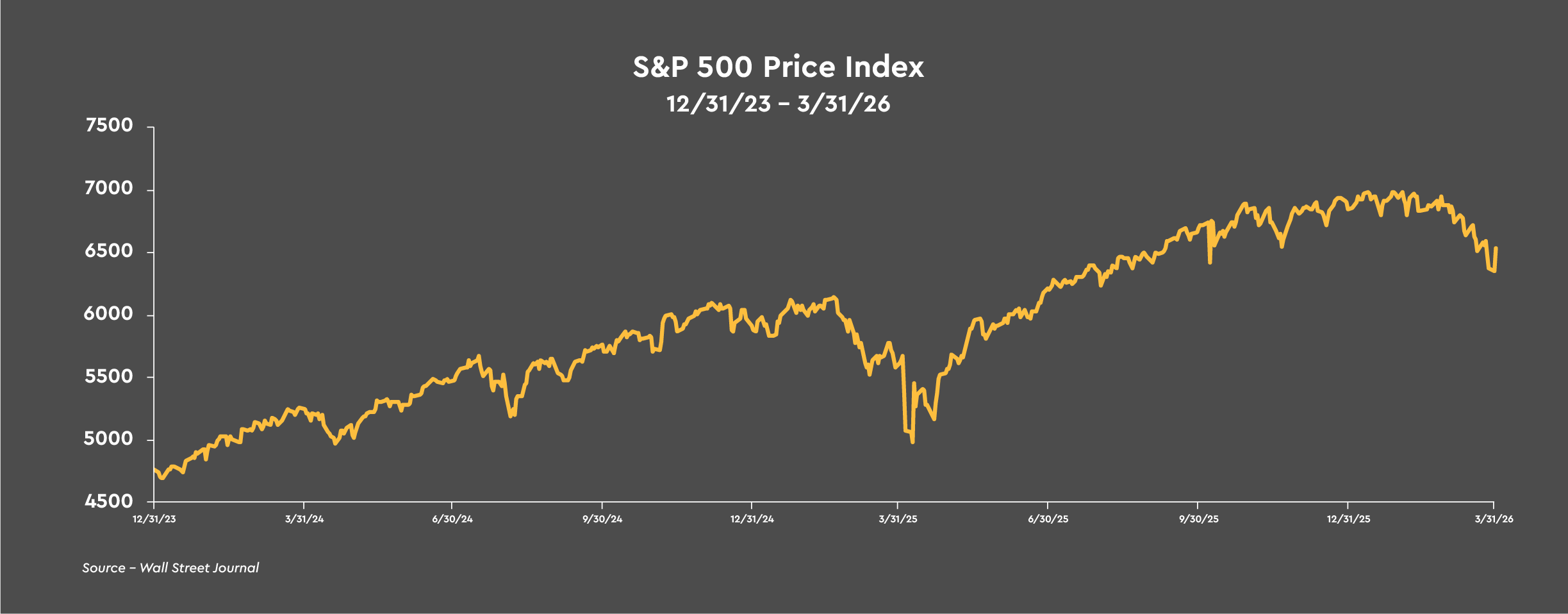

With WTI oil prices breaking above $100 per barrel as March drew to a close, higher oil prices dragged three of the four major stock market measures into correction territory -- lower by at least -10% from their recent highs. The peak-to-trough declines ranged from -10.0% to -13.2%, with only the S&P 500 avoiding a correction, but did decline by -9.1% versus its January 27 high.

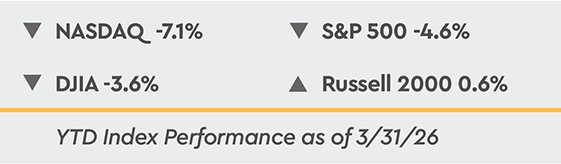

While hitting correction territory for three of the four major market indices is a notable occurrence, keep in mind that since 1928 the S&P 500 reaches correction territory on average once every year. For the month of March, the major stock market measures declined by -4.8% to -5.4%. For the first quarter of 2026, the Russell 2000 Index posted a small gain of 0.6%, while the three large company stock indices fell -3.6% to -7.1%, with the NASDAQ Composite suffering the largest decline.

Equity Markets

Supply Disruption Leads to Surge in Oil Prices & Slump in Stocks

March experienced the most severe shock to energy markets since the 1970’s, and stock prices dropped for four straight weeks in volatile trading following the U.S. and Israel launching massive air strikes against Iran on February 28. West Texas Intermediate (WTI) oil prices traded near $100 per barrel for most of the month as transit through the Strait of Hormuz, a critical chokepoint through which roughly a fifth of the oil consumed around the world flows each day, came to an abrupt halt. Fears that Iran could attack oil tankers in the Strait trapped hundreds of ships in the Persian Gulf while forcing Gulf oil producers to slash output as storage capacity filled up.Investors had one key question once the U.S. and Israel started the air strikes, “Will there be a quick resolution to the war with Iran, or will it be a drawn out affair?” The conduit from geopolitical unrest in the Middle East to the global economy and markets is the price of oil. The keys for the U.S. to end the conflict is making sure that Iran’s capacity to build a nuclear bomb has been materially degraded, if not eliminated, and reopening the Strait of Hormuz to safe passage.

While the U.S. and Israel quickly achieved military dominance, and Iran’s missile and nuclear programs were significantly degraded, Tehran’s hardline regime remained entrenched and was still able to hit sensitive targets across the Gulf after four weeks of military strikes. The battered but resilient regime has pursued a strategy of sowing economic chaos in the global markets by threatening to attack foreign vessels attempting to pass through the Strait of Hormuz, with traffic in the strategically vital passageway grinding to a halt.

Oil prices have traded higher because there appears to be no end in sight to oil disruptions through the Strait of Hormuz. The Iranian strategy is to not only push oil prices higher to damaging levels to place pressure on President Trump to end the hostilities on terms favorable to Iran, but to sever global supply chains for liquified natural gas, refined energy products, petrochemicals, and fertilizers.

The month long trends of rising oil prices and falling common stock prices initially reversed on March 23rd after President Trump posted on social media that he was postponing threatened strikes against Iran’s power plants by five days as the U.S. and Iran were having “productive conversations regarding a complete and total resolution of our hostilities.” This announcement came after President Trump threatened in a Saturday evening post that “If Iran does not fully open, without threat, the Strait of Hormuz within 48 hours…the U.S. will hit and obliterate their various power plants.”

Oil prices fell a touch further mid-week as the U.S. sent a 15 point peace plan to Iran to end the war and as Iran’s mission to the United Nations said that “non-hostile vessels” would be able to pass through the Strait of Hormuz provided they coordinate “with the competent Iranian authorities.”

However, oil prices rebounded after Iran responded to the U.S. peace plan by declaring that it will not end the conflict unless Washington pays war reparations, closes its military bases in the Gulf region, and international shippers pay a toll to Iran for the right to transit the Strait, three demands that the U.S. has said are “non-starters” in terms of reaching an agreement to end the war. With every day that the Strait remained closed, investors’ fears that gaining control of the Strait may require a longer campaign increased, despite President Trump’s rhetoric about the war already being won.

One day before President Trump’s original five-day postponement was set to expire, he extended his reprieve for Iran’s energy infrastructure ten days to April 6, which he said was in response to a request from Iran. The ten-day reprieve failed to soothe the market’s oil supply concerns, however, with oil prices rising further. While President Trump’s move avoided escalating the war with Iran at a time that the U.S. had signaled it was open to a negotiated end to the conflict, investors seemed to increasingly lose faith that a quick end to the war with Iran was possible.

The events of last week make three things perfectly clear. One is that while the U.S. decided when the war with Iran would begin, it does not yet control when the war will end. While most of Iran’s military capabilities have been destroyed, its arsenal of drones, naval mines, fast attack craft and midget submarines, and an extensive arsenal of coastal launched anti-ship missiles currently gives Tehran the ability to maintain the narrow Strait of Hormuz as a high risk transit zone for commercial shipping. Second is that what is left of the Iranian regime understands that maintaining control of the Strait is their only bargaining chip currently. The Trump administration has not yet unveiled how the U.S. will translate its military achievements into a lasting cessation of the conflict, with a guarantee that the Strait of Hormuz will offer safe passageway for ships from across the globe. Uncertainty and prices for energy, certain chemicals, and fertilizer will remain high until the key to unlocking the Straits is unveiled. The third is just how rapidly things can change once the drivers of a downturn in stock prices reverse as long as the fundamentals supporting higher stock prices remain in place. While stock prices eventually reversed late in the week and declined to new lows on the month, the rebound in stock prices early in the week is a reminder of how the markets are likely to respond once the war with Iran ends and the Strait of Hormuz is reopened.

Investors received another reminder to remain invested during periods of rising geopolitical tensions following an unconfirmed report on the last day of March that the new Iranian president was open to ending the war with certain guarantees. Stock prices rebounded sharply on the news, which only gained steam on a report from Axios that China and Pakistan proposed a deal on a cease fire and safe passage through the Strait of Hormuz.

With WTI oil prices breaking above $100 per barrel as March drew to a close, higher oil prices dragged three of the four major stock market measures into correction territory -- lower by at least -10% from their recent highs. The peak-to-trough declines ranged from -10.0% to -13.2%, with only the S&P 500 avoiding a correction, but did decline by -9.1% versus its January 27 high.

While hitting correction territory for three of the four major market indices is a notable occurrence, keep in mind that since 1928 the S&P 500 reaches correction territory on average once every year. For the month of March, the major stock market measures declined by -4.8% to -5.4%. For the first quarter of 2026, the Russell 2000 Index posted a small gain of 0.6%, while the three large company stock indices fell -3.6% to -7.1%, with the NASDAQ Composite suffering the largest decline.

We see very little chance of a rate hike any time soon as the rise in oil prices has resulted from a supply shock, not from an unexpected surge in demand, and would require a meaningful rise in inflation expectations, which has not yet occurred.

Federal Reserve Holds Rates Steady

The Federal Reserve voted 11 to 1 to hold the target range for the federal funds rate steady at 3.5% to 3.75% at the March 17-18 FOMC meeting. The policy statement, the quarterly update on economic forecasts, and Chair Jerome Powell’s press conference provided virtually no clues on future policy adjustments. The policy statement was largely unchanged, the new economic projections penciled in one rate cut this year, the same as in December, and Mr. Powell used some variation of “uncertain” more than a half dozen times in the question and answer session.

Chair Powell said that forecasting the future and modeling policy at a time when the U.S. is at war with Iran is nearly impossible. The resulting oil shock added to worries about the labor market -- payrolls fell by 92,000 jobs in February -- by threatening to further squeeze household purchasing power by boosting inflation in the near term. The mission of the Federal Reserve to address both sides of its dual mandate -- maximum employment and price stability -- is made more difficult by the impact of tariffs on goods prices, the current jump in oil prices, and the immigration and deportation crackdowns which are shrinking labor supply, keeping the unemployment rate steady despite anemic jobs growth over the past 14 months.

The Federal Reserve was expected to hold rates steady at the March meeting with inflation running closer to 3% than 2%. The impact of the war only reinforced that expectation as the standard advice for a central bank facing an oil shock is to look past it, on the grounds that the hit to growth and the higher inflationary pressures roughly cancel out in the near term. That policy stance assumes that inflation expectations remain well anchored. While five-year inflation expectations embodied in Treasury securities have risen since the beginning of the year, they have not broken out, moving to the upper end of the recent three-year range at 2.66% mid-month, but ending March at 2.54%.

The timing of Trump nominee Kevin Warsh to succeed Jerome Powell as chair of the Federal Reserve once his term is over on May 15 remains tied up in the judicial system. A federal judge blocked a pair of Justice Department subpoenas issued on January 9 against the Federal Reserve in connection with a criminal probe of Chair Powell’s congressional testimony last June regarding the renovation of the central bank’s office buildings. A federal judge ruled the federal government had produced “essentially zero evidence” that Mr. Powell committed a crime and said there was “abundant evidence” the dominant purpose of the subpoenas was to pressure him to cut interest rates or resign.

The subpoenas have drawn bipartisan criticism and complicated the politics around Chair Powell’s eventual successor. While the Justice Department appealed the ruling, the decision by the U.S. District Court marks a significant setback in the Administration’s efforts to weaken the independence of the central bank. President Trump continues to insult Mr. Powell on social media, while demanding that he cut rates. The Trump administration also continues its efforts to remove Governor Lisa Cook from the Board of Governors in a landmark case that is before the U.S. Supreme Court.

The nomination of Kevin Warsh needs Senate confirmation. Retiring Senator Thom Tillis, the swing vote on the Senate Banking Committee, has said that he will block Mr. Warsh’s nomination until the Administration drops its criminal probe of Chair Powell. Following the ruling of the District Court, Senator Tillis said in a statement, “This ruling confirms just how weak and frivolous the criminal investigation of Chair Powell is and it is nothing more than a failed attack on Federal Reserve independence. Appealing the ruling will only delay the confirmation of Kevin Warsh as the next Federal Reserve chair.”

Jerome Powell said he would stay on as chair if Kevin Warsh is not confirmed in time for the June FOMC meeting. Mr. Powell also said he would stay on the Board as a Governor until the Justice Department investigation of the central bank, “is well and truly over, with transparency and finality.” Chair Powell said he had not decided whether or not to stay on the Board after his term as chair is over if the investigation ended. Mr. Powell said that he would make his decision based on “what I think is best for the institution and the people we serve.” Staying on the Board after his term as Chair ends, possibly until his term as a Governor ends in January 2028, would deprive President Trump of the opportunity to nominate a loyalist to the Board.

While we were not looking for a rate cut to the end of Jerome Powell’s term as chair through May, following the spike in both uncertainty and oil prices following the start of the war with Iran at the end of February, the futures market for the federal funds rate has completely flipped. Traders now see an almost 3% chance of a rate increase at the June FOMC meeting compared to a 46% chance of a rate cut at the end of February.

The probability that the Federal Reserve could raise rates is greater than zero for every FOMC meeting through the end of 2027.The market does not expect a rate cut this year and has pushed out the possibility of a rate cut to the summer of 2027 at the earliest. We see very little chance of a rate hike any time soon as the rise in oil prices has resulted from a supply shock, not from an unexpected surge in demand, and would require a meaningful rise in inflation expectations, which has not yet occurred.

We acknowledge that crises in financial markets are inherently unpredictable as they can feed upon themselves and lead to unintended consequences that can spread in a manner that was largely unforeseen.

Private Credit Concerns

Large private credit funds have recently faced significant investor redemption requests following publicly traded enterprise software stocks coming under selling pressure for most of 2026. The concern of investors is that over 25% of private credit loans have been extended to smaller software companies. Investors have been questioning whether AI competitors and automation tools could erode demand for traditional software licenses and workflows. Valuations once justified by steady subscription growth are being re-evaluated as investors weigh the possibility that AI could permanently reduce long term revenue potential.

Private credit refers to loans made by a non-bank lender directly to private companies. The private credit market grew rapidly following the 2008 Great Financial Crisis, when tighter banking regulations prompted commercial banks to pull back from certain types of riskier lending. Private credit firms stepped in to fill the credit gap and have since grown to an estimated $1.2 trillion, about 9% of all corporate borrowing, according to J.P. Morgan.

The appeal of private credit included the opportunity for institutional and certain “qualified” wealthy investors to earn returns that generally were higher than what was available on publicly trade debt investments, i.e., government and corporate bonds. With the underlying loans being private and largely illiquid, investors must agree to have their money locked up for several years and redemption requests are typically capped at a percentage of the funds’ net assets, such as 5% per quarter.

While it is clear that some pockets of weakness in private credit exist and that lending by private credit firms will likely tighten in coming months, the relatively small size of the private credit market compared to total corporate borrowing, the amount of underlying equity supporting the credit lines, and the locked-in nature of the capital and the fact that there are no depositors involved lowers the risk of a broad-based meltdown among private credit lenders which could cause a major financial crisis like the 2008 Great Financial Crisis.

In the past 30 to 40 years, every major credit cycle has coincided with a recession or a major shock in a heavy credit dependent industry. We continue to expect the economy to grow at a pace near 2% this year and more than 2% next year, right in line with the economy’s trend growth rate since 2000. Until there is a material weakening in economic growth, the likelihood of a full-blown credit cycle is low.

Additionally, there are not any indicators that would normally signal the onset of a broader credit cycle, such as a material widening of corporate lending spreads, a spike in bank loan loss reserves, or a concerning pickup in consumer and small business bankruptcies. We acknowledge, however, that crises in financial markets are inherently unpredictable as they can feed upon themselves and lead to unintended consequences that can spread in a manner that was largely unforeseen.

Investors need to keep in mind that during periods of regional conflict like the current war with Iran, markets may be volatile, but the need to remain invested is paramount, providing portfolios the opportunity to recover once the conflict is over.

Nothing Good Will Happen Until the Strait of Hormuz Reopens

Higher oil prices had a negative impact on the economy in 1973,1979,1990, and 2008, but did not push the economy into a recession in 2022. The economy is far more resilient to oil shocks today as the U.S. has become energy independent with domestic oil production exploding from five to six million barrels per day in 2011 to over 13 million barrels per day currently. The shale oil revolution has turned the U.S. into a net exporter of oil and a major exporter of liquefied natural gas. The domestic drag on households from higher oil prices is now transferred to domestic oil producers rather than to foreign oil producers.In terms of the outlook for the economy, the rise in oil prices and uncertainty will likely shave the economy’s expected growth rate this year to 2% compared to our prior expectation of 2.5% to 3%, with the potential for growth this year to be less than 2% the longer oil prices remain elevated. As for inflation, we expect pricing pressures to remain sticky near 3% for the better part of the year, before easing a bit over the back half of the year, but likely remaining above the Federal Reserve’s 2% target.

The consensus outlook for earnings on the S&P 500 to grow this year has actually risen slightly to about 17% from a little under 14% before the start of the Iran war, largely due to the positive impact on the energy sector from higher energy prices. Some of the growth in the economy that was expected in 2026 is likely being pushed into 2027 due to the higher level of oil prices currently. Stock gains could also be pushed into 2027. However, the forward looking nature of markets could realize some of those delayed gains into the back half of 2026, depending upon how long the Strait of Hormuz is closed and oil prices remain elevated.

Investors need to keep in mind that during periods of regional conflict like the current war with Iran, markets may be volatile, but the need to remain invested is paramount, providing portfolios the opportunity to recover once the conflict is over. The unexpected rebound in stock prices early last week and again on the last day of March only underscores the need to maintain a steady hand with your investments when geopolitical risks rise. The initial retreat from risk assets tends not to last long and has relatively quickly been recouped so long as the economy was not already in recession or stocks in a bear market when the conflict started.

Several pundits have tried to compare the current disruption in the markets from the Iran war to the sharp decline in stock prices last April following President Trump unveiling his “reciprocal tariffs,” which would have resulted in the largest tax increase in the history of the U.S. The S&P 500 plunged -12.1% in the four days after the President announced his sweeping levies on April 2, only to rally 37.4% through the end of the year.

The key difference currently from Liberation Day last April is the turn in the market last year depended upon one person, President Trump, partially walking back some of those tariff policies. With respect to the current war with Iran, three parties must agree to change the narrative, President Trump and Israel, and most importantly, someone who speaks for the Iranian regime and has the authority to cease the retaliatory strikes by Iran.

While it was unsettling to watch the rise in oil prices and uncertainty last month and the resulting drop in stock prices, the underlying fundamentals for the U.S. economy -- strong corporate earnings growth, the continued AI buildout, the business capital spending incentives contained in the tax and spending bill signed into law last summer, larger than normal tax refunds from the tax cuts that were retroactive to the beginning of 2025, and a more balanced regulatory regime -- are still positive. The current pullback in common stocks is providing long term investors with an opportunity to put uninvested cash to work at much more attractive prices.

In last month’s ISS, we stated that the recent rotation into the slower growth sectors of the market will run its course in coming months, with the sectors and companies demonstrating the strongest actual and potential earnings growth poised to take the lead. With investors even more concerned about growth in the economy following the rise in uncertainty and oil prices during March, the war with Iran only increases our expectation that growth stocks will be the main beneficiary of an upturn in stock prices with a cessation of the war with Iran.

We do not expect the yield on the ten-year Treasury note to trade below 4% over the next few quarters, unless the economy’s growth rate disappoints in large measure from the economy’s 2% average annual growth rate since 1970.

Treasury Market

Treasury Yields Rise as Oil Prices Surge and Worries over Federal Budget Deficits Mount.

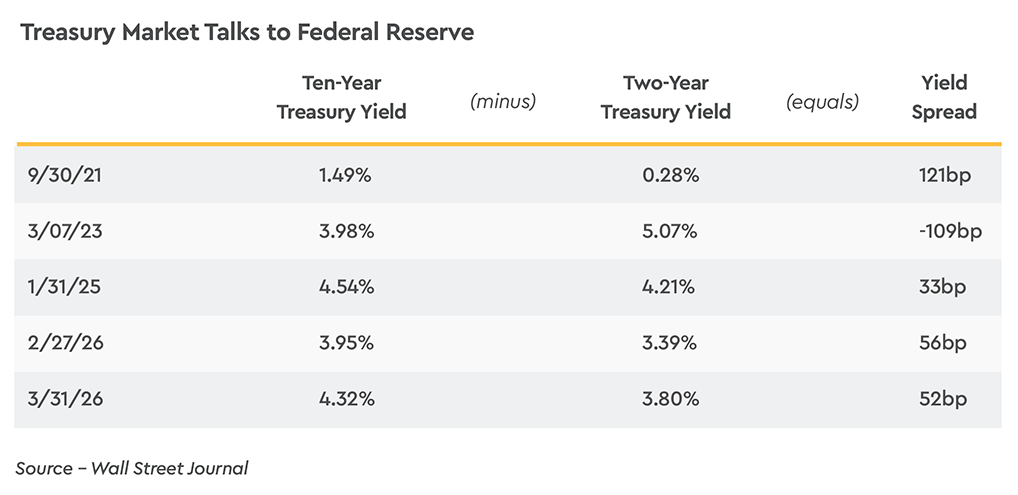

Frequently a rise in geopolitical risks and a sudden swoon in stock prices will bring about a flight to safety into Treasury securities. That was not the case last month as yields rose across Treasury yield curve. The yield on two-year Treasury notes rose 41 basis points to 3.80% last month, with inflation expectations rising 15 basis points and the real yield rising 26 basis points.

The 3.80% two-year Treasury yield is higher than the 3.63% mid-point of the current 3.50% to 3.75% target range for the federal funds rate. The Treasury market is not only not expecting a rate cut before the end of the year, it is expecting about a 68% chance of a rate hike. The higher real yield likely reflects the dismal fiscal position of the federal government.

A larger federal budget deficit is widely expected in order to pay for the munitions used so far in the Iran war, along with, an expectation that a permanently higher level of defense spending will likely be required to protect the U.S. against our adversaries. With the economy’s growth rate expected to be slower this year than previously expected due to the rise in uncertainty and oil prices and defense outlays expected to grow at a faster pace, the recent trend of the federal budget deficit falling in relative size to the economy has now reversed, with incremental improvement difficult to pencil out given recent trends.

The yield on ten-year Treasury notes rose 37 basis points to 4.32%, with real yields rising 32 basis points and inflation expectations rising a modest 5 basis points. The rise in real yields likely reflects the longer run deteriorating outlook for federal budget deficits, at a time that interest on the national debt was 3.2% of nominal GDP last year, greater than the amount spent on defense.

This compares to interest on the national debt running at 1.5% of nominal GDP in 2021, and projected to reach 4.2% of nominal GDP in less than a decade. Even if inflationary pressures fall next year, it will be difficult for yields on longer dated Treasury yields to fall much in the future due to ever growing spending on social programs, at the same time that defense outlays and interest expense will be under significant upward pressure.

Where the ten-year Treasury yield settles out in coming months will likely be the result of a tug-of-war between higher oil prices and other supply disruptions placing upward pressure on inflation in the near term and the economy’s growth rate muddling along at a pace of 2.0% or slightly less, resulting in an environment of nominal GDP running close to 5.0%. Historically, the ten-year Treasury yield gravitates toward the economy’s nominal growth rate over time.

As such, we do not expect the yield on the ten-year Treasury note to trade below 4% over the next few quarters, unless the economy’s growth rate disappoints in large measure from the economy’s 2% average annual growth rate since 1970. The longer energy and commodity supplies remain disrupted, the greater is the near term risk to inflationary pressures, as well as, potential damage to the economy’s growth rate.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve, largely due to the heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.