The Electorate Votes for Change

12/2/2024 (Updated: 4/9/2026) - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

The economic data released over the past couple months paints a picture of an economy that is on firm footing. Now, prospects for investors stand to improve with President-elect Trump’s pro-growth, domestic-focused agenda, as long as the deficit, tariffs, and a potentially heated economy are managed appropriately.

Common stocks reacted very strongly to the election results, with the total value of U.S. stocks rising by $1.62 trillion the day after the election, their fifth best one day showing ever, by that measure. The surge reflects the opportunities that investors are hoping will materialize with four years of tax cuts, deregulation, a revival of dealmaking and domestic manufacturing, and strong economic growth supporting an elongated economic expansion. Additionally, President Biden’s all-of-government approach to climate change will be replaced with an all-of-government effort to promote domestic energy production.

President Trump is expected to bring a much more laissez-faire approach to anti-trust enforcement, which should spur an increase in merger and acquisition activity, and a shift toward deregulation, the anticipation of which has already lifted business and market sentiment, particularly in industries such as banking, energy and cryptocurrency. A revival of research and development tax credits would also be positive for productivity in the years ahead and, in turn, U.S. competitiveness and the economy’s potential growth rate.

On the immigration front, Mr. Trump will likely have strong congressional backing, including considerable resources, to close the southern border. Mr. Trump has also proposed the largest deportation operation in U.S. history. There are concerns that the combination of closing the southern border and a significant deportation effort could tighten labor market conditions, placing upward pressure on wages and prices.

With supply and demand conditions in the labor market in much better balance than two years ago, we do not expect that reducing the flow of illegal immigrants will have any near term inflationary impacts. We anticipate that legal hurdles and public sentiment will likely limit the scope of the deportation operation and expect the Trump administration to focus on deporting migrants who have been identified as public safety and national security threats and those who have been ordered to leave the U.S but have not done so.

Equity Markets

The Electorate Votes for Change

Donald Trump’s decisive election victory marked an extraordinary political comeback that included a powerful mandate by winning the popular vote, the first Republican president to do so since President George W. Bush in 2004. The sweeping Republican victory carried GOP majorities on both sides of Capitol Hill which will undoubtedly reshape the economic outlook as broad policy shifts on taxes, federal government spending, immigration, and trade take place. American voters seeking a change in fortune bet on the President-elect’s promises to boost the economy, lower inflationary pressures and taxes, settle foreign conflicts, and put a stop to illegal immigration.Common stocks reacted very strongly to the election results, with the total value of U.S. stocks rising by $1.62 trillion the day after the election, their fifth best one day showing ever, by that measure. The surge reflects the opportunities that investors are hoping will materialize with four years of tax cuts, deregulation, a revival of dealmaking and domestic manufacturing, and strong economic growth supporting an elongated economic expansion. Additionally, President Biden’s all-of-government approach to climate change will be replaced with an all-of-government effort to promote domestic energy production.

President Trump is expected to bring a much more laissez-faire approach to anti-trust enforcement, which should spur an increase in merger and acquisition activity, and a shift toward deregulation, the anticipation of which has already lifted business and market sentiment, particularly in industries such as banking, energy and cryptocurrency. A revival of research and development tax credits would also be positive for productivity in the years ahead and, in turn, U.S. competitiveness and the economy’s potential growth rate.

On the immigration front, Mr. Trump will likely have strong congressional backing, including considerable resources, to close the southern border. Mr. Trump has also proposed the largest deportation operation in U.S. history. There are concerns that the combination of closing the southern border and a significant deportation effort could tighten labor market conditions, placing upward pressure on wages and prices.

With supply and demand conditions in the labor market in much better balance than two years ago, we do not expect that reducing the flow of illegal immigrants will have any near term inflationary impacts. We anticipate that legal hurdles and public sentiment will likely limit the scope of the deportation operation and expect the Trump administration to focus on deporting migrants who have been identified as public safety and national security threats and those who have been ordered to leave the U.S but have not done so.

On trade policy, tariffs will raise the prices of imported goods, though it would be a one-time bump in prices, not necessarily the start of an inflationary cycle.

On trade policy, tariffs will raise the prices of imported goods, though it would be a one-time bump in prices, not necessarily the start of an inflationary cycle. Of course, the extent of any price increase from higher tariffs could be offset by pricing concessions from foreign manufacturers and domestic distributors, along with appreciation in the U.S. dollar versus foreign currencies.

There appear to be two schools of thought on how tariffs could be implemented. One is that President Trump uses them as bargaining tools to get better trade deals and influence the foreign policy of other nations, while the other is that he delivers on his threats and implements them much more broadly. Reflecting on Mr. Trump’s first term as president, the lesson for investors is to take the President-elect seriously, but not literally, as he is just as likely to use his policy proposals as negotiating tactics as he is to actually make changes in policy.

In trade negotiations, no country gives up something of value for nothing. The strategic use of leverage is essential to successful negotiating. With broad opposition among Republicans to across-the-board tariffs and the likelihood that they could be blocked by the courts, we expect President Trump to use a targeted approach to tariff policy with a keen focus on outcomes which support domestic manufacturing and production and provide access to foreign markets. As is so often the case in economic policy proposals, the devil will be in the details with regard to the impact on the economy.

There appear to be two schools of thought on how tariffs could be implemented. One is that President Trump uses them as bargaining tools to get better trade deals and influence the foreign policy of other nations, while the other is that he delivers on his threats and implements them much more broadly. Reflecting on Mr. Trump’s first term as president, the lesson for investors is to take the President-elect seriously, but not literally, as he is just as likely to use his policy proposals as negotiating tactics as he is to actually make changes in policy.

In trade negotiations, no country gives up something of value for nothing. The strategic use of leverage is essential to successful negotiating. With broad opposition among Republicans to across-the-board tariffs and the likelihood that they could be blocked by the courts, we expect President Trump to use a targeted approach to tariff policy with a keen focus on outcomes which support domestic manufacturing and production and provide access to foreign markets. As is so often the case in economic policy proposals, the devil will be in the details with regard to the impact on the economy.

Measures of business sentiment and expectations soared last month following the election...

Measures of business sentiment and expectations soared last month following the election on the prospects of continued low corporate tax rates, a lighter approach to regulation, and the creation of the Department of Government Efficiency which will pursue three major types of reform: regulatory rescissions, administrative reductions, and spending cuts.

Investors are encouraged that the Trump administration is looking to address the $1.8 trillion federal budget deficit by focusing on growth and cutting spending and regulations rather than raising taxes. Measures of overall consumer sentiment continued their rise following the election, though with sharply opposing reactions along party lines.

The powerful combination of President Trump’s re-election amidst a Republican takeover of Congress and another rate cut by the Federal Reserve unleashed the animal spirits of investors, sending stock prices sharply higher over the first week of November. Common stocks gave back about one half of that initial surge in the middle of the month as investors turned their focus to the potential consequences arising from Mr. Trump’s policy proposals, which included a sharp rise in Treasury yields across the yield curve to four month highs during the third week of November.

Likewise, investors had to price in the possibility that the Federal Reserve could deliver fewer rate cuts than were previously expected should the economic outlook improve following Mr. Trump’s re-election. Chair Powell reinforced this notion in a question and answer session in Dallas by commenting that the economy was not sending any signals that the Federal Reserve needs to be in a hurry to lower interest rates. A modest pullback in stock prices mid-month was the price to be paid for a brighter outlook for economic growth and profit-making opportunities.

However, stock prices regained their footing over the final two weeks of November as Treasury yields pulled back from their late November highs and President-elect Trump unveiled many of his cabinet picks, including his economic policy team – Treasury, Commerce, National Economic Council, Office of Management and Budget – which collectively are likely to place a priority on market friendly policies to boost economic growth and hold down inflation, interest rates, and bond yields.

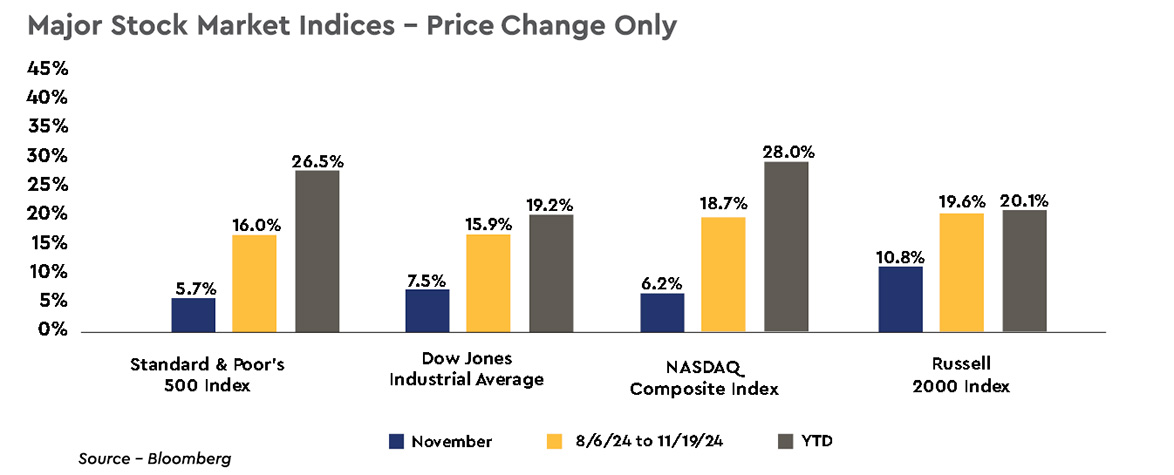

For the full month of November common stocks posted strong returns with the major market indices rising between 5.7% to 10.8% led by the Russell 2000 Index of small company stocks. Since the aggressive unwind of the “yen carry trade” in early August, the major stock market measures are higher by 15.9% to 19.6% and are higher by 19.2% to 28.0% over the first eleven months of 2024.

At the press conference, Chair Powell again characterized the September and November rate cuts as an attempt to “recalibrate policy to a more neutral level.” He commented that prior to the rate cut in September, the real federal funds rate was very high at a level just under 3.0%. After 75 basis points of rate cuts and using the latest inflation data, the real federal funds rate is now just under 2.0%, a level that is still high from a historical perspective. Mr. Powell stated that monetary policy was still “restrictive,” the labor market has “cooled significantly,” and inflation has “moved down a great deal.”

Chair Powell said the FOMC Committee is currently focused on “the appropriate pace of rate cuts and the destination.” In other words, the Federal Reserve does not want to see the labor market cool further and is attempting to take the policy rate to a neutral level that neither stimulates nor restricts the pace of economic activity. It appears that Mr. Powell is hoping that removing some of the policy restrictiveness while the economy and the labor market are still relatively strong will boost the odds of the soft landing for the economy continuing.

Investors are encouraged that the Trump administration is looking to address the $1.8 trillion federal budget deficit by focusing on growth and cutting spending and regulations rather than raising taxes. Measures of overall consumer sentiment continued their rise following the election, though with sharply opposing reactions along party lines.

The powerful combination of President Trump’s re-election amidst a Republican takeover of Congress and another rate cut by the Federal Reserve unleashed the animal spirits of investors, sending stock prices sharply higher over the first week of November. Common stocks gave back about one half of that initial surge in the middle of the month as investors turned their focus to the potential consequences arising from Mr. Trump’s policy proposals, which included a sharp rise in Treasury yields across the yield curve to four month highs during the third week of November.

Likewise, investors had to price in the possibility that the Federal Reserve could deliver fewer rate cuts than were previously expected should the economic outlook improve following Mr. Trump’s re-election. Chair Powell reinforced this notion in a question and answer session in Dallas by commenting that the economy was not sending any signals that the Federal Reserve needs to be in a hurry to lower interest rates. A modest pullback in stock prices mid-month was the price to be paid for a brighter outlook for economic growth and profit-making opportunities.

However, stock prices regained their footing over the final two weeks of November as Treasury yields pulled back from their late November highs and President-elect Trump unveiled many of his cabinet picks, including his economic policy team – Treasury, Commerce, National Economic Council, Office of Management and Budget – which collectively are likely to place a priority on market friendly policies to boost economic growth and hold down inflation, interest rates, and bond yields.

For the full month of November common stocks posted strong returns with the major market indices rising between 5.7% to 10.8% led by the Russell 2000 Index of small company stocks. Since the aggressive unwind of the “yen carry trade” in early August, the major stock market measures are higher by 15.9% to 19.6% and are higher by 19.2% to 28.0% over the first eleven months of 2024.

Federal Reserve Lowers Rates Another 25 Basis Points

In a unanimous decision, the Federal Reverse lowered the target range for the federal funds rate another 25 basis points to 4.5% to 4.75% at the November 6-7 FOMC meeting, a policy move that was widely anticipated. There was not a lot new to take away from the meeting. Only modest changes were made to the policy statement, none of which were significant.At the press conference, Chair Powell again characterized the September and November rate cuts as an attempt to “recalibrate policy to a more neutral level.” He commented that prior to the rate cut in September, the real federal funds rate was very high at a level just under 3.0%. After 75 basis points of rate cuts and using the latest inflation data, the real federal funds rate is now just under 2.0%, a level that is still high from a historical perspective. Mr. Powell stated that monetary policy was still “restrictive,” the labor market has “cooled significantly,” and inflation has “moved down a great deal.”

Chair Powell said the FOMC Committee is currently focused on “the appropriate pace of rate cuts and the destination.” In other words, the Federal Reserve does not want to see the labor market cool further and is attempting to take the policy rate to a neutral level that neither stimulates nor restricts the pace of economic activity. It appears that Mr. Powell is hoping that removing some of the policy restrictiveness while the economy and the labor market are still relatively strong will boost the odds of the soft landing for the economy continuing.

The Federal Reserve remains data dependent, but we would add that it is also policy dependent following the election with President-elect Trump returning to the White House.

The Federal Reserve remains data dependent, but we would add that it is also policy dependent following the election with President-elect Trump returning to the White House. The FOMC Committee will need to assess the policies enacted by the Trump administration and estimate their impact on the economy’s growth rate and underlying inflationary pressures. Based on Mr. Trump’s campaign platform, we expect fewer rate cuts and higher yields on longer dated Treasury securities than what would have occurred under a Harris administration.

In last month’s Investment Strategy Statement, we stated that we expected no more than four additional rate cuts to June of next year given the forward momentum in the economy. Following last month’s rate cut, that leaves at most three rate cuts over the next seven months in our view. Mr. Trump’s re-election only reinforces our perspective that fewer rather than more rate cuts will occur over the next year or two. We suspect that if there is any change in our view based on the policy agenda that will unfold from the Trump administration early in 2025, the number of rate cuts to June of next year will likely be lower than three, not higher.

The markets will be closely watching Mr. Trump’s previously contentious relationship with Mr. Powell. President Trump appointed Mr. Powell as Chair in February 2018, but repeatedly lashed out against Mr. Powell during his first term as president, complaining that the central bank chief was unnecessarily raising rates to an eventual peak in December 2018. The Federal Reserve subsequently started lowering rates in July 2019. Mr. Trump said in an interview in October prior to the election that the president should have a say on interest rate decisions.

The tradition of the Federal Reserve System’s independence from the Executive Branch gives the central bank the ability to shape monetary policy decisions based solely on its dual mandate of full employment and price stability, without political interference or pressure. It is commonly held, and we agree, that a central bank’s ability to carry out monetary policy without political interference is a critical component of its ability to control inflation.

A central bank’s credibility is bolstered by its independence and such credibility is key to maintaining long term, anchored inflation expectations. A central bank subject to short term political influences would likely not be credible in its pursuit of price stability as the markets and the public would recognize the risk that monetary policymakers could be pressured to pursue short run expansionary policies that could be inconsistent with long run price stability.

The Federal Reserve views its political independence as a core feature that allows it to shape monetary policy exclusively based on the health of the economy, not election considerations. Under the current interpretation of the legal framework Congress put in place to oversee the Federal Reserve, the President’s most direct way of increasing his influence at the central bank would be to install loyalists on its seven member board of governors, in particular the chair. The first governor’s term to expire during the Trump administration will be in January 2026 and Mr. Powell’s term as Chair of the Federal Reserve expires in May 2026.

The economic data released over the past couple months paints a picture of an economy that is on firm footing with consumer and business confidence rising, solid productivity growth, employers still adding more than 100,000 jobs each month – October’s jobs report (12,000) was distorted by two hurricanes and the strike at Boeing – and wage gains handily outpacing inflation. Now the prospects for the economy have brightened further with the re-election of President Trump who has promised a pro-growth, domestic-focused agenda including deregulation, tax cuts, and higher energy production.

The key for common stocks is that earnings should continue to grow through 2025, which is absolutely necessary for further gains in stock prices over the next year or so as we expect that the majority of the price-to-earnings ratio expansion from the expectation for rate cuts has already occurred. On the earnings front, with 94% of S&P 500 companies reporting, 3Q 2024 operating earnings are projected to grow a very strong 14% on a year-over-year basis. The analysts at Standard and Poor’s are forecasting operating earnings to grow by 9.6% over the four quarters of 2024 and by another 16.6% by 4Q 2025.

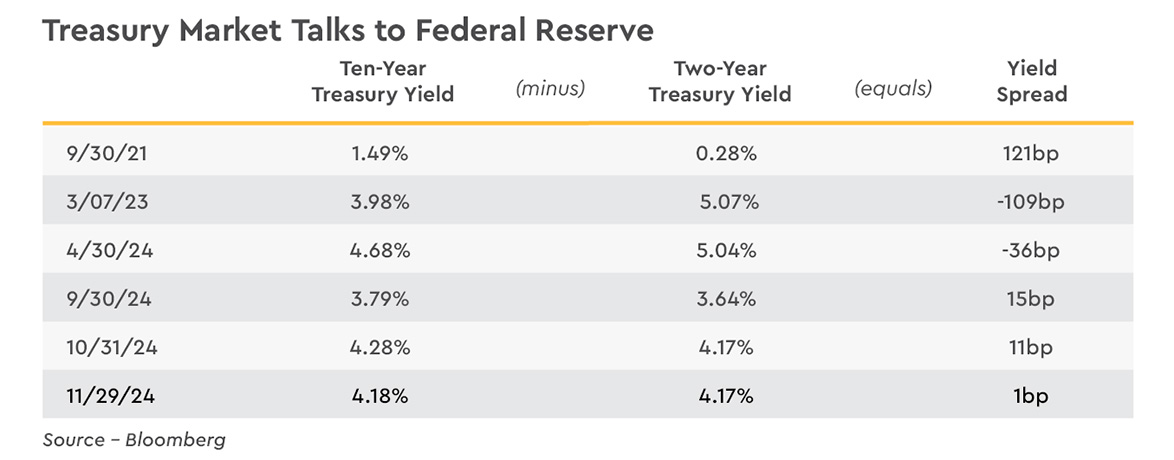

It seems to us that the biggest risk to common stocks over the next couple of months is the aggressive rise in Treasury yields from the lows recorded in mid-September around the 50 basis point cut in the policy rate by the Federal Reserve. While Treasury yields retraced all of their sudden rise following the election over the last week of November, the yield on two-year Treasury notes is still higher by 62 basis points compared to mid-September at 4.17%, while ten-year Treasury yields are higher by 54 basis points at 4.18%.

The combination of stronger than expected growth, record issuance of new Treasury debt, the Federal Reserve balance-sheet reduction, and now renewed inflation and deficit concerns about forthcoming economic policy have pressured Treasury yields higher.

In last month’s Investment Strategy Statement, we stated that we expected no more than four additional rate cuts to June of next year given the forward momentum in the economy. Following last month’s rate cut, that leaves at most three rate cuts over the next seven months in our view. Mr. Trump’s re-election only reinforces our perspective that fewer rather than more rate cuts will occur over the next year or two. We suspect that if there is any change in our view based on the policy agenda that will unfold from the Trump administration early in 2025, the number of rate cuts to June of next year will likely be lower than three, not higher.

Will He Stay or Will He Go?

The most newsworthy exchange at the press conference was Chair Powell being asked if he would resign if requested by President-elect Trump. Mr. Powell simply answered, “No.” On a follow-up question, Mr. Powell was asked if he thought a sitting president has the legal authority to fire or demote a Chair of the Federal Reserve or any other governor. Chair Powell replied, “Not permitted under the law.”The markets will be closely watching Mr. Trump’s previously contentious relationship with Mr. Powell. President Trump appointed Mr. Powell as Chair in February 2018, but repeatedly lashed out against Mr. Powell during his first term as president, complaining that the central bank chief was unnecessarily raising rates to an eventual peak in December 2018. The Federal Reserve subsequently started lowering rates in July 2019. Mr. Trump said in an interview in October prior to the election that the president should have a say on interest rate decisions.

The tradition of the Federal Reserve System’s independence from the Executive Branch gives the central bank the ability to shape monetary policy decisions based solely on its dual mandate of full employment and price stability, without political interference or pressure. It is commonly held, and we agree, that a central bank’s ability to carry out monetary policy without political interference is a critical component of its ability to control inflation.

A central bank’s credibility is bolstered by its independence and such credibility is key to maintaining long term, anchored inflation expectations. A central bank subject to short term political influences would likely not be credible in its pursuit of price stability as the markets and the public would recognize the risk that monetary policymakers could be pressured to pursue short run expansionary policies that could be inconsistent with long run price stability.

The Federal Reserve views its political independence as a core feature that allows it to shape monetary policy exclusively based on the health of the economy, not election considerations. Under the current interpretation of the legal framework Congress put in place to oversee the Federal Reserve, the President’s most direct way of increasing his influence at the central bank would be to install loyalists on its seven member board of governors, in particular the chair. The first governor’s term to expire during the Trump administration will be in January 2026 and Mr. Powell’s term as Chair of the Federal Reserve expires in May 2026.

Earnings Growth Should Carry the Day

The economic data released over the past couple months paints a picture of an economy that is on firm footing with consumer and business confidence rising, solid productivity growth, employers still adding more than 100,000 jobs each month – October’s jobs report (12,000) was distorted by two hurricanes and the strike at Boeing – and wage gains handily outpacing inflation. Now the prospects for the economy have brightened further with the re-election of President Trump who has promised a pro-growth, domestic-focused agenda including deregulation, tax cuts, and higher energy production. The key for common stocks is that earnings should continue to grow through 2025, which is absolutely necessary for further gains in stock prices over the next year or so as we expect that the majority of the price-to-earnings ratio expansion from the expectation for rate cuts has already occurred. On the earnings front, with 94% of S&P 500 companies reporting, 3Q 2024 operating earnings are projected to grow a very strong 14% on a year-over-year basis. The analysts at Standard and Poor’s are forecasting operating earnings to grow by 9.6% over the four quarters of 2024 and by another 16.6% by 4Q 2025.

It seems to us that the biggest risk to common stocks over the next couple of months is the aggressive rise in Treasury yields from the lows recorded in mid-September around the 50 basis point cut in the policy rate by the Federal Reserve. While Treasury yields retraced all of their sudden rise following the election over the last week of November, the yield on two-year Treasury notes is still higher by 62 basis points compared to mid-September at 4.17%, while ten-year Treasury yields are higher by 54 basis points at 4.18%.

The combination of stronger than expected growth, record issuance of new Treasury debt, the Federal Reserve balance-sheet reduction, and now renewed inflation and deficit concerns about forthcoming economic policy have pressured Treasury yields higher.

It will be important that the Trump administration displays a clear-eyed assessment of budget trade-offs by offsetting spending and tax policy changes in a fiscally responsible manner.

It will be important that the Trump administration displays a clear-eyed assessment of budget trade-offs by offsetting spending and tax policy changes in a fiscally responsible manner. Mr. Trump needs to remember that profligate spending with little regard for budget deficits and inflation contributed to his re-election.

The major uncertainty investors will face as the new year unfolds is the current policy fog which will not clear up until the legislative sessions play out during 2025. However, we expect the disinflationary influences to remain largely intact and for the economic expansion to stay on track for an elongated cycle, helped along by the pro-business economic agenda that the Trump administration will put in place.

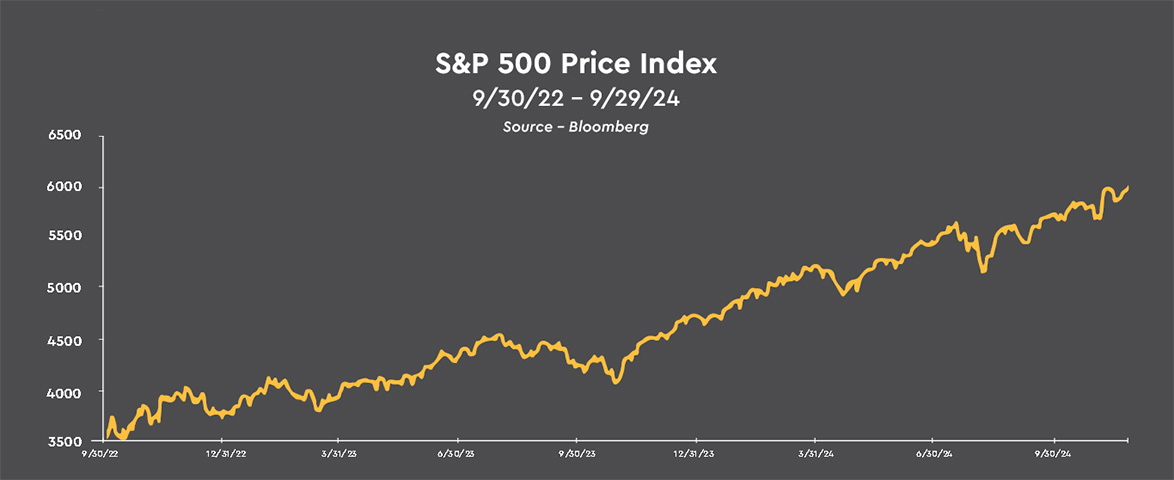

Leaving aside a significant sell-off in common stocks this month, the S&P 500 is looking at back-to-back +20% yearly price gains. This has occurred on four occasions since WWII with the next year return coming in at 2.6% in 1956, 31.0% in 1997, 26.7% in 1998, and 19.5% in 1999. Not surprisingly, the key to the next year returns was subsequent growth in the economy and earnings.

We expect the inherently positive interplay between additional rate cuts – even if fewer than previously expected – and continued growth in the economy and earnings to carry the day and support higher common stock prices over time. The major risk to stock prices over the next couple years would be the Federal Reserve needing to shift policy to a more restrictive stance to fight a rekindling of inflationary pressures, which would likely reset common stock prices lower.

While the Federal Reserve will eventually need to pivot to fighting inflationary pressures at some point in the future, the dynamics for that next policy pivot are not currently in place. However, we will follow the new administration’s policy proposals closely to determine their potential inflationary influences. The Treasury market will undoubtedly assist in that assessment as it is always sensitive to a build in inflation expectations.

While Treasury yields did pull back from their post-election peaks, the yield on the ten-year Treasury note still ended November at 4.18%, 54 basis points higher than the 3.64% yield the day before the September FOMC meeting. The 3.64% Treasury yield was comprised of a 2.12% ten year inflation expectation and a real yield of 1.52%.

Currently, the 4.18% ten-year Treasury yield is comprised of a slightly higher ten year inflation expectation of 2.22%, a rise of 10 basis points, while the real yield is higher by 44 basis points at 1.96%. The stronger economic data over the past two months and the expectation that President Trump’s economic agenda will be pro-growth and add to the national debt led to 81% of the rise in the ten-year Treasury yield since mid-September showing up as a higher real yield.

The analysis of the 62 basis point rise in the two-year Treasury yield to 4.17% from 3.55% the week following the September FOMC meeting is quite different. The two year inflation expectation has risen by 40 basis points to 2.40% from 2.0% – 65% of the rise in the two-year Treasury yield – while the real yield has risen by 22 basis points to 1.77% from 1.55%. Investors are concerned that the combination of the Federal Reserve cutting rates and a faster pace of economic growth will cause the disinflationary trend since 2022 to stall above the Federal Reserve’s 2% target.

With the yield on the two-year Treasury note 51 basis points below the 4.68% midpoint of the current target range of the federal funds rate, the market is not expecting a further material drop in the target range for the federal funds rate. This is consistent with our view that the Federal Reserve will cut rates at most three more times to June of next year. This somewhat more restrictive monetary policy stance should help keep the disinflationary trend in the economy in place, just at a slower pace than has been experienced over the past two years.

As we mentioned in the October Investment Strategy Statement, in a steady state environment the yield on the ten-year Treasury note tends to settle in at a level near the growth rate of nominal GDP. An inflation rate and a real growth rate both in the range of 2% to 2.5%, would be consistent with a yield on the ten-year Treasury note in a range of 4.0% to 5.0%, compared to the current yield of 4.18%. Where the yield on the ten-year Treasury note trades over the next year will be determined by how the policy proposals of the Trump administration unfold next year and how they impact the economy.

In this environment, investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve, while also modestly extending duration to lock in yields on intermediate term – four to seven year – fixed income securities.

Even though yield spreads on both investment grade and non-investment grade corporate securities to Treasury securities are below average, it appears to be worthwhile to increase corporate bond exposure as we expect the soft landing scenario to continue to play out, with the economy in the early stages of an elongated economic cycle. In this environment, yield spreads are not likely to widen to any significant degree.

The major uncertainty investors will face as the new year unfolds is the current policy fog which will not clear up until the legislative sessions play out during 2025. However, we expect the disinflationary influences to remain largely intact and for the economic expansion to stay on track for an elongated cycle, helped along by the pro-business economic agenda that the Trump administration will put in place.

Leaving aside a significant sell-off in common stocks this month, the S&P 500 is looking at back-to-back +20% yearly price gains. This has occurred on four occasions since WWII with the next year return coming in at 2.6% in 1956, 31.0% in 1997, 26.7% in 1998, and 19.5% in 1999. Not surprisingly, the key to the next year returns was subsequent growth in the economy and earnings.

We expect the inherently positive interplay between additional rate cuts – even if fewer than previously expected – and continued growth in the economy and earnings to carry the day and support higher common stock prices over time. The major risk to stock prices over the next couple years would be the Federal Reserve needing to shift policy to a more restrictive stance to fight a rekindling of inflationary pressures, which would likely reset common stock prices lower.

While the Federal Reserve will eventually need to pivot to fighting inflationary pressures at some point in the future, the dynamics for that next policy pivot are not currently in place. However, we will follow the new administration’s policy proposals closely to determine their potential inflationary influences. The Treasury market will undoubtedly assist in that assessment as it is always sensitive to a build in inflation expectations.

Treasury Market

Treasury Yields Remain Elevated

The somewhat remarkable rise in Treasury yields since the Federal Reserve cut the target range for the federal funds rate by a larger than expected 50 basis points at the September 17-18 FOMC meeting remains the most surprising recent development in the financial markets. Expectations for stronger real growth and concerns about the federal budget deficit and the growing interest burden of the national debt appear to be pressuring ten-year Treasury yields higher, while near term inflation concerns are having a greater impact on two-year Treasury yields.While Treasury yields did pull back from their post-election peaks, the yield on the ten-year Treasury note still ended November at 4.18%, 54 basis points higher than the 3.64% yield the day before the September FOMC meeting. The 3.64% Treasury yield was comprised of a 2.12% ten year inflation expectation and a real yield of 1.52%.

Currently, the 4.18% ten-year Treasury yield is comprised of a slightly higher ten year inflation expectation of 2.22%, a rise of 10 basis points, while the real yield is higher by 44 basis points at 1.96%. The stronger economic data over the past two months and the expectation that President Trump’s economic agenda will be pro-growth and add to the national debt led to 81% of the rise in the ten-year Treasury yield since mid-September showing up as a higher real yield.

The analysis of the 62 basis point rise in the two-year Treasury yield to 4.17% from 3.55% the week following the September FOMC meeting is quite different. The two year inflation expectation has risen by 40 basis points to 2.40% from 2.0% – 65% of the rise in the two-year Treasury yield – while the real yield has risen by 22 basis points to 1.77% from 1.55%. Investors are concerned that the combination of the Federal Reserve cutting rates and a faster pace of economic growth will cause the disinflationary trend since 2022 to stall above the Federal Reserve’s 2% target.

With the yield on the two-year Treasury note 51 basis points below the 4.68% midpoint of the current target range of the federal funds rate, the market is not expecting a further material drop in the target range for the federal funds rate. This is consistent with our view that the Federal Reserve will cut rates at most three more times to June of next year. This somewhat more restrictive monetary policy stance should help keep the disinflationary trend in the economy in place, just at a slower pace than has been experienced over the past two years.

As we mentioned in the October Investment Strategy Statement, in a steady state environment the yield on the ten-year Treasury note tends to settle in at a level near the growth rate of nominal GDP. An inflation rate and a real growth rate both in the range of 2% to 2.5%, would be consistent with a yield on the ten-year Treasury note in a range of 4.0% to 5.0%, compared to the current yield of 4.18%. Where the yield on the ten-year Treasury note trades over the next year will be determined by how the policy proposals of the Trump administration unfold next year and how they impact the economy.

In this environment, investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve, while also modestly extending duration to lock in yields on intermediate term – four to seven year – fixed income securities.

Even though yield spreads on both investment grade and non-investment grade corporate securities to Treasury securities are below average, it appears to be worthwhile to increase corporate bond exposure as we expect the soft landing scenario to continue to play out, with the economy in the early stages of an elongated economic cycle. In this environment, yield spreads are not likely to widen to any significant degree.