June Stock Market Update

6/6/2023 (Updated: 1/16/2026) - On Point Investment Strategy Statement | SouthState Wealth

As we near the midpoint of the year, it is worth addressing a peculiar dynamic unfolding in the stock market, specifically the S&P 500, where a significant portion of the overall return is being driven by relatively few companies’ stock returns.

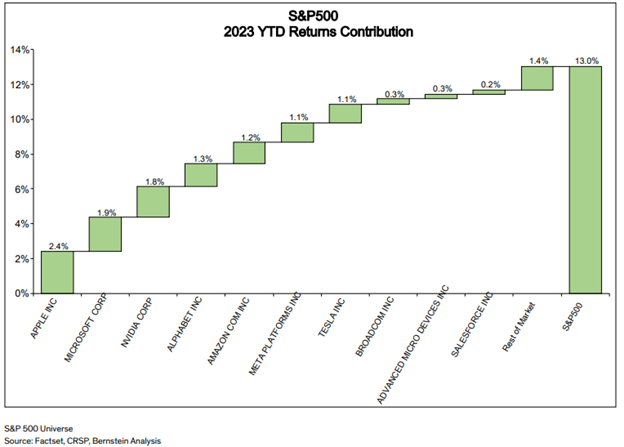

Within the S&P 500, 10 stocks have contributed 90% of the Index’s 13.0% gain this year: Apple (up 39%), Microsoft (+36%), Nvidia (+164%), Google (+38%), Amazon (+48%), Meta (+120%), Tesla (+91%), Broadcom (+45%), AMD (+87%) and Salesforce (+58%). The year-to-date absolute contribution (9.4%) from the top 10 stocks to total index performance is the highest of any half-year period in 40+ years of available date. (The next closest was 6.9% in the second half of 2020.)

What’s even more notable is that the performance of the 10 stocks powering the rally has been driven nearly entirely by multiple expansion: i.e., the willingness to pay for possible future growth as opposed to actual earnings. Historically, concentrated returns have been driven by a combination of earnings growth and multiple expansion. After the year-to-date moves the average stock in the cohort trades at 6.5x sales and has a Price to Future Earnings of 32x, vs. the top 1500 stock average of 2.2x and 18.7x. The average Price to Future Earnings multiple for the cohort has expanded by 48% YTD vs. 16% for the broader market.

So why is this and what happens next? The common thread amongst these companies is that they are all tied to the artificial intelligence boom that started to take form in the latter half of 2022. The A.I. phenomenon will be addressed in a subsequent On Point but it is safe to say that given the rapid rise in valuations and history being rife with examples of niche (especially) technology bubbles, that a buyer-beware mentality is warranted. Market forecasters examined the 6- and 12-month performance of the broader market and the top 10 contributing stocks following 6-month periods of very concentrated market performance. They found that on average, overall market returns were modestly below historical average levels (1.20% below over 6 months; .70% below over 12 months), and that the performance of the top 10 contributing stocks underperformed the market by 3.6% and 3.8% on average in the following 6 and 12-month periods. The sample size is small given this is a rare phenomenon, but also note that the magnitude of the top-10 contribution this year is unprecedented.

Within the S&P 500, 10 stocks have contributed 90% of the Index’s 13.0% gain this year: Apple (up 39%), Microsoft (+36%), Nvidia (+164%), Google (+38%), Amazon (+48%), Meta (+120%), Tesla (+91%), Broadcom (+45%), AMD (+87%) and Salesforce (+58%). The year-to-date absolute contribution (9.4%) from the top 10 stocks to total index performance is the highest of any half-year period in 40+ years of available date. (The next closest was 6.9% in the second half of 2020.)

What’s even more notable is that the performance of the 10 stocks powering the rally has been driven nearly entirely by multiple expansion: i.e., the willingness to pay for possible future growth as opposed to actual earnings. Historically, concentrated returns have been driven by a combination of earnings growth and multiple expansion. After the year-to-date moves the average stock in the cohort trades at 6.5x sales and has a Price to Future Earnings of 32x, vs. the top 1500 stock average of 2.2x and 18.7x. The average Price to Future Earnings multiple for the cohort has expanded by 48% YTD vs. 16% for the broader market.

So why is this and what happens next? The common thread amongst these companies is that they are all tied to the artificial intelligence boom that started to take form in the latter half of 2022. The A.I. phenomenon will be addressed in a subsequent On Point but it is safe to say that given the rapid rise in valuations and history being rife with examples of niche (especially) technology bubbles, that a buyer-beware mentality is warranted. Market forecasters examined the 6- and 12-month performance of the broader market and the top 10 contributing stocks following 6-month periods of very concentrated market performance. They found that on average, overall market returns were modestly below historical average levels (1.20% below over 6 months; .70% below over 12 months), and that the performance of the top 10 contributing stocks underperformed the market by 3.6% and 3.8% on average in the following 6 and 12-month periods. The sample size is small given this is a rare phenomenon, but also note that the magnitude of the top-10 contribution this year is unprecedented.