Leveraging Tariff Negotiations Produce Serious Trade Deal

8/5/2025 (Updated: 4/3/2026) - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

Equity Markets

Maximum Leverage in Tariff Negotiations Produces a Series of Significant Trade Deals

The Trump Administration celebrated the 4th of July holiday by signing into law a sprawling tax and spending bill which made permanent the personal income tax rate cuts passed into law in 2017, which were scheduled to expire at the end of this year. This new legislation created new, but modest, tax cuts for tipped workers, overtime pay, and senior citizens. It created a deduction for car loan interest and expanded the cap on the state and local tax deduction, while ramping up funding for immigration enforcement and the military.

The primary stimulus in the bill is contained in tax incentives for business investment, including 100% expensing for building a factory, equipment purchases, and research and development, which will start hitting the economy in a positive manner quickly as the incentives are retroactive to the beginning of the year. Coupled with further efforts to reduce regulatory burdens in certain sectors of the economy, the primary stimulus to the economy’s growth rate is concentrated in the business sector rather than the household sector.

Trade headlines came back into focus following the holiday weekend as President Trump sent letters to several nations outlining tariff rates they will pay if they do not strike trade deals with the U.S. by August 1. The tariff rates were generally in the range of 25% to 40%, similar to the April 2 “reciprocal” tariff rates. Mid-month, President Trump also threatened Mexico and Canada -- the largest and second largest trading partners of the U.S. -- with tariffs of 35% and 30%, respectively, for those goods not covered by the United States-Mexico-Canada Agreement, and 30% on the European Union -- collectively the single largest trading partner of the U.S.

The letters effectively provided a three-week extension of the 90-day pause in the tariffs announced on April 2. With trade deals successfully negotiated with only the United Kingdom and Vietnam as of July 1, and a tenuous trade war truce with China, by turning to letters the Trump administration effectively conceded that its self-imposed 90-day deadline was too ambitious for a full teardown and rebuild of the old architecture of the U.S.-led global trading system.

The shift in the White House’s strategy reflects the challenges of completing trade agreements that address non-tariff trade barriers, commitments to invest in the U.S., foreign regulations on U.S companies, agreements to purchase goods made in the U.S., and access to foreign markets, as well as the tariff rate. Based on the pattern of trade negotiations over the past three to four months, the tariff letters were clearly more of a prod to the trading partners of the U.S. to fast-track stalled negotiations and to shake loose the best, final trade offers. Treasury Secretary Bessent stated several times last month that the letters were intended to create maximum leverage for the U.S. in the trade negotiations.

The market’s initial response to President Trump’s trade letters was fairly restrained, as investors largely took them as just part of the negotiating process as President Trump has announced a number of times that he was imposing -- and later temporarily pausing or lowering -- duties on countries such as Mexico, Canada, China, and the European Union. The pattern has been to escalate the trade conflict, only to de-escalate.

With five significant trade deals announced over the back half of the month, it appears the tariff letters helped bring several negotiations to closure. Indonesia and the Philippines agreed to tariffs on goods sold into the U.S. at 19%, with virtually no tariffs on U.S. goods. Japan agreed to a trade deal containing 15% tariffs with the U.S, which will also apply to autos, no cap on auto exports to the U.S., and a $550 billion investment in the U.S., while opening their market to U.S. goods. As July drew to a close, a trade deal with South Korea was announced, also with 15% tariffs, a commitment from Seoul to invest $350 billion in the U.S., and U.S. goods not subject to any tariffs.

The blockbuster trade deal of the month was announced on July 27 with the European Union. President Trump and European Commission President Ursula von der Leyen announced that the U.S. and the EU had agreed to the framework of a deal after negotiating in Scotland. President Trump called it “the biggest of all the deals.”

The EU agreed to 15% tariffs on most European goods, including automobiles, $750 billion of energy purchases, an additional $600 billion investment into the U.S., and significant purchases of U.S. military equipment, while opening their markets to U.S. exports with no tariffs.

A year ago, tariffs ranging from 15% to 19% would have been shocking, but currently investors and the trading partners of the U.S. are breathing a sigh of relief as worst case tariff scenarios are not playing out. These deals show that the size of the U.S. market provides powerful negotiating leverage and that the trading partners of the U.S. are willing to accept tariffs on their exports and to open up their markets in order to have access to the U.S. market and to benefit from the protection of the U.S. military.

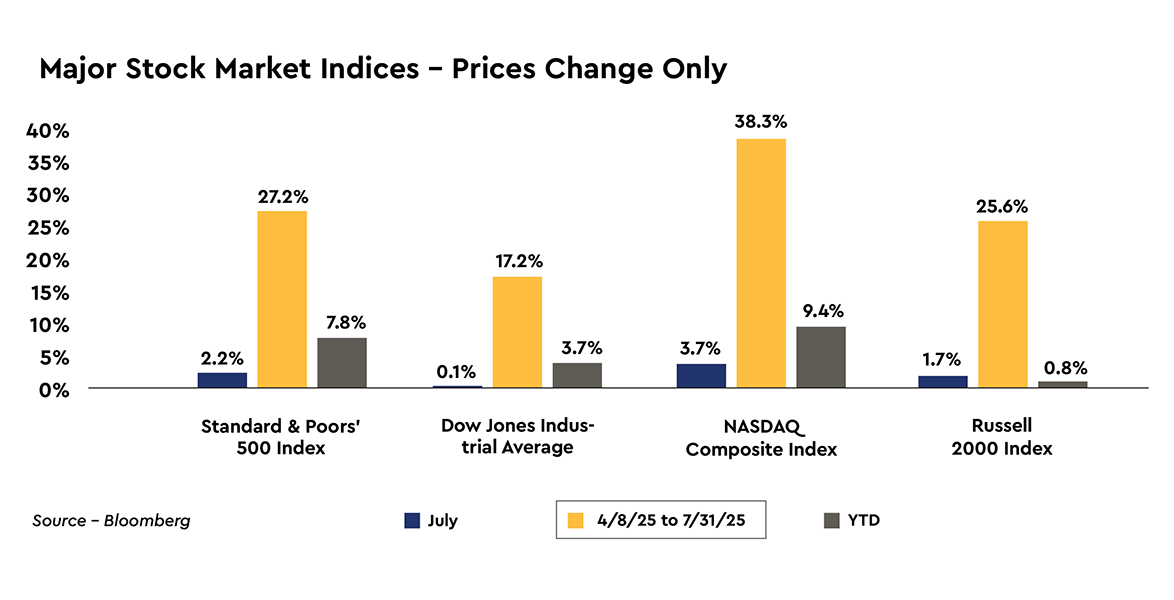

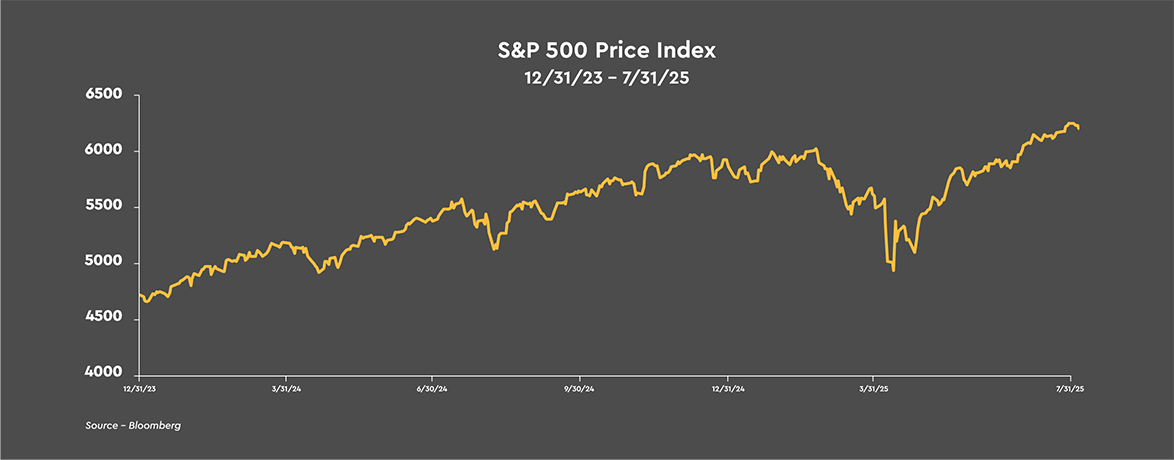

Common stock prices methodically worked their way higher over the first half of July before receiving a modest boost over the back half of the month as the announcements of significant trade deals lifted the risk appetite of investors. For the month of July, the NASDAQ Composite led the way with a gain of 3.7%, followed by the S&P 500 and the Russell 2000 posting gains of 2.2% and 1.7%, respectively. The DJIA was unchanged, rising 0.1%.

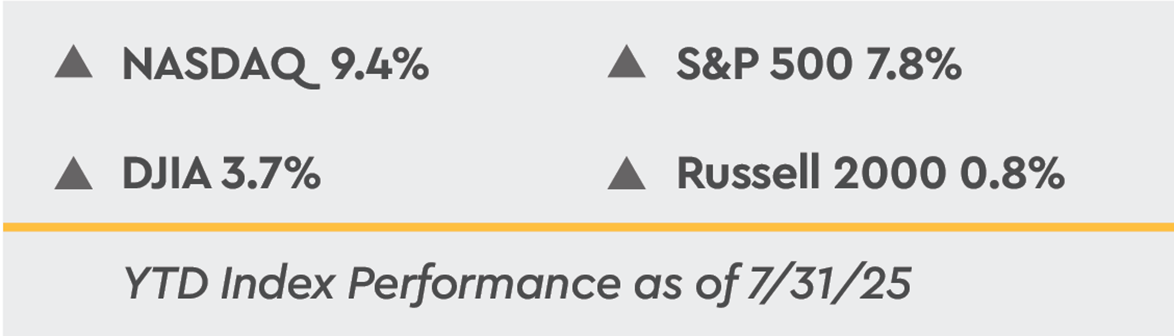

Since the recent low in stock prices on April 8, common stock prices have rebounded with the major stock market indices higher by 17.2% to 38.3%. On the year-to-date, the three large company stock measures are higher by 3.7% to 9.4%, while the Russell 2000 Index of small company stocks is lower by -0.8%.

Federal Reserve Still in No Hurry to Cut Rates

Despite unrelenting criticism from President Trump that the Federal Reserve should immediately and aggressively cut interest rates, a divided FOMC Committee held the target range for the federal funds rate steady at the August 29-30 FOMC meeting at 4.25% to 4.50%, where it has been since December. Chair Powell set a hawkish tone at the press conference by stating that “inflation is farther from our goal than employment.”

Mr. Powell emphasized that the Federal Reserve will conduct monetary policy in a manner that will keep any tariff-related pricing pressures, even if they are one-time price increases, “from becoming an ongoing inflation problem.” Chair Powell seemed to go out of his way to lower expectations that rates could be cut at the September FOMC meeting. The market odds of a rate cut in September fell to 40% after the press conference.

The decision to hold rates steady was met with opposition from two governors appointed by President Trump during his first term. Governors Waller and Bowman have advocated in recent speeches that with inflation under control and the possibility that the labor market could start weakening soon, the central bank should start easing monetary policy. This was the first time since late 1993 during the Greenspan era that two governors dissented on a rate decision.

The drama of President Trump threatening to fire Jerome Powell as Chair of the Federal Reserve intensified last month, with the Administration turning its focus to finding “cause” for Mr. Powell’s removal. The White House is alleging Chair Powell either lied to Congress about the Federal Reserve’s headquarters’ renovation or grossly mismanaged it with cost overruns potentially offering a new legal avenue to remove him.

The ramped-up pressure followed President Trump’s demand that the Federal Reserve consider federal debt service costs when setting rates, which is outside the institution’s dual mandate set by Congress of maximum employment and price stability. The markets expect that the probability of President Trump removing Mr. Powell before his term as Chair expires next May is low, primarily because such a move would be counterproductive to President Trump’s aim of lowering borrowing costs.

An attack on the independence of the Federal Reserve would raise inflation expectations, driving Treasury yields and other borrowing costs -- including car loans, mortgage rates, and many business loans -- higher, not lower. For these reasons and Treasury Secretary Bessent’s characterization of President Trump’s criticism of Chair Powell as simply “working the referees,” -- jawboning in sports parlance intended to get more favorable calls in sporting events -- we do not expect that the President will attempt to remove Mr. Powell.

To us, the far more important issue is who is chosen as the next Federal Reserve Chair, who will likely face an assumption of some level of political bias. A Trump loyalist could have a large number of dissenting voters on the Committee, or even enough to vote for a policy stance contrary to the one supported by President Trump’s appointee. That situation would seriously weaken the power of the Federal Reserve Chair and raise concerns in the markets about the internal conflict at the central bank.

Should President Trump’s appointee manage to deliver rate cuts that are not supported by the economic data, the bond market would likely push Treasury yields higher in an attempt to offset the too accommodative policy positioning at the short end of the yield curve. History says the bond market will undoubtedly win that confrontation, and the economy will be the loser.

There are only two scenarios which can bring about lower Treasury yields across the yield curve. The first, and most effective way, is patience and steadfastness in maintaining a moderately restrictive monetary policy that lowers inflation expectations, allowing nominal Treasury yields to decline in line with a moderating inflationary backdrop. The other is a significant recession, which crushes credit demand along with inflation expectations. Likely no one is in favor of the latter scenario, which leaves a patient approach that can result in a long-lasting era of low Treasury yields anchored by low inflation as the far preferrable scenario.

We expect Treasury Secretary Bessent’s influence on President Trump to result in a pragmatist being appointed to succeed Chair Powell when his term is finished next year. The target range for the federal funds rate should remain above the core rate of inflation, keeping the possibility of a very accommodative, inflationary monetary policy stance off the table. However, the spread of the federal funds rate above inflation will likely moderate from where it currently stands.

Tariffs Continue to Distort the Economic Data

The enormous trade-related distortions found in the 1Q 2025 report on the economy spurred by President Trump announcing that higher tariffs would be implemented almost as soon as he was sworn into office reversed in 2Q 2025. The trade deficit exploded in 1Q 2025 as businesses responded by accelerating their purchases of foreign goods to front run the threatened tariff increases. Imports soared at a 37.9% annual rate, leading to net exports subtracting -4.6 percentage points from the real GDP growth rate of -0.5% reported for the first quarter.

Not surprisingly, imports collapsed in the second quarter at a -30.3% annual rate, leading to net exports adding 5.0 percentage points to the real GDP growth rate of 3.0% reported for 2Q 2025. Looking through the swings in the contributions from net exports in the first two quarters of the year, the core economy -- consumer spending, business capital spending, and residential construction -- grew at a 1.7% pace over the first half of 2025. The economy’s performance so far in 2025 is a little below the economy’s average annualized growth rate of 2.1% over the past twenty years but indicates that the economy held up fairly well in the face of extreme tariff-related volatility during the first two quarters of the year.

With the consumer sector accounting for almost 70% of the U.S. economy, an important development in the second quarter data was consumer spending rebounding at a 1.4% rate compared to a weak reading of 0.5% in 1Q 2025. Solid job gains during the quarter -- monthly payroll employment averaged 150,000 -- led to real disposable personal income growing at a 3.0% rate which supported household spending during the quarter. Spending on motor vehicles led the way, advancing at a 16.2% annual rate as consumers attempted to get ahead of looming tariff-related price hikes.

Business capital spending rose at only a 1.9% rate last quarter compared to a gain of 10.3% in 1Q 2025, held back by structure outlays falling at a -10.3% rate. Businesses delayed the construction of plants and commercial space waiting to see if the bonus depreciation tax incentive would be included in the tax and spending bill. Residential construction spending declined at a -4.6% rate last quarter following a drop of -1.3% in 1Q 2025 as poor affordability conditions continue to hold back the housing market.

The best news in the report was found in the inflation data as the widely anticipated tariff-related pricing pressures did not show up in a significant way in the 2Q 2025 data. The Federal Reserve’s preferred measure of inflation, the core personal consumption price index, rose at a 2.5% annual rate compared to a 3.5% pace in 1Q 2025. From a broader perspective, the GDP price index rose at only a 2.0% rate, right in line with the Federal Reserve’s target, compared to a 3.8% pace in 1Q 2025. Easing energy prices helped moderate pricing pressures, while the squeeze on household discretionary income from the inflation surge in 2022 and 2023 showed up in lower prices for non-durable and imported goods.

Earnings Will Decide if the Stock Market Has More Room to Run in the Near Term

In reviewing the details of the completed trade deals, the effective tariff rate will end up near 15%, markedly higher than the 2.3% average tariff rate of last year, but well off the feared 25% or higher rate back in early April. Tariff revenue flowing to Treasury has soared over the past year, reaching $27 billion in June, more than three times the prior year’s amount, with the annual run rate looking to be close to $500 billion once all the higher tariffs are put in place. Higher tariff rates will represent a larger tax hike on households and will result in additional pricing pressures on imported goods in coming months.As the back and forth of tariff threats and the subsequent market reactions have taken place over the past few months, the Trump administration pursued a strategy of seeking the highest level of tariffs that do not disrupt the economy and the financial markets. The President’s aggressive tariff announcements have been used as a way of testing “what the markets would bear,” through a pattern of new tariff threats, partial retreats if the financial markets showed signs of stress, and then more threats once the markets stabilize.

As President Trump’s tariff strategy evolved over the past five to six months, uncertainty rose across the markets and the economy. With the strong rally in stock prices since the April 8 lows, it is reasonable to ask why stock prices have not come under more pronounced selling pressure over the past few months. Part of the answer is that it would have been fairly risky for long term investors to bet against an array of outcomes which could have boosted investor sentiment.

Currently those potential positive developments include the Federal Reserve restarting the rate cutting cycle, an acceleration in the economy’s growth rate in response to the business capital spending incentives contained in the recently signed tax and spending bill and further progress on lowering regulations, a cease fire in Ukraine, and unexpected progress on a wide array of workable trade deals, a development that is rapidly unfolding. Investors are keeping in mind the completely unexpected, explosive rally in common stocks on April 9 following President Trump dramatically reversing course by pausing the aggressive tariffs announced on April 2.

Once it became clear back in the late February to March timeframe that President Trump was about to unleash a far reaching tariff policy designed to fundamentally restructure economic and trade relationships across the world, we took the position that with the mid-term elections rapidly approaching and a President who kept score during his first term on the basis of economic growth and stock prices, the Trump administration had every incentive to make sure that tariffs and trade policy would ultimately be positioned and implemented in a manner that is beneficial to the economy, earnings, and common stock prices. We see no change in the incentives that the Administration faces.

It remains our view that the economy is in the midst of an elongated cycle. However, the proposed tariff policies of the Trump administration have brought about a mid-cycle slowdown as households turned defensive, fearing job losses and higher prices, and businesses increasingly became hesitant to make hiring and investment decisions. We expect the economy’s growth rate to pick up as 2025 draws to a close and remain optimistic about the long run given the inherent dynamics of the U.S. capitalistic economy to drive higher levels of earnings through innovation, creativity, self-interest to grow, and the desire for higher standards of living.

Corporate America is unbelievably adept at quickly adjusting to unexpected macro impacts and is fast at work protecting profit margins through the application of ingenuity, while keeping a close watch on expenses, sourcing new suppliers and reworking supply chains, and not allowing capacity to run ahead of demand.

The 2Q 2025 earnings reporting season arrived at a pivotal point for the stock market. The S&P 500 and the NASDAQ Composite entered earnings season trading at record highs, but the evolving tariff policy raised questions about the economy’s growth rate over the next couple quarters, near term inflationary pressures, the impact on inflation expectations, the response of the Federal Reserve in terms of interest rate policy, and, of course, the impact on corporate earnings which ultimately determine the path forward for common stock prices.

Not surprisingly, investors are seeking clarity on how the back and forth on trade has not only affected earnings, but the outlook for earnings. So far, with roughly two-thirds of the S&P 500 companies reporting, 2Q 2025 operating earnings are projected to have grown a solid 10.3% on a year-over-year basis following a gain of 5.3% in the previous quarter, with 82% of companies reporting a positive earnings surprise. This earnings momentum is impressive in light of the uncertainty households and businesses faced last quarter and should provide support for further gains in stock prices this year.

The process of de-escalating the risks from tariffs is underway and has clearly picked up steam with policy uncertainty receding at a rapid pace. While there appears to be light at the end of the tariff tunnel following the trade deals announced last month, the Trump administration has yet to strike trade deals with Mexico, Canada, and India. Meanwhile, the mid-August deadline with China when tariffs could snap back to 145% looms, although all indications are that the recent Stockholm meetings were productive.

A note of caution: while great progress was made last month on reaching trade deals, and President Trump agreed to give Mexico more time to reach an agreement by extending existing tariffs for 90 days, tariff uncertainty has not been completely eliminated. On the eve of the trade deal deadline, President Trump hit Canada with 35% tariffs from 25% and announced tariffs of 10% to 41% on dozens of smaller trading partners. Tariff threats will likely remain an issue for businesses and the stock market for the duration of President Trump’s term in office. Finally, the actual economic impact on the labor market and inflation from the higher level of tariffs need to play out over the back half of the year.

Treasury Market

Treasury Yields Back Up Modestly

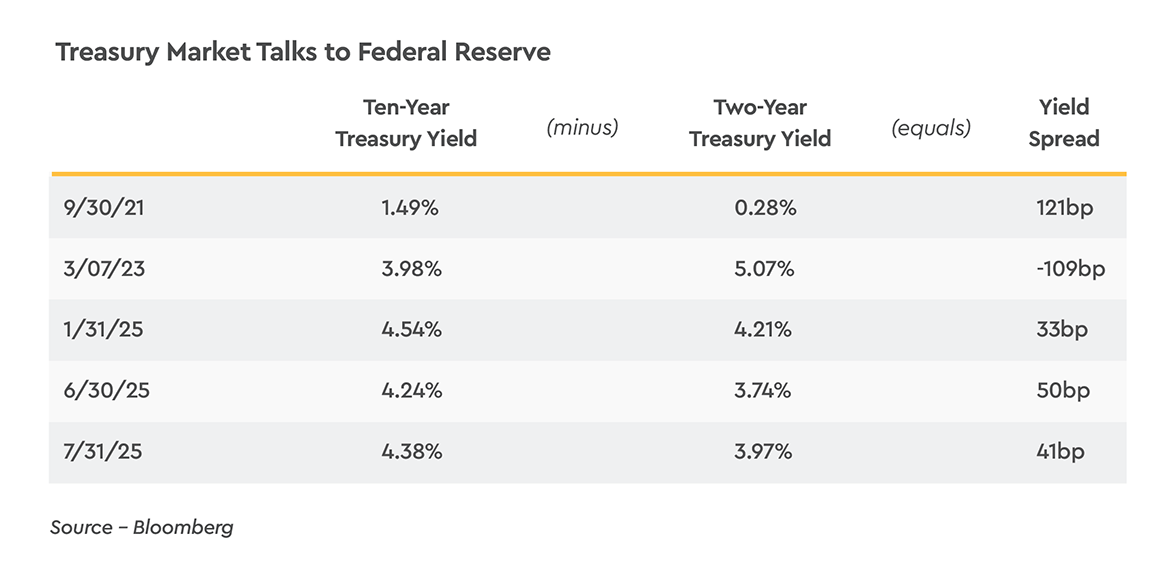

Treasury yields backed up a touch last month but stayed within the established trading ranges that have been in place since President Trump’s tariff proposals took center stage. The yield on the two-year Treasury note rose 23 basis points to 3.97%, within the 3.65% to roughly 4.0% range that has been in place since March. With the Federal Reserve on hold since December, the trading range for the two-year Treasury note has been fairly narrow and continues to point to approximately two rate cuts over the next year.A 22-basis point rise in inflation expectations to 2.92% accounted for almost all of the rise in the yield on the two-year Treasury during July. Pricing pressures resulting from the somewhat higher tariff levels than were expected just a couple months ago and concerns about the independence of the Federal Reserve partly accounted for the rise in near-term inflation expectations.

At the longer end of the Treasury yield curve, the yield on the ten-year Treasury note rose 14 basis points to 4.38%, again within a roughly 4.2% to 4.5% trading range that has been in place since mid-April once the aftershocks of the April 2 “reciprocal” tariffs worked their way through the markets. The recent range for the yield on the ten-year Treasury note is right in line with expectations for nominal GDP over the foreseeable future, with inflation trending toward the Federal Reserve’s 2% target and the economy’s growth rate building toward the economy’s 2% average growth rate since 1970. An 11-basis point rise in inflation expectations to 2.41% accounted for most of the rise in ten-year Treasury yields.

The yield on two-year Treasury notes is expected to decline in line with the Federal Reserve cutting rates over the next year, on the order of 50 basis points. This outlook assumes that President Trump’s appointee as the next Chair of the Federal Reserve does not attempt to engineer a policy rate lower than that supported by the economic data. We do not expect the trading range for the ten-year Treasury note to change much over the next few quarters, unless the economy’s growth rate deviates in large measure from the expected 2% growth rate.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve—because the Federal Reserve has not yet cut rates—and heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term (three to seven year) fixed income securities.