Major Stock Market Indices Delivered Double-Digit Gains in 2025

1/6/2026 (Updated: 2/25/2026) - By Joseph Keating - On Point Investment Strategy Statement | SouthState Wealth

Equity Markets

Major Stock Market Indices Delivered Double-Digit Gains in 2025

2025 was a tumultuous year, but ended up delivering strong gains in common stocks and solid returns on fixed income securities. The year opened with change in the wind with then President-elect Trump poised to return to the White House with many campaign promises that he looked to fulfill. This left businesses and markets to figure out how the looming policy initiatives would alter the outlook for investments, growth, and inflation. Likewise, the Federal Reserve would need to navigate what the eventual set of policies passed by Congress and by executive order would mean for growth and inflation.

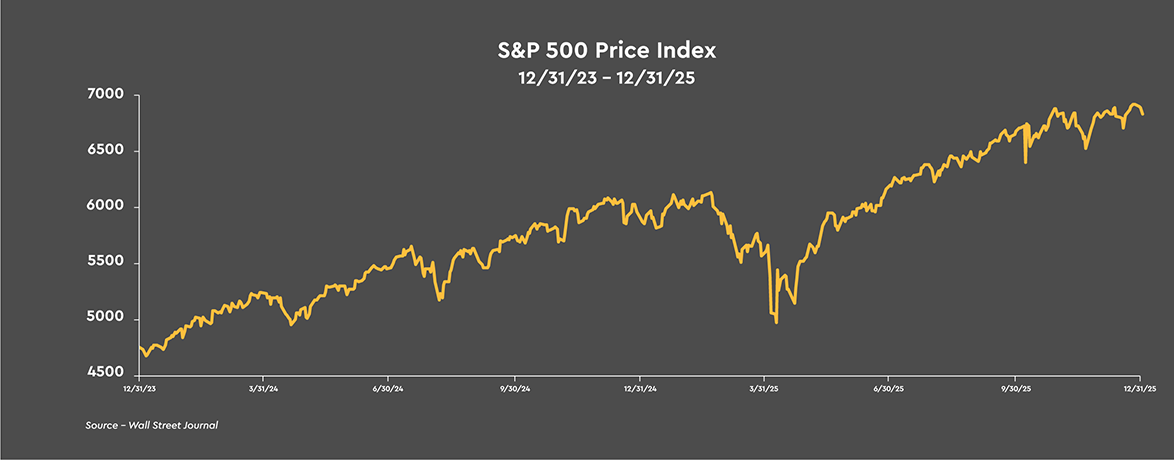

Investors, business leaders, and households spent the early part of the year digesting the scope and velocity of President Trump’s efforts to pressure U.S. trading partners into meeting the administration’s demands on trade, national security issues, and immigration, shrinking the size of the federal government, and reorienting the trade norms of the global economy. The S&P 500 hit correction territory (a drop of at least -10% from previous high) in March as mounting concerns about the outlook for the economy, punctuated by threatening tariff headlines, led to an erosion of business, consumer and investor confidence.

The growing policy fears peaked in early April following President Trump stunning the markets by unveiling a suite of significantly higher tariffs on April 2 which amounted to a “worst case scenario” relative to expectations, causing recession fears to mount. From the record high on February 19, the S&P 500 declined more than -20% on an intraday basis to the low on April 8. Common stock prices skyrocketed on April 9, however, when President Trump dramatically reversed course by significantly walking back the aggressive tariffs and signaling a willingness to negotiate on trade.

A further de-escalation of trade tensions, the passage of the sprawling tax and spending bill in early July, combined with the Federal Reserve restarting rate cuts in September and very strong earnings growth in 2Q and 3Q 2025, sent stock prices to a series of all time highs over the back half of the year. The S&P 500 hit a peak on December 24, representing a 17.9% gain on the year and a 39.1% advance off the reciprocal tariff low on April 8.

Common stock prices mostly traded sideways since early October following the lengthy shutdown of the federal government and a slump in consumer sentiment. However, the recent stall in the stock market rally was primarily due to artificial intelligence (AI)-related stocks running headlong into a strong bout of selling pressure amidst a rethink of the pace of AI capital expenditures and the enormous amount of capital required for the massive data center buildout.

Additionally, the shifting leadership among large language model developers, the potential return on investment on the enormous expenditures required to build out the AI-powered products, and questions about the aggressive debt financing several of the major hyperscalers have turned to recently to finance their AI ambitions have raised concerns about whether the buildout remains well-considered and on track.

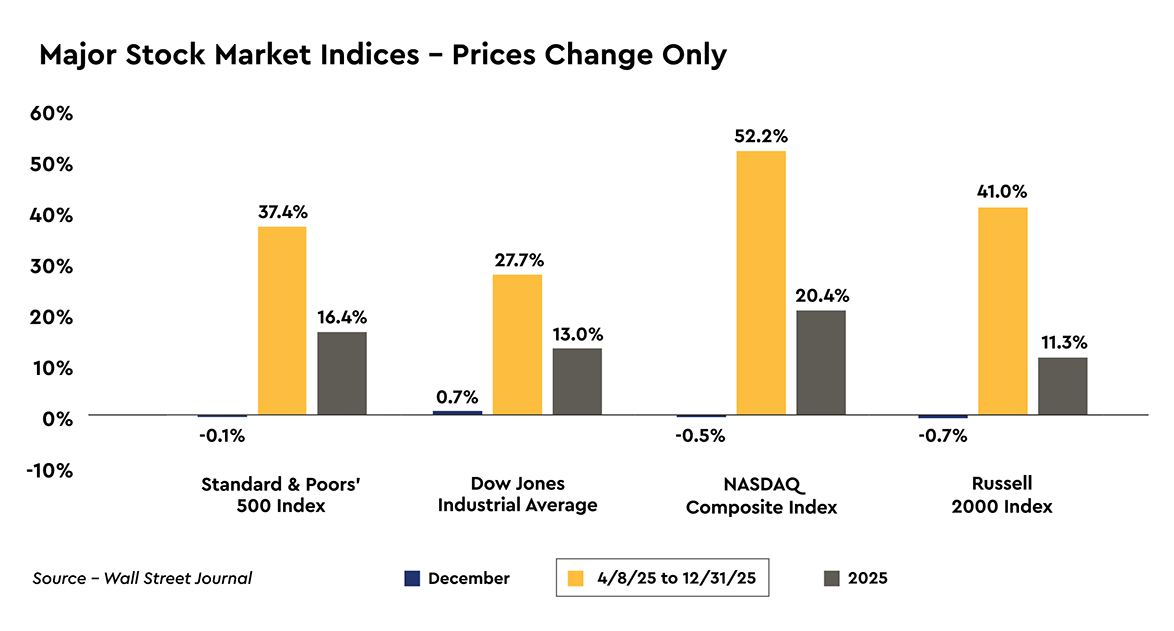

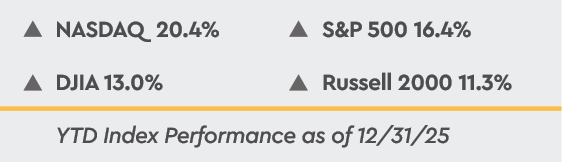

Continuing the trend since early October, the major stock market measures were largely unchanged during December with the DJIA posting a gain of 0.7%, while the other three indices fell -0.1% to -0.7%. All four major stock market indices delivered double-digit gains for 2025, however, on the order of 11.3% to 20.4% and are higher by an impressive 27.7% to 52.2% since the recent low in stock prices on April 8.

FOMC Committee Remains Divided, Policy Likely on Hold for Time Being

After discouraging hopes for a December rate cut at the October FOMC meeting, the Federal Reserve lowered the target range for the federal funds rate to 3.50% to 3.75% at the December 9-10 FOMC meeting despite having little fresh economic data to guide the decision due to the government shutdown. The Federal Reserve has now cut the federal funds rate 75 basis points over the past four months and by 175 basis points over the last 16 months.

The third rate cut of the year was far from an easy decision, with Chair Powell saying the decision to lower rates was a “close call.” The twelve person rate setting Committee delivered nine “yes” votes, two “no” votes from regional Federal Reserve Bank presidents, and recent President Trump appointee, Stephen Miran, again wanting a 50 basis point rate cut.

In addition to the two “no” votes on the rate cut, four other nonvoting meeting participants indicated that they did not support the decision to lower rates. The caution about additional rate cuts was evident in the rate projections, updated on a quarterly basis, which showed officials penciling in just one rate cut in 2026 and another in 2027.

The carefully crafted official policy statement released after the meeting repurposed language from the December 2024 FOMC meeting which ushered in a nine month pause in the rate cutting cycle. Chair Powell said the tariff increases last year were the key reason inflation remained “somewhat elevated” as goods inflation picked up. However, Mr. Powell also said the tariffs would likely create a “one-time” increase in prices and that “Our job is to make sure that it is.”

Chair Powell emphasized again that there is no risk free path for monetary policy currently as the central bank navigates the tensions between its employment and inflation mandates. Chair Powell justified the three rate cuts since September as insurance against a weakening labor market, a position he first signaled in his Jackson Hole speech in August. Mr. Powell and several Committee members are clearly worried about the jobs market as the Federal Reserve research staff believes the payroll data could be overstating job creation by up to 60,000 jobs a month since April, implying monthly job losses of 20,000 rather than the moderate monthly job gains of 40,000 that have been reported.

The biggest surprise from the meeting was the announcement that the central bank will start buying Treasury securities again, $40 billion of Treasury bills in December and likely similar amounts each month until at least April when income tax payments are due. Mr. Powell said the T-bill purchases are intended to maintain ample reserves in the banking system.

We view the dissents at the FOMC meeting as a reflection of a very uncertain outlook leading to healthy debate. The tariff policies of the Trump Administration have brought about a complicated outlook of tariff-related pricing pressures and softness in the labor market, which are impossible for the Federal Reserve to address simultaneously.

The last two rate cuts were more contested as rates approached a neutral setting which neither stimulates nor restrains the economy. Given the lack of consensus on the FOMC Committee and the arrival of a new chair of the Federal Reserve in May, it is likely the Federal Reserve will remain on hold in early 2026 as Committee members weigh incoming data. The policy statement noted that Committee members are debating the “extent and timing of additional adjustments.” We think it will take additional weak data on the labor market to spur the Committee to lower rates before the June 16-17 FOMC meeting with the newly appointed chair.

We would expect the division on the FOMC Committee to widen next year if the new chair of the Federal Reserve presses for a level of policy accommodation that is not supported by the data on growth and inflation. Another consideration is that the new chair could well enter the position in an environment where rates do not need to be lowered, as the economy should be accelerating as it moves beyond the disruptions of implementing much higher tariffs and benefits from tax refunds and business capital spending incentives.

The market is expecting short-term interest rates to fall to just over 3.0% next year, which would be consistent with inflation falling toward 2.0% with a real, or inflation-adjusted, short-term interest rate at roughly 1.0%. The current rate expectations in the market are quite a ways away from President Trump’s recent comments that short-term interest rates should be near 1.0%, however.

Strong Consumer and AI-Related Spending Drive Growth in 3Q 2025

Real GDP grew at a strong 4.3% annual rate in 3Q 2025 after growing at a 1.6% rate during the first half of the year and is higher by 2.3% year-over-year. The report, which was delayed nearly two months, showed that consumers continue to drive the economy, growing at a 3.5% pace, despite job gains which have been modest since April and weak consumer sentiment readings reflecting the high cost of necessities, along with everything from cars and homeownership to college tuition. AI-related spending also contributed to the strong quarter with both business capital spending on equipment and on intellectual property growing at 5.4% rates.

Real final sales to private domestic purchases -- a truer reflection of underlying demand from households and business -- grew at a 3.0% annual rate and are higher by 2.6% compared to a year ago. However, consumer spending is increasingly being driven by upper income households benefiting from large gains in asset values. Indications that low- and moderate-income households continue to struggle were evident in real, after-tax income being unchanged in 3Q 2025, with many households needing to dip into savings to maintain spending levels. As a result, the personal savings rate dropped to 4.2% compared to an average of 5.1% during the first two quarters of the year.

Core consumer prices were higher by 2.9% on a year-over-year basis compared to a 2.6% reading in 2Q 2025. The combination of healthy growth and a little higher core inflation lowered the likelihood of a January rate cut even further to 13% compared to 20% prior to the release of the data. The key read-through from the third quarter data is that the combination of strong growth in real GDP and a modest gain of only 154,000 jobs during the quarter points to a solid gain in productivity, which boosts profitability and leads to higher standards of living over time.

Look for Earnings to Support Further Gains in Common Stock Prices in 2026

Common stocks have been in a bull market since October 2022 following the reset in the market forced by the Federal Reserve tightening monetary policy and a significant rise in Treasury yields. The current bull market started with the typical price-to-earnings multiple expansion as stock prices almost always bottom before earnings. However, since mid-2024 earnings growth has taken over as the dominant driver of stock returns, which in our view is absolutely necessary for the bull market to continue.

Our expectation for higher stock prices in 2026 is largely based on our outlook for the economy’s growth rate to accelerate this year on the continued AI buildout, the business capital spending incentives contained in the tax and spending bill signed into law last summer, along with larger than normal tax refunds from the tax cuts which were retroactive to the beginning of 2025.

Add in an accommodative central bank, lower Treasury yields, generally healthy credit conditions, and a fading of policy uncertainty and a faster pace of economic activity should lead to a second consecutive year of above trend earnings growth. Supporting this perspective, the analysts at Standard and Poor’s are looking for a roughly 17% gain in operating earnings over the four quarters of 2026, following a gain close to 13% for 2025.

The way we see it, the bull market in common stocks remains intact and appears poised to continue this year propelled by strong earnings momentum and a much better sentiment backdrop following the cleansing of some excessive optimism over the past couple months. We view the cautious sentiment regarding the somewhat open ended nature of the AI capital expenditure boom as a pretty clear indication that the stock market is not in bubble territory and still has room to run on the back of strong earnings growth driven by technology-led productivity gains and expanding profit margins.

Bubbles in stock prices that ultimately get burst in a serious bear market are not formed when investors question what companies are doing with their capital expenditures and critically analyze the expected return on those investments. We view the recent easing of monetary policy, with a little more likely to come this year, and core inflation trending toward the Federal Reserve’s 2% target on the back of lower oil prices and moderating shelter costs and wage pressures as positives for common stocks.

While maintaining a positive outlook for common stocks this year, we expect the move higher in stock prices to be accompanied by a fairly healthy rise in volatility, particularly during the first half of the year. Consider that the deal which ended the government shutdown last year provided funding for most federal agencies only through January 30, 2026. Our Congressional leaders have not yet advanced spending proposals to provide funding beyond that date.

The Supreme Court could overturn President Trump’s tariff agenda of last year. While other existing authorities would likely be used to reinstate them, a potentially messy refund of roughly $200 billion of unauthorized tariffs collected last year could be required. Another upcoming decision by the Supreme Court on whether or not President Trump has the authority to fire Federal Reserve Governor Lisa Cook “for cause” will have a significant impact on the future independence of the Federal Reserve to conduct policy.

The confirmation process of the new chair of the Federal Reserve could be contentious and the central bank could well hold policy steady during the remainder of Chair Powell’s term. We assign a probability of a little better than fifty percent that no additional rate cuts will happen before the first FOMC meeting with the new chair in June. We think the lengthy list of positives for the economy and earnings will eventually carry the day this year, but we anticipate a bumpy ride higher for common stocks.

Treasury Market

Near Term Inflation Expectations Decline, Longer Term Inflation Expectations Well Anchored

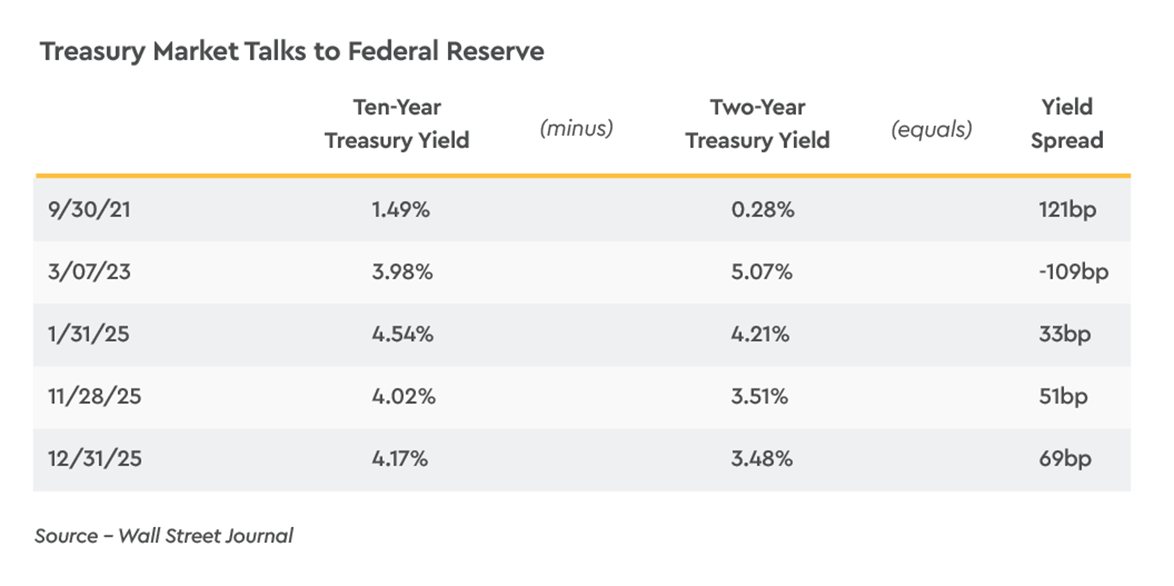

The Treasury yield curve steepened by 18 basis points last month as the yield on the two-year Treasury note fell -3 basis points while ten-year Treasury note yields rose 15 basis points. Although the two-year Treasury yield fell only a modest amount last month, its components made fairly large moves. The implied inflation expectation fell another -38 basis points during December and is a whopping -101 basis points below its recent high reading at the end of August.

The markets are saying that inflation is no longer a scary threat with the limited pass-through of higher tariff costs to final goods prices compared to expectations back in the spring. Recall that in last month’s Investment Strategy Statement (ISS), we commented that in what appears to be an unintended consequence of the aggressive tariff policy implemented last year, the labor market has absorbed the largest portion of the tariffs in the form of diminished employment opportunities.

While near term inflation expectations have fallen, the real yield on two-year Treasury notes rose 35 basis points during December and is higher by 86 basis points since August. The higher real yield is consistent with our view that the tariff-related stall of 2025 will give way to a faster pace of economic growth this year.

While the ten-year Treasury yield rose 15 basis points last month, the inflation expectation remained well anchored at 2.25%, largely unchanged on the month. That means that nearly all of the yield rise was in the real yield rising to 1.92% from 1.78% at the end of November.

Part of the upward pressure on the real yield embodied in ten-year Treasury notes last month was likely due to Treasury securities responding to increased competition for fixed income investments around the globe. During 2025, yields on longer dated sovereign securities generally rose across the globe, with a 43 basis point increase in the yield on ten-year German bonds to 2.86% and a 99 basis point increase in the yield on Japan’s ten-year government bond to 2.07%, its highest level in 26 years. The upward pressure on global sovereign bond yields last year resulted from a general concern over persistently high budget deficits across many countries, as well as expectations for a pickup in growth.

In the U.S., another year of a federal budget deficit around $1.8 trillion and our expectation for an acceleration in the economy’s growth rate lumps the U.S. yield dynamics in with other sovereign yields. Where the ten-year Treasury yield settles out in coming months will likely depend on yield levels on overseas sovereign bonds and from a tug-of-war between inflation pressures falling and the economy’s growth rate picking up some steam, resulting in an environment of nominal GDP running about 4.5%. Historically, the ten-year Treasury yield gravitates toward the economy’s nominal growth rate.

As such, we do not expect the yield on the ten-year Treasury note to trade consistently below 4% over the next few quarters, unless the economy’s growth rate disappoints in large measure from the economy’s 2% average annual growth rate since 1970. We are expecting an acceleration in the economy’s growth rate to a range of 2.5% to 3% in 2026 as the economy rebounds from the 2025 stall.

In this environment investors should continue to benefit by embracing a barbell approach by taking advantage of still high yields on the short end of the yield curve, largely due to the heavy issuance of Treasury bills to finance the federal budget deficit, while also modestly extending duration to lock in yields on intermediate term -- three to seven year -- fixed income securities.