Deflation of Trade Tensions Sends Stocks Climbing

6/1/2025 (Updated: 4/3/2026) - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

While we do not view the temporary trade deal with China as an “all clear” signal, it is clearly a major positive compared to the back and forth hiking of tariffs between the U.S. and China in the aftermath of the reciprocal tariff announcements on April 2. We view it as a “more clear” signal and shift in tone which helped stocks recover from their overshoot to the downside to the recent low on April 8.

Equity Markets

A Further De-Escalation of Trade Tensions Sends Stock Prices Higher

Investors celebrated a meaningful de-escalation of U.S.-China trade tensions following successful negotiations between U.S. and Chinese officials in Switzerland over the weekend of May 10-11. The U.S. tariff on Chinese goods was lowered to 30% from 145%, while China tariffs on U.S. goods were lowered to 10% from 125% The U.S. and China agreed to maintain the new tariff levels for 90 days with the goal of working toward a more comprehensive trade deal in further talks.The trade deal ended, for the time being, the de facto trade embargo between the two nations that developed after President Trump announced the Administration’s reciprocal tariff agenda on April 2. The temporary trade deal was negotiated amid warnings of empty retail shelves, plunging shipping container traffic, and small business failures.

Following the announcement of the trade deal, stock prices jumped with the DJIA gaining more than 1100 points on May 12. The markets quickly priced out a summer rate cut by the Federal Reserve, pointing to the first rate cut happening in the fall, and reduced the number of expected rate cuts this year from three to a toss-up between one and two cuts.

Taken with the trade agreement with the United Kingdom a couple days earlier, it is clear the Trump administration is focused on de-escalating a punishing trade war that was placing the U.S. economy, as well as the world economy, at risk. The agreement with China reset the tone between the world’s two largest economies from an almost complete shutdown of trade to a constructive agreement that allowed time for negotiations and lowered the risk of the U.S. economy falling into recession.

The timing and the extent to which the Trump Administration has backtracked on the initial reciprocal tariff proposals indicates that the President’s pain threshold for damage to the economy from tariffs is lower than many investors feared. The looming economic damage proved to be too risky to be politically sustainable as the electorate did not vote for a recession or still higher prices. The very real threat of significant product shortages, hefty price hikes, and rising unemployment were major incentives to start the process of lowering tariffs to a more manageable level with China.

The recovery in stock prices hit a speed bump mid-month on the one-two punch of Moody’s Rating stripping the U.S. of its last triple-A credit rating and the realization by investors that the tax legislation working its way through Congress cannot provide economic stimulus without further worsening an already alarming trajectory for the national debt over the next decade. In response, the yield on the thirty-year Treasury bond reached its highest level in 18 years at 5.15%, before finishing the month at 4.93%.

The latest twist in the tariff saga occurred late last week when the U.S. Court of International Trade blocked President Trump’s reciprocal and fentanyl tariffs imposed in April, though the ruling does not affect the smaller sectoral tariffs. The Administration appealed the ruling and a federal appeals court granted the request to temporarily pause the lower court ruling the following day. The Supreme Court could end up having the final say in the case. There was a very limited response in the markets because the general assumption is that the Trump administration will find other avenues to impose tariffs if the ruling of the appeals court is overturned.

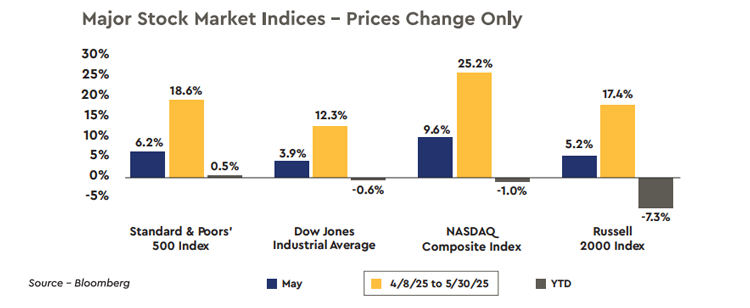

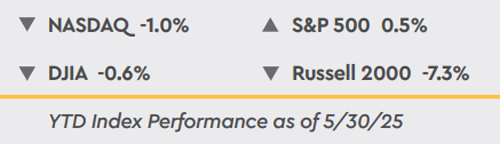

Despite the sharp and sudden drop in stock prices to the recent low on April 8, the large company stock market measures ended May close to where they started the year as trade tensions eased. The S&P 500 is slightly positive on the year with a gain of 0.5%, while the DJIA and the NASDAQ Composite are slightly negative at -0.6% and -1.0%, respectively. The Russell 2000 index of small company stocks is lower by -7.3% year-to-date.

For the month of May the major stock measures gained 3.9% to 9.6%, with the S&P 500 posting its first monthly gain since January and finishing the month within 3.8% of its record high reached on February 19. Since the recent low in stock prices on April 8 stock prices have soared with the major stock market indices higher by 12.3% to 25.2% as the Trump administration started to walk back the aggressive tariffs unveiled on April 2.

Federal Reserve Holds Rates Steady, Says Uncertainty Has Increased

The Federal Reserve maintained the target range for the federal funds rate at 4.25% to 4.50% at the May 6-7 FOMC meeting, where it has been since December. However, the policy statement warned that tariffs have increased the uncertainty about the economic outlook by raising the risks of both higher unemployment and higher inflation.

Tariffs pose a policy dilemma for the central bank, which has to decide whether to focus more on the potential for one-time price increases to become ingrained in higher inflation expectations or for a pullback in consumer spending and in hiring and investment by businesses to lead to higher unemployment. The central bank will not know the actual impact of tariffs on the economy until the full array of tariffs are put into effect. Consequently, the Federal Reserve is not in any different position relative to trade policy than the markets, businesses, and households.

Based on Chair Jerome Powell’s comments at the press conference, it appears the FOMC is confident that monetary policy is sufficiently restrictive to keep the disinflationary trend of the past two to three years in place, with no pressing need to raise rates. At the same time, the policy statement stated that “recent indicators suggest that economic activity has continued to expand at a solid pace,” indicating no need to immediately lower interest rates either.

This backdrop provided the Committee members with the latitude to wait for additional data to provide a clearer assessment of how the economy, inflation, and the labor market will be impacted by trade policy. Chair Powell stated in the press conference that “We do not feel like we need to be in a hurry. We feel like it is appropriate to be patient.”

With Chair Powell again stating that the Federal Reserve has an “obligation to keep tariff inflation contained,” it will likely take a rise in the unemployment rate above 4.5% from the current 4.2% for the FOMC Committee to restart the rate cutting cycle. The prospect of tariff-related pricing pressures makes it difficult for the Federal Reserve to pre-emptively cut rates, particularly when the economic data continues to indicate positive, albeit slowing growth. The futures market for the federal funds rate is pricing in a restart of the rate cuts by September and a total of two rate cuts by year end.

Economy to Slow, but Skirt a Recession

With the recovery in stock prices since the recent low on April 8, investors appear to be willing to look through the economic damage in April and early May from the proposed tariffs if there is some meaningful progress on trade negotiations and deals coming over the next couple months. Additionally, investors will need to look through distortions to the economic data resulting from the unpredictable tariff proposals over the past two months.

Imports were pulled forward in March as businesses were busy front-running proposed tariff increases. A payback in the second quarter was widely expected and in fact, imports fell in April and into early May, particularly from China. Now, following the temporary 90-day trade deal with China, another ramp in imports is occurring as businesses in both nations rush to take advantage of the lower tariffs in the event that tariffs go back up from current levels once the pause ends.

Until an overall, well thought out and coordinated tariff game plan is unveiled, consumers will remain somewhat defensive as fears of job losses have grown with the prospect of slower growth and higher prices. Businesses remain somewhat hesitant to go forward on hiring and investment decisions because the tariff uncertainty makes it difficult to judge whether the risk is worth taking for the potential return.

Inflation was relatively mild in April — the consumer price index was higher by 2.3% year-over-year and the core personal consumption price measure was higher by 2.5% --however, higher prices from tariffs are likely to be reported over the next couple months. Once those hopefully one-time price hikes are over, a return to the disinflationary trend of the past couple years should re-emerge as monetary policy remains moderately restrictive.

With the hit to both consumer and business sentiment from the tariff threats, we expect a slowing in the pace of economic growth, but the likelihood of the economy hitting stall speed has fallen with the thawing of trade tensions. Monthly job gains should fall to around 100,000, or slightly lower over the rest of the year, but remain positive as the tariff impact is mitigated.

The unemployment rate should rise toward 4.5%, but not much higher as labor force growth is held back by much lower immigration and as employers are likely to hoard labor given the difficulty companies had in finding quality workers following the pandemic. The economy withstood the tightening of monetary policy from March 2022 to July 2023 as the jobs market remained firm, and we expect it will withstand this year’s tariff turmoil.

Investors will increasingly focus on all three pillars of President Trump’s economic policy rather than just tariffs and trade deals as 2025 wears on. The tax bill, which is expected to include significant incentives for business investment and extend the 2017 tax cuts for households and small businesses, and efforts to deregulate certain industries beyond the current freeze on new regulations that has been in place since Inauguration Day, should provide a modest boost to the economy’s growth rate and be received positively by investors.

Markets Are Expecting a More Constructive Approach to Trade Policy

We continue to hold the position that it will take nothing short of a policy shift, i.e., a better set of economic policies, for common stocks to resume their previous upward trend and advance to new highs. The trade deal with the United Kingdom and the temporary deal with China are great first steps in the journey toward a better set of economic policies.

These first steps now need to turn into a trend which will go a long way toward calming the fears of investors and consumers and providing businesses with some clarity on the rules of the road going forward. This will set the stage for the next move higher in stock prices to take place.

While the trade deal with China was unambiguously good news, the ongoing negotiations will not be without hurdles. President Trump said the “most exciting part” of the deal was China promising to open up its markets to U.S. companies. While that may occur, this is not the first time China has agreed to open up its markets. Other issues include China’s manipulation of its currency, the subsidies it provides to the manufacturing sector, and non-tariff barriers to trade like administrative hurdles, quotas, and the threat of intellectual property theft and forced technology transfers.

After reviewing the framework of the final deal with the United Kingdom and the agreement with China, they appear to represent the ceiling and floor of the trade deals to be negotiated over the next few months. That China’s temporary deal should be the ceiling makes sense. China is a geopolitical adversary which has built up massive industrial overcapacity with which it can flood global markets with cheap goods, drive competitors out of business, and dominate key industries.

There is agreement on both sides of the aisle in Washington that U.S. dependence on Chinese supply chains places the U.S. in a vulnerable position and needs to be addressed. The trade deals with other trading partners will likely contain a mix of lower tariffs than those applied to China and custom made arrangements based on the nature of the imports.

While we do not view the temporary trade deal with China as an “all clear” signal, it is clearly a major positive compared to the back and forth hiking of tariffs between the U.S. and China in the aftermath of the reciprocal tariff announcements on April 2. We view it as a “more clear” signal and shift in tone which helped stocks recover from their overshoot to the downside to the recent low on April 8. Investors are looking beyond the trade policy transitions of 2025 to the hoped for benefits from business investment incentives and deregulation efforts that will show up in 2026.

By the end of the 90-day pause of the reciprocal tariffs put in place on April 9, several trade deals are likely to be in place. The next round of trade deals will likely be negotiated during a second 90-day postponement period. President Trump needs to put the tariff issue behind him to lower the odds of a significant slowdown in the economy and a resurgence of inflationary pressures with the mid-term elections rapidly approaching and his legacy on the line.

Markets Are Facing a Wall of Worry

There are several factors which will provide the markets with a wall of worry to climb before the major market indices can reach new record highs. First, even with the current negotiations to reduce the scale and scope of the proposed tariffs, keep in mind that they are a consumption tax on households, and potentially a profits tax on companies that import, and will likely settle out at a much higher level than at the start of the year. Second, the weak consumer and business sentiment measures will soon translate into slightly weaker economic data, which will be accompanied by some tariff-related price hikes.

Third, the tax legislation working its way through Congress cannot provide economic stimulus without adding trillions of dollars of additional debt to the current projection of a $22 trillion increase in the national debt over the next ten years by the Bipartisan Policy Center. Fourth, the tariff-related pricing pressures will keep the Federal Reserve on the sideline until the labor market weakens and the unemployment rate rises.

Lastly, while efforts to de-escalate trade tensions have been somewhat erratically pursued over the past seven weeks, investors were reminded late last month that President Trump is prone to use tough talk to gain leverage in trade negotiations, which raises uncertainty over which tariffs will be implemented, at what level, and for how long. President Trump shocked the markets, once again, by threatening a 25% tariff on Apple if the company does not start manufacturing iPhones in the U.S. and by recommending a “straight 50% tariff” on the European Union after complaining that trade negotiations had stalled.

In a pattern that is becoming increasingly familiar, less than 48 hours after threatening higher tariffs on the European Union, President Trump agreed to delay the 50% tariffs to July 9 following a request from the President of the European Commission, Ursula von der Leyen. She said the European Union needed until July 9 to “reach a good deal,” and that “Europe is ready to advance talks swiftly and decisively.”

President Trump’s latest tariff threats again highlighted the challenge for investors, households, and businesses eager to move on from a global trade war that can come back into focus at any moment. With the President always looking to gain an advantage in negotiations, tariff threats could remain an issue for businesses and the stock market for the duration of President Trump’s term in office.

While there is plenty to challenge the stock market in the near term, the outlook for common stocks ultimately comes down to the outlook for the economy and earnings. Jobless claims, credit yield spreads, consumer spending, and continued jobs growth all point to positive growth in the economy, albeit at a slower pace. Long term investors need to look past near term hurdles as the process of de-escalating the risks from tariffs is underway with the trade negotiations and to focus on the better news expected in the back half of the year, namely strong incentives for businesses to invest and an aggressive deregulatory agenda.

Fixed Income Markets

U.S Credit Rating Downgraded, Again

Mid-month Moody’s Ratings service downgraded the credit rating of U.S. debt to Aa1 from Aaa, one notch below the top triple-A rating. The nation’s credit rating was initially downgraded by Standard & Poor’s in August 2011 and by Fitch in August 2023. In the latest downgrade, Moody’s cited the government’s persistent failure to adopt measures that would “reverse the trend of large annual fiscal deficits and growing interest costs.”

The Moody’s downgrade simply reminded investors what they already knew. Namely, the U.S. is on an unsustainable debt trajectory. Consider that the federal budget deficit this year is on track to match, or slightly exceed, the $1.83 trillion deficit for fiscal year 2024. The national debt will reach $37 trillion this year and interest payments on the national debt are projected to exceed $950 billion in fiscal year 2025. Nearly $1 of every $7 the U.S. spends goes toward paying interest, more than the country spends on defense.

The problem is spending, which neither political party is willing to address. Tax revenue this year is expected to be roughly 17% of nominal gross domestic product, right in line with the 17.2% average from 1995 through last year. Spending is another matter, however, as it is projected at 23.4% of GDP this year, compared to an average of 21.1% from 1995 to 2024. In fiscal year 2024, the federal budget deficit was 6.4% of GDP, which is unheard of when the economy is growing and there is no war or emergency.

Under the House GOP budget plan, the federal shortfall is expected to exceed 7% of GDP for a decade. The net result is that investors are likely to require increasingly higher real yields on Treasury securities to fund the national debt. Pressure on the federal budget will intensify as debt service costs rise further and the value of the U.S. dollar could come under pressure. Ultimately, higher Treasury yields will raise the cost of capital for all borrowers.

Treasury Yields Rose in a Persistent Manner during May

Treasury yields rose in a persistent manner during May fueled by a mix of receding recession fears, lingering worries about inflation, and growing concerns that ever larger federal budget deficits will require ever larger issuance of Treasury securities. Until proven otherwise, real yields on Treasury securities are likely to continue to rise as the currently proposed tax and spending legislation provides no evidence that Washington has any intention of addressing the nation’s worsening budget deficit and debt problems.

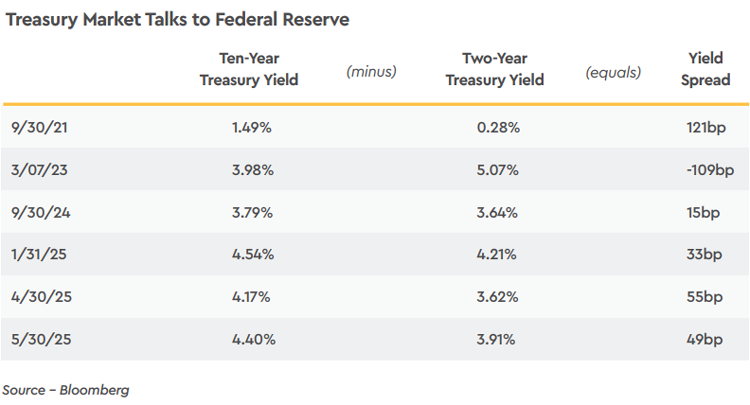

The yield on a two-year Treasury note rose from 3.62% at the end of April to 3.91% as recession fears fell with the easing of trade tensions with China. Expectations on the timing of rate cuts by the Federal Reserve were pushed out and the extent to which the target range for the federal funds rate could be lowered was reduced. Inflation expectations over the next two years fell -2 basis points to 2.76%, meaning that more than 100% of the 29 basis point rise in the two-year Treasury yield was due to expectations for better growth and increased issuance of Treasury debt with the real yield rising to 1.15%.

On the longer end of the Treasury yield curve, the yield on ten-year Treasury notes rose to 4.40% from 4.17% at the end of April. Eleven basis points of the rise in yield reflected a higher inflation expectation at 2.33%, while the real yield rose 12 basis points to 2.07%, largely reflecting the massive borrowing requirements given the largely out of control deficit spending of the federal government.

In this environment, investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve because investors fear massive issuance of Treasury securities, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.

Even though yield spreads on both investment grade and non-investment grade corporate securities to Treasury securities are below average, it appears to be worthwhile to increase corporate bond exposure given that credit yield spreads are modestly wider than at the start of the year. Additionally, the likelihood of the soft landing scenario playing out has increased with the thawing of trade tensions, leaving the economy in the early to middle stage of an elongated economic cycle. In this environment, yield spreads are not likely to widen to any significant degree.