Markets Respond to Trump Tariff Policy

5/1/2025 (Updated: 4/9/2026) - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

Considering the market reaction on April 3 and then six days later on April 9, we think peak market volatility has passed. The announcement of the reciprocal tariffs provided investors with a glimpse of the worst possible impact on the economy from the tariffs, while the reaction in the stock and bond markets gave an indication of the possible downside risk to the markets.

Equity Markets

Markets Respond to Trump Tariff Policy

Investors entered April anticipating the release of President Trump’s reciprocal tariff agenda on April 2. The hope was that the Administration would unveil a comprehensive, well-thought-out and coordinated tariff game plan designed to level the tariff playing field with U.S. trading partners. Instead, President Trump stunned the markets by unveiling a baseline 10% tariff on all imported goods and significantly higher reciprocal tariffs to be applied on all trading partners -- friend and foe alike -- including 34% on China, 24% on Japan, 46% on Vietnam, and 20% on the European Union. The suite of tariffs announced on April 2 amounted to a “worst case scenario” relative to expectations, causing recession fears to mount.

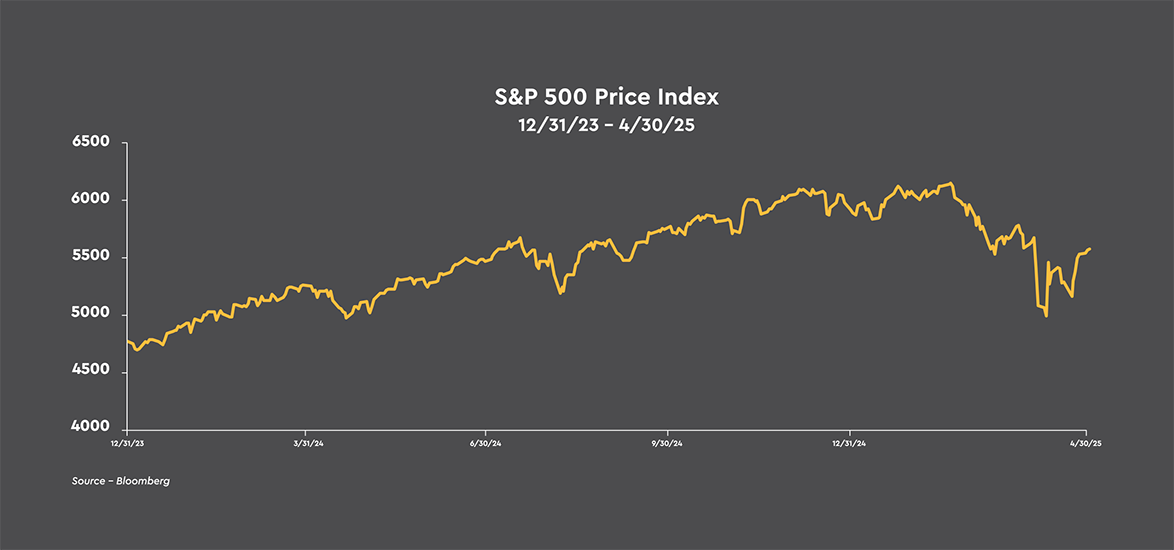

Instead, President Trump stunned the markets by unveiling a baseline 10% tariff on all imported goods and significantly higher reciprocal tariffs to be applied on all trading partners -- friend and foe alike -- including 34% on China, 24% on Japan, 46% on Vietnam, and 20% on the European Union. The suite of tariffs announced on April 2 amounted to a “worst case scenario” relative to expectations, causing recession fears to mount.Following the tariff announcements after the market close on April 2, the stock market suffered its steepest decline since mid-February to late March of 2020 at the inception of the pandemic. Over the following four trading days, the S&P 500 dropped -12.1%, while the NASDAQ Composite declined -13.3%. From the recent record highs on February 19, the S&P 500 declined more than -20% on an intraday basis, but missed hitting bear market territory on a closing basis by dropping -18.9%, while the NASDAQ Composite reached bear market status with a decline of -23.9%.

With the onslaught of tariff announcements, from late February to the April 2 reciprocal tariffs, the dynamics for a significant slowdown in the pace of economic activity began to build at a rapid pace. Consumers turned increasingly defensive with consumer sentiment measures cratering. Businesses have become increasingly hesitant to make hiring and business capital spending investments because they do not know what the tariff framework will be, making it difficult to estimate the potential returns on future investments.

The longer the oppressive tariff rates had remained in place, the higher the likelihood of recession and the stronger its potential severity would have grown. Attempting to fundamentally restructure supply chains and economic and trade relationships across the world in short order ushers in an uncertain new global trading era that threatens the economic order.

On Wednesday, April 9, President Trump dramatically reversed course by partially walking back the aggressive tariffs on U.S. trading partners that he announced on April 2, but singled out China for an even bigger tariff of 125%, bringing the total tariff on Chinese imports to 145%. Rather than negotiate, China retaliated with 125% tariffs on imports from the U.S. President Trump has markedly escalated his trade war with China, bringing the world’s two largest economies the closest to a full economic decoupling since China began to rejoin the global trading system in the 1980s.

The President said his 10% baseline tariff on virtually all imports would stay in effect, but he paused for 90 days the steep reciprocal tariffs and signaled a willingness to negotiate on trade. The White House claimed the pause in the reciprocal tariffs was always the strategy, suggesting the announcement of massive reciprocal tariffs was designed to gain leverage in trade negotiations and to give the trading partners of the U.S. a reason to sit at the negotiating table.

The S&P 500 skyrocketed 9.5%, the index’s third largest one day gain since World War II, following the announcement of the pause on reciprocal tariffs. The NASDAQ Composite jumped 12.2%, notching its second best daily gain ever. A key reason stocks rallied following the announcement of a 90 day pause was the significant shift in the messaging from the White House, letting investors know the Administration had begun negotiations and planned on continuing negotiations with its trading partners.

The first two weeks of April were among the most volatile periods in the history of the stock market, rivaling shutting down the economy in March 2020 and the Black Monday week in October 1987. The market response only seems fitting as the tariff policies announced by President Trump on April 2 were the most disruptive set of economic policies we can recall in our lifetimes.

A troubling selloff took place in the Treasury market over the three days prior to President Trump pausing the reciprocal tariffs. The yield on the ten-year Treasury note rose from 3.99% to 4.47% despite the mounting fears of a recession. This represented the steepest three day climb in ten-year Treasury yields since 2001. Not coincidentally, the value of the U.S. dollar dropped -6.5% against a basket of foreign currencies since the beginning of April.

Such selling pressure in the markets for Treasury securities and the U.S. dollar is very unusual because normally investors flock to these assets during times of market distress. It prompted speculation that U.S. trading partners could be boycotting the Treasury market in retaliation to the tariffs, and that investors were losing confidence in U.S. policymakers. The turbulence in the Treasury market was likely the final straw that forced President Trump’s hand to pause the reciprocal tariffs, because capital flight can turn a prosperous country into one with poor growth prospects rather quickly.

As if tariff-related uncertainty and volatility were not enough, President Trump added another source of uncertainty to the markets by ramping up his criticism that Chair Jerome Powell is not lowering interest rates to cushion the fallout from his trade war. The President lashed out at the Federal Reserve Chair, renewing threats to remove the leader of the central bank.

It should be no surprise that markets responded negatively to the President threatening the independence of the central bank. President Trump subsequently backpedaled on his threats to fire Mr. Powell by saying he had “no intention” of firing the Federal Reserve Chair before his term heading the central bank ends in May 2026. The President’s about-face was a clear positive as it seemed to tame one of several destabilizing factors that have roiled markets over the past couple months and lowered the odds that the U.S. will enter a recession this year.

The Trump administration also signaled the President was open to taking a less confrontational approach to trade talks with China, including a new willingness to lower the current steep tariffs on China. Treasury Secretary Bessent stated in a private investor summit that he expects “there will be a de-escalation” in the China trade war in the “very near future” and that “no one thinks the current status quo is sustainable.” Again, it should be no surprise that markets responded negatively to 145% tariffs on imports from China.

The current efforts to negotiate the proposed reciprocal tariffs, the Treasury Secretary’s optimism that both China and the U.S. do not want the current all out trade war between the countries to continue, and that he believes a deal with China can be reached provided a lift to stock prices over the back half of April. While the losses on the month were reduced, the S&P 500 still closed the month -1.8% below its closing level on April 2.

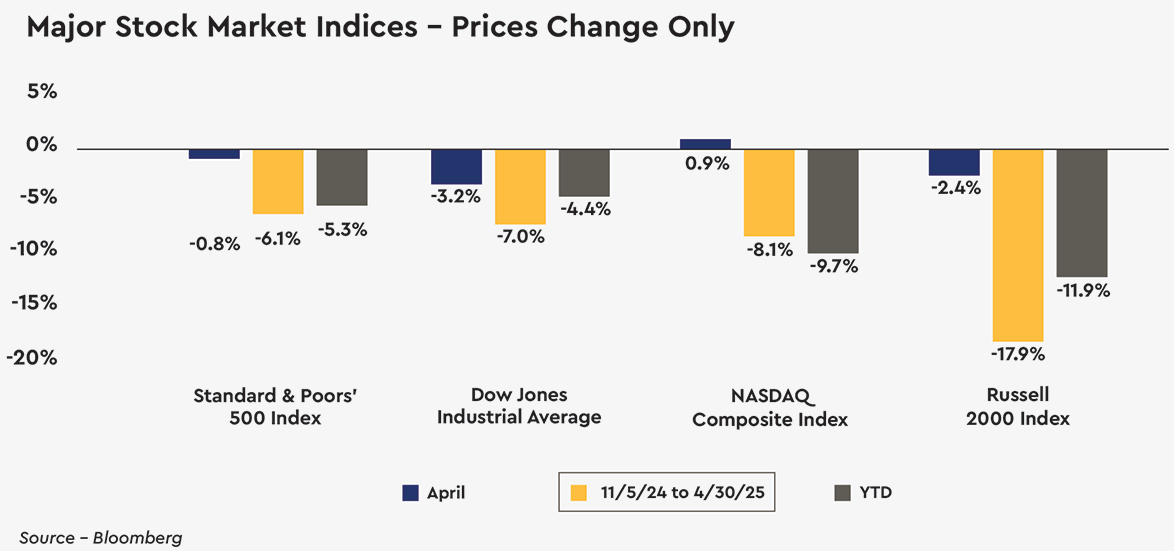

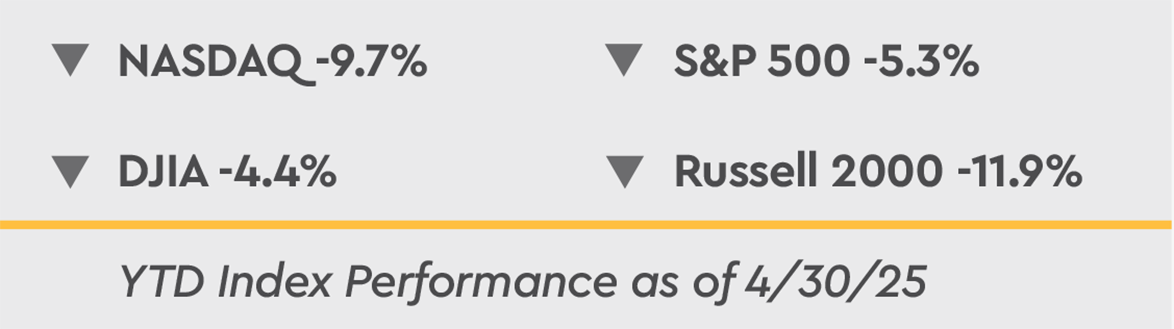

For the full month of April, the NASDAQ Composite actually posted a small gain of 0.9%, while the S&P 500 fell -0.8%. Over the first four months of 2025, the major market indices have fallen -4.4% to -11.9%. Since the presidential election, the S&P 500 has fallen -6.1% while the Russell 2000 index of small company stocks is lower by -17.9%.

Tariff Threats Distort First Quarter Data

Economic activity in 1Q 2025 was significantly distorted by President Trump’s threats of materially higher tariffs on goods imported to the U.S. The trade deficit exploded last quarter as businesses were busy front-running the proposed tariff increases. Imports soared at a 41.3% annual rate driven by a 50.9% increase in goods, leading to net exports subtracting -4.8 percentage points from the real GDP growth rate of -0.3% reported for the first quarter. That was the largest quarterly drag on growth from net exports on record dating back to 1947. By comparison, the economy grew 2.5% over the four quarters of 2024.A portion of the imports were temporarily stockpiled in inventories, causing the change in business inventories to add 2.3 percentage points to the economy’s growth rate. Netting out the negative impact from net exports due to the surge in imports and the positive impact from the inventory build, the growth in real GDP in the first quarter was reduced by -2.5 percentage points, resulting in the economy’s slightly negative growth rate. The last time the economy reported a negative growth rate was 1Q 2022 at -1.0%, which also resulted from a deterioration in the trade deficit, although the overall economy did not slip into recession.

Consumer spending slowed to a 1.8% rate last quarter, lower than the 3.1% advance over the four quarters of 2024. Households have turned cautious as recession fears and concerns over job security have increased. However, durable goods purchases surged at a 46.2% annual rate in March as consumers stepped up their purchases of motor vehicles to get ahead of the 25% tariff on automobiles. Business capital spending was the strongest sector of the economy, growing at a 9.8% annual rate in 1Q 2025, primarily driven by a 69.3% surge in information processing equipment that likely also reflected a tariff-related pull forward. Housing outlays gained a modest 1.3% as affordability conditions continue to hold back the housing market.

The inflation data for the quarter provided several mixed messages, with the GDP price index rising at a 3.7% rate compared to a 2.3% pace in 4Q 2024. Likewise, core personal consumption prices rose at a 3.5% rate, higher than the 2.6% pace in the previous quarter. However, core personal consumption prices were unchanged in March and were higher by 2.6% year-over-year, down from a 2.9% gain in December.

The economy did not slide into recession last quarter as the core economy -- consumer spending, business capital spending, and residential construction outlays -- grew at a 3.1% annual rate, but admittedly did experience a number of tariff-related shifts in spending patterns. The economy’s reported growth rate for the current quarter will be impacted by an inventory drawdown and a reversal of the import surge, while the consumer and business pull forwards will lapse at some point in the quarter.

While we still do not see a recession as the most likely outcome, the continued uncertainty around tariff policy will drive businesses to delay and defer investments and hiring, and anxious consumers to pull back on spending, which will likely lead to at least a stall in the economy’s forward momentum. As such, our baseline forecast for the economy is not as rosy as it was at the start of the year.

We look for growth to slow to a pace close to zero, with the unemployment rate heading toward 4.5%, and possibly higher, depending upon how the tariff agenda plays out, and a one time increase in prices on imported goods that will flow through the economy. Tariffs will also lead to shortages of consumer goods and for businesses that source goods and components from abroad.

We continue to be more worried about growth than a resurgence of inflationary pressures, as we expect the Federal Reserve will lean against the pricing pressures resulting from tariffs by waiting on actual weakness in the labor market and in consumer spending before resuming rate cuts. Our view remains that the economy is in the midst of an elongated cycle, however, the disruptive tariff policies of the Trump administration is bringing about a meaningful mid-cycle slowdown.

Difficult Trade-Off for the Federal Reserve

As for monetary policy, the Federal Reserve is facing a major conundrum. Growth is expected to slow, best highlighted so far by the significant drop in energy prices and the plunge in consumer sentiment measures. Oil prices have fallen -19.7% since early April, and the University of Michigan consumer sentiment measure hit its second lowest reading in the history of the survey last month.Typically, lower growth expectations would lead the Federal Reserve to cut rates. The problem is that the one year inflation expectation embodied in the Treasury market has jumped to 3.2% from 2.2% at the end of March, while the latest read from the University of Michigan consumer sentiment survey saw the one year inflation expectation surge from 5% to 6.5%. That backdrop makes it difficult for the Federal Reserve to pre-emptively cut rates.

On two occasions last month, Chair Jerome Powell warned that the Federal Reserve could have less flexibility to quickly cushion the economy from the fallout of President Trump’s tariff policy. He expects consumers to face both higher prices and a softer labor market as a result of the tariffs in the short run. While Mr. Powell stated that the central bank would weigh how far inflation is from its 2% target and the degree of stress in the labor market, he emphasized that the Federal Reserve had an “obligation to keep tariff inflation contained.”

With Chair Powell hinting that the central bank will prioritize its 2% inflation target over its labor market mandate in the short run, we assume the Federal Reserve will focus on ensuring that any one time increases in prices from tariffs do not turn into persistent price increases, which is consistent with the body politic’s deep distaste for inflation. The Federal Reserve will closely monitor longer term inflation expectations embodied in Treasury securities and will likely need to see an increase in the unemployment rate above 4.5% before cutting rates. The futures market for the federal funds rate is pricing in another pause in May, followed by 75 to 100 basis points of rate cuts this year starting in June.

Market Pullback Providing Long Term Investors with a Buying Opportunity

Following President Trump’s initiatives on tariffs, there is much less certainty than during “normal” times. The policy framework has been changing on an almost daily basis, including weekends. Whether the approach was intentional or mercurial and reactive, uncertainty has risen across the markets and the economy, resulting in higher risk premiums on common stocks, Treasury securities, and the U.S. dollar, and wider yield spreads on corporate debt securities.The real-world realities versus President Trump’s campaign agenda of a more self-sufficient U.S. economy began to hit in April shortly after the April 2nd ‘Liberation Day’. Trump’s campaigned on increasing domestic manufacturing of critical goods, reducing imports in general, controlling illegal immigration, easing regulatory burdens on the private sector, and creating a smaller, more efficient federal government. However, investors are concerned that this transition is disruptive, especially given the President's current approach. This disruption could lead to higher inflation, at least temporarily, and an increased risk of a short-term recession.

As tariffs and trade policy have almost single-handedly disrupted the financial markets, it will take nothing short of a policy shift i.e., a better set of economic policies, for common stocks to resume their previous upward trend. Specifically, the White House has stated that negotiations with more than 100 nations over the reciprocal tariffs are taking place. Actual progress on those negotiations, including the announcement of new trade deals, would go a long way toward calming the fears of investors and consumers and providing businesses with some clarity on the rules of the road going forward.

It is expected that the new trade deals will include commitments to purchase more U.S. made products, including agricultural products, defense equipment, energy products, manufactured goods, and services. Additionally, we expect commitments to investment in the U.S., the elimination of quotas and non-tariff barriers, and access to previously closed markets. Given the necessity for foreign countries to have access to the largest consumer economy in the world, we expect tariffs on U.S. goods to be significantly reduced and greater access to foreign markets to become the norm.

Considering the market reaction on April 3 and then six days later on April 9, we think peak market volatility has passed. The announcement of the reciprocal tariffs provided investors with a glimpse of the worst possible impact on the economy from the tariffs, while the reaction in the stock and bond markets gave an indication of the possible downside risk to the markets. The indiscriminate selling that took place following the announcement of the reciprocal tariffs reflected extremely negative investor sentiment and capitulation on the part of many investors.

The Trump administration has every incentive to make sure that the policy mix will ultimately be positioned and implemented in a manner that is beneficial to the economy, earnings, and common stock prices with the mid-term elections rapidly approaching and the President’s legacy on the line. Despite the President’s insistence that he is not fazed by the current volatility in the markets, the timing of his backtracks and policy accommodations make it clear that he and his advisors are paying close attention to how Wall Street and major corporate chieftains respond to his policy agenda.

The process of de-escalating the risks from tariffs is underway with the trade negotiations. Unfortunately, uncertainty will remain high until the markets see some positive trade developments. However, we remain optimistic about the long run given the inherent dynamics of the U.S. capitalistic economy to drive higher levels of earnings through innovation, creativity, self-interest to grow, and the desire for higher standards of living. Corporate America is unbelievably adept at quickly adjusting to unexpected macro impacts. Unfortunately, with the current economic threat being tariff policy, the adjustment process could come at the expense of jobs and the pace of job creation in the short run.

Tariff clarity and resolution is on the horizon, and combined with the Federal Reserve eventually pursuing a more accommodative monetary policy, oil and gasoline prices falling, and Treasury yields off their recent peaks, the dynamics for new highs in the major market measures, possibly as soon as during the back half of the year, are in the process of developing.

Additionally, it seems to be fairly risky for long term investors to bet against an array of outcomes which could boost investor sentiment in the near term, including the Federal Reserve restarting the rate cutting cycle, major progress on a new pro-growth fiscal package which preserves the 2019 tax cuts, more equitable trade relationships with fewer barriers to entry for U.S. exports than expected a month or so ago, and a cease fire in Ukraine. Keep in mind the completely unexpected, explosive rally in common stocks on April 9.

While we anticipate that the markets will remain volatile in the months ahead as tariff uncertainty will remain high for some time, we think there is a good chance the low in stock prices for this cycle was established on April 8. The pace of new trade deals and the extent to which tariffs and trade barriers are reduced on a global basis will play a major role in settling down the markets and restoring the forward momentum in the economy. Ultimately how the economy and earnings play out over the next couple quarters will determine if the low is already in.

Fixed Income Markets

Treasury Yield Curve Steepens Further

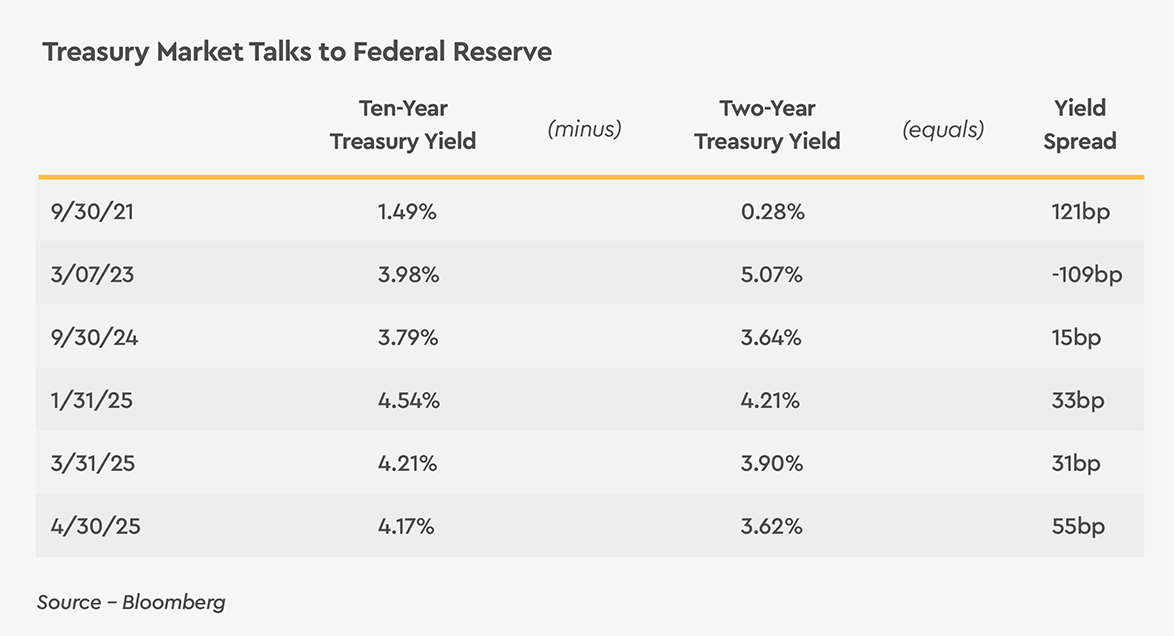

The Treasury yield curve steepened further during April, rising from 31 basis points at the end of March to 55 basis points, the yield curve’s steepest level since early February 2022 prior to the Federal Reserve starting to tighten monetary policy. More than 100% of the steepening resulted from a -28 basis point drop in the yield on the two-year Treasury note as markets priced in a greater likelihood of the Federal Reserve cutting rates as there is general agreement that the tariff policies of the Trump administration will put a dent in the economy’s forward momentum.It is interesting to note that the -28 basis point drop in the two-year Treasury yield to 3.62% last month partly resulted from a -10 basis point drop in inflation expectations over the next two years despite concerns that tariffs will bring higher prices. It seems investors are focused on a softening in the economy reinforcing the current trend toward lower inflation resulting in inflation resuming its decline toward the Federal Reserve’s 2% target in 2026.

The -4 basis point decline in the yield on ten-year Treasury notes to 4.17% during March was driven by a -14 basis point drop in ten year inflation expectations to 2.22%. It appears the dislocation in the Treasury market mid-month when the ten-year Treasury yield spiked to 4.47% had some lingering impact on the level of longer dated Treasury yields with the real yield rising 10 basis points.

Investors are also clearly concerned about the federal government's ongoing dismal fiscal situation. The federal budget deficit is on track to match the $1.83 trillion deficit for fiscal year 2024. With the national debt on track to hit $37 trillion this year, and interest payments on the national debt projected to exceed $950 billion in fiscal year 2025, investors are requiring higher real yields to finance the largely out of control deficit spending of the federal government.

It will likely take a significant cooling of the economy, possibly a mild recession, to bring the yield on the ten-year Treasury below 4.0%. Since we are looking for the economy to approach stall spread over the next couple quarters, the ten-year Treasury yield could drop a touch, but we think it is unlikely that it will fall materially below 4.0%. With the two-year Treasury note yield 76 basis points below the midpoint of the current target range for the federal funds rate, it will likely take more than three rate cuts by the Federal Reserve to move the two-year Treasury yield much below its current level of 3.62%.

Credit Yield Spreads Widen a Touch, Still Well Below Average

After widening a touch from mid-February to the end of March, yield spreads on corporate securities widened further in early April after the announcement of the reciprocal tariffs on April 2 increased the odds of recession. Investment grade yield spreads widened from 97 basis points to 121 basis points, a large move, but still below the 152 basis point average since December 1996. Yield spreads on non-investment grade corporate debt widened significantly from 355 basis points to 461 basis points, but still below the 542 basis point average since December 1996.  Following President Trump pausing the reciprocal tariffs on April 9, corporate yield spreads narrowed as recession concerns faded a touch. Investment grade yield spreads declined to 106 basis points, while non-investment grade yield spreads narrowed to 374 basis points. The message from credit yield spreads is that the risk of recession from tariffs has risen since mid-February, but a serious recession is still not the most likely outcome. We continue to expect a stall in the economy’s forward momentum this summer, rather than an actual contraction in the pace of economic activity.

Following President Trump pausing the reciprocal tariffs on April 9, corporate yield spreads narrowed as recession concerns faded a touch. Investment grade yield spreads declined to 106 basis points, while non-investment grade yield spreads narrowed to 374 basis points. The message from credit yield spreads is that the risk of recession from tariffs has risen since mid-February, but a serious recession is still not the most likely outcome. We continue to expect a stall in the economy’s forward momentum this summer, rather than an actual contraction in the pace of economic activity.In this environment, investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve because the Federal Reserve has not yet brought inflation down to the 2% target, while also modestly extending duration to lock in yields on intermediate term -- four to seven year -- fixed income securities.

Even though yield spreads on both investment grade and non-investment grade corporate securities to Treasury securities are below average, it appears to be worthwhile to increase corporate bond exposure given the recent modest widening of credit yield spreads. Additionally, while we expect the economy’s growth rate to stall over the next couple quarters, we view it as a pause in an elongated economic cycle. In this environment, yield spreads are not likely to widen to any significant degree.